Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

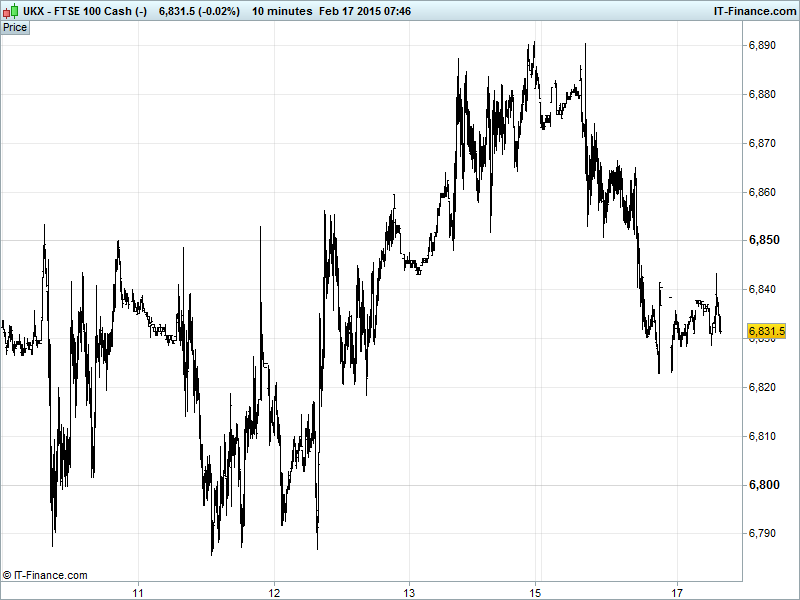

UK 100 Index called to open -25pts at 6830, having fallen back from another foray close to 6900 highs, but with support kicking in around 6820 which gives us a trend of rising lows in February. Trading activity remains in the upper half of the sideways channel from 22-Jan. Rising support could mean there is still potential for a continuation of the uptrend from mid-December. Watch levels Bullish 6910, Bearish 6800.

The negative open comes after talks between Greece and the Eurogroup collapsed, ending in acrimony with Greek rejection of a revised draft proposal to change the flexibility of its current bailout programme, adding to fears of a ‘Grexit’. Geopolitical concerns continue with the Ukraine ceasefire proving somewhat patchy.

Eurogroup head Dijsselbloem (who revised a previous EC draft for Greece that was deemed acceptable) sees a 6-month extension as the best solution, giving it until Friday to make a decision, while the IMF review establishes that if criteria are not met then there will be no further disbursement. Uncertainty prevails as talks continue.

No lead from US Stocks due to President’s Day holiday, however there was some hawkish chat from the Fed’s Mester who said she wants to drop the ‘patient’ terminology from the next FOMC policy statement before raising US rates in June. This helped strengthen the USD.

Asian stocks mixed overnight with progress tempered by Greece’s rejection of a second draft bailout renegotiation with European counterparts. China data showed new house prices declining for a fifth straight month with contraction even accelerating, suggesting deepening economic weakness in the world’s number two economy.

Australia hindered by RBA minutes proving less dovish than expected with a lack of forward policy guidance, but much debate about another rate cut at the next meeting given the slower growth outlook (China’s appetite for raw materials) and subdued inflation. China stocks and Hong Kong are outperforming ahead of the Lunar New Year holidays and despite disappointing China property readings with hopes that more stimulus may be on the way.

In focus today we have the fallout from the disastrous EU finance minister’s meeting yesterday on the Greek debt situation. Next up will be the UK CPI, seen slowing even more recently which will make life a whole lot more difficult for those in the UK rate-hike camp. In Germany all eyes will be on the ZEW survey at 10:00 to see whether positive expectations will be met, adding to the GDP beat on Friday. US Empire Manufacturing and Housing Market data are all expected to improve too.

Gold ($1225) has headed back from yesterday’s $1235 highs overnight despite the growing chaos in Eastern Europe and politicians keeping the uncertainty ball in the air regarding Greece’s bailout negotiations. A slightly stronger USD is a hindrance following Mester’s hawkish tones as was lower volumes on US President’s Day and Chinese preparations for Lunar New Year Holiday starting tomorrow (for 1-week). Support likely around $1220.

Oil holding around yesterday’s levels ($62 for Brent and $53 for US Light Crude), unhindered by the stronger USD, supported by rising violence in Libya and uncertainty in the Eurozone. The February uptrend and recovery from lows on hopes that adjustments to global supply glut (capex cuts, rig counts etc.) will eventually flow through.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Property Prices Deteriorated

- China MNI Business Indicator Deteriorated

- EU New Car Registrations Improved

UK Company Headlines: (Source: Reuters/DJ Newswires)

- John Wood Group FY total rev up 7.8 pct

- Profits rise at hotelier IHG on strong U.S. demand

- New British bank Aldermore more than doubles 2014 profit

- Kenmare Resources sees 15 – 20 pct headcount reduction in Moma mine

- UK's Wood Group says full – year pretax profit rises 3 pct

- Alliance Pharma says finance director Richard Wright to leave

- Canada's Fairfax to buy insurer Brit Plc for 1.22 bln stg

- Hargreaves Services H1 pretax profit from cont ops 15.2 mln stg

- Sinclair IS Pharma posts wider H1 pretax loss

- Mobile-banking software firm Monitise's EBITDA loss widens

See Live Macro Calendar for full data line-up, incl. consensus expectations