Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

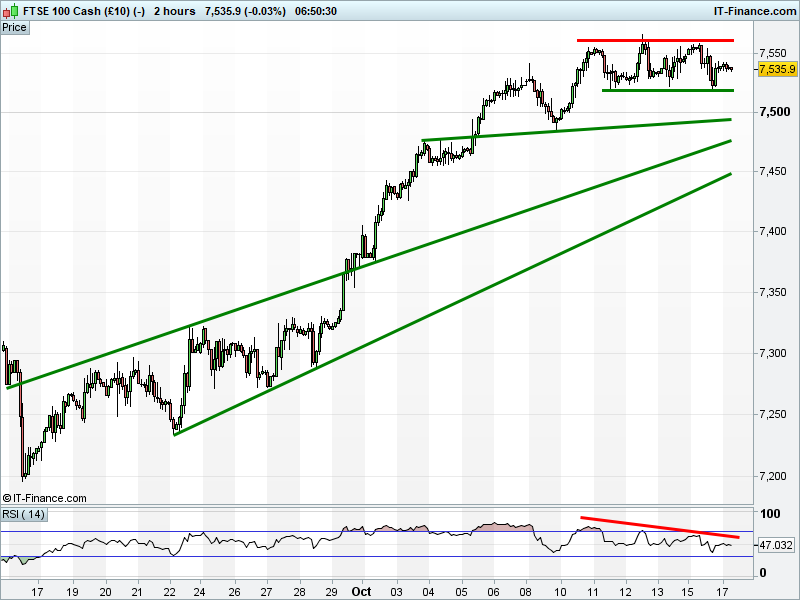

UK 100 Index called to open +5pts at 7530, up off yesterday’s closing low, holding its sideways 7520-7565 shift as it consolidates the recent 7200-7555 rebound. Bulls need a break beyond 24hr falling highs resistance at 7540. Bears require a breach of 5-day support at 7520 lows, but face multiple support hurdles thereafter. Watch levels: Bullish 7540, Bearish 7520.

Calls for a solid open come after yet more record highs on Wall St and a positive session in Asia overnight after the USD strengthened further. This has added to GBP weakness, helping sentiment towards UK Index internationals. Geopolitics still very much in play as we await the Catalan independence response and the upshot of PM May’s Brexit dinner in Brussels.

Overnight, Australia's ASX outperforms thanks to Energy, even as the oil price pulled back form is Kurdistan disruption inspired highs. Results from Rio Tinto and still solid Copper and Iron ore prices has also helped. Japan’s Nikkei added to its 21yr highs, as the stronger USD sent JPY lower to benefit exporters. China was quiet on account of the 19th Party Congress in Beijing this week.

UK Index headlines include AstraZeneca being granted FDA priority review for Imfinzi for advanced unresectable Non-Small Cell Lung Cancer. Rio Tinto hit a near 5y high down-under after a solid Q3 production update, with iron ore shipments up, although with lower copper output and guidance. Smiths Group announces new CFO.

Bellway outlook positive, expects FY volumes up at least 5%. Pearson 9M Revenues Consistent with upper half of guidance; 300m share buyback. Mediclinic results impacted by FX. Merlin warns on revenues and profits after difficult summer, Legoland NY planned for 2020. ASOS FY group revenues +33% (UK +16%, Int +47%), PBT +26%. Virgin Money profitability, earnings and returns in line with expectations; 10% mortgage market share.

US equity markets closed at all-time record highs as Financial names led wider market sentiment. The Dow Jones closed 85pts higher thanks to JP Morgan and Apple strength, the latter after a broker upgrade, while the S&P 500 rose 0.2% as Telecoms rallied alongside the Financial sector. Note Netflix saw continued subscriber growth in Q3, beating analysts’ estimates by almost 1m to trade a fresh all-time high after hours.

Crude Oil prices have come off the boil as Kurdistan tensions abate while the US dollar has continued to rally from its lows. Global benchmark Brent has recovered from overnight lows of $57.5, however remains a distance from yesterday's 3-week highs, while US Crude remains under pressure, trading close to overnight lows of $51.6.

Gold has continued to retreat below $1300 as traders react to yet another new frontrunner for the Fed chair job emerging last night. Stanford University economist John Taylor, a favourite of President Trump, is widely seen as a hawkish figure, with his Taylor rule advocating for higher interest rates. The subsequent stronger dollar has seen the precious metal fall to a low of $1290 overnight despite a brief recovery to $1296.

In focus today will be UK Inflation (9:30am). With expectations that the Bank of England will imminently raise interest rates for the first time since the 2008 financial crisis, forecasts for headline CPI to have re-accelerated to 3% in Sept (highest since early 2012) may all but seal the deal. Whilst also requiring the BoE governor to write yet another letter to the chancellor (new pen required?) to explain the latest and continued overshoot, a fresh 3% reading while GBP has recently rebounded might also dent the idea that rising inflation is merely a product of Brexit-weakened GBP.

Other releases of note include Eurozone CPI (10am) seen unchanged at 1.5%, German and Eurozone ZEW Surveys (also 10am), US Industrial and Manufacturing Production (2:15pm) and US NAHB Housing Market Index (3pm). US earnings include banking giants Goldman Sachs and Morgan Stanley, both expected before the US open, followed by tech behemoth IBM tonight after the close.

Speakers today include ECB vice-President Constancio (9am) who gives a keynote speech at a Conference on Financial Stability organised by Banco de Portugal in Lisbon and ECB Chief Economist Praet (10.30am) participating in a panel discussion at the High level international conference "More than ever, Europe matters" in Brussels.

At 9.15am, Bank of England (BoE) Governor Carney testifies in front of the Treasury Select Committee (TSC) alongside newly arrived colleagues Ramsden and Tenreyro, while the Bank’s Brazier (Financial Stability Strategy and Risk; 2.30pm) speaks to businesses in Leicester. The Fed’s Harker (voter, hawkish, 6pm) speaks on "Equitable Transit" in Pennsylvania.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.