Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

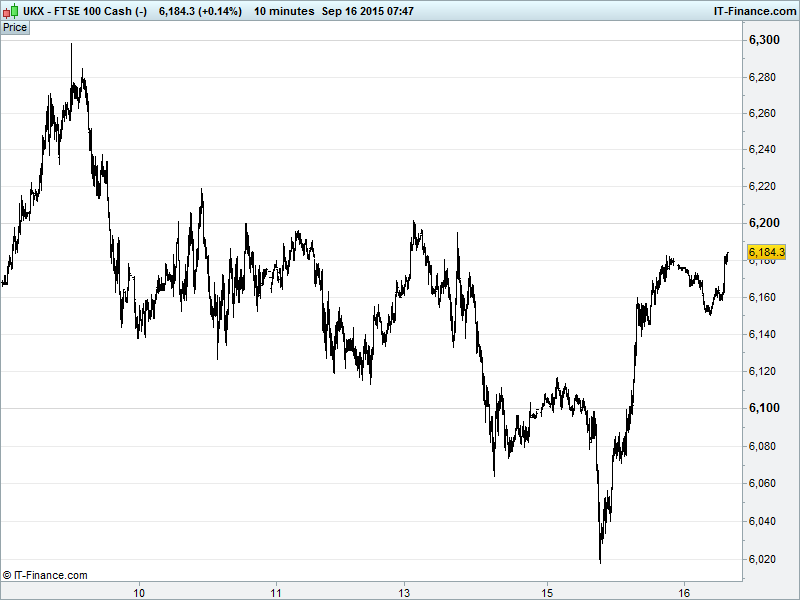

UK 100 Index called to open +40pts at 6180 after recovering strongly from yesterday’s lows to get back above the trend-line of rising support breached on Monday. Overnight weakness found support at 6150 which suggests brief consolidation and thus appetite for uptrend from August lows to be revived, although recent highs of 6200 need to be cleared meaningfully before we can look towards 6300 and higher. Watch levels: Bullish 6205, Bearish 6120.

The positive opening call comes courtesy of gains in Asia echoing advances in Europe and the US yesterday along with oil rising further from September lows. Is fear receding ahead of tomorrow’s Fed decision? Are markets less worried about a hike or more convinced of no change? Consensus remains divided after the latest US data.

In Asia-Pacific, Japan’s Nikkei higher, helped by a weaker USD/JPY however underperforming peers amid thin volume as investors brace for tomorrow’s Fed decision. China is recovering some of yesterday’s heavy losses, helping Hong Kong’s Hang Seng outperform.

Australia’s ASX is middle of the group despite a stronger AUD/USD and RBA’s Debelle saying medium-term growth may have slowed, while China FX regime change is a welcome development and he’d be surprised if Fed rate hike didn’t result in volatility.

US stocks closed up in yesterday’s session with seemingly growing confidence the Fed will hold fire on rates tomorrow. All major US indices up over 1% (DOW +1.4%, S&P +1.3%, NASDAQ +1.1%). 14 out of 30 economists surveyed by the FT said they expected a rate rise on Thursday while just 25% of actual investors are expecting the same – a good example of the ravine that exists between economists and their theories and the ‘reality’ experienced by market participants themselves.

Nonetheless, so-called ‘risk-off’ positions (long USD, short EM equities and currencies) which will pay off in the event of a US rate hike are seen to be ‘crowded’ ahead of the FOMC meeting and, with 2 more opportunities for the Fed to pull the plug in 2015, such positions may still prove profitable.

Note ‘risk-off in this sense does not include Gold ($1105), which is still languishing around those month lows with any meaningful moves likely to a) come after tomorrow and b) be short lived as an eventual US rate hike becomes inevitable.

In corporate news, note battered mining giant Glencore (GLEN) confirming its rights issue raised the target £1.6bn ($2.5bn) required to bolster its balance sheet via the sale of 1.3bn new shares at 125p.

In focus this morning will be UK Employment and wages data at 9.30am with consensus looking for the latter to accelerate in the three months to July while joblessness stays put in . Eurozone Consumer Price Inflation seen recovering to flat in August after July deflation, although still too low on an annual basis.

US Consumer Price Inflation in the afternoon expected to show a drop to deflation in August adding to Fed woes in terms of progress on jobs front but inflation still MIA. The US NAHB Housing Market Index seen unchanged in September.

Crude prices seen posting moderate gains this morning (WTI $45; Brent $48) as the US Dollar reacts in kind to diminishing expectations of Stateside fiscal policy tightening and with Yesterday’s API data showing US inventories contracting by 3m barrels in the week ending 11 Sept, missing consensus ahead of today’s more closely watched EIA stockpiles report.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Glencore raises $2.5bn via share placement

- Ladbrokes CFO Ian Bull to step down in Feb 2016

- Serco sells BPO division for £250m to Blackstone

- Stagecoach subsidiary gets new East Midlands rail franchise

- Imagination Tech forecasts first – half loss after market weakens

- Hornby sees H1 revenue lower than prior year

- Galliford Try Pretax Profit +20% in FY15

- JD Sports Fashion Reports 88% Jump in 1H Pretax Profit

- Balfour Beatty Infrastructure to Buy Alkane Energy For £61.4m