Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

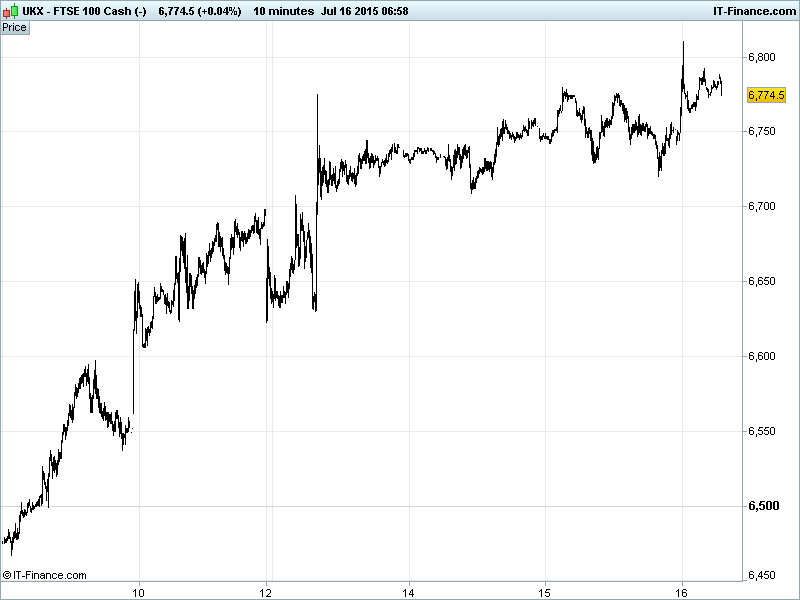

UK 100 Index called to open +15pts at 6770, continuing to inch higher after Tuesday’s breakout above falling highs at 6730. The overnight test of 6800 shows appetite to recover May/June highs of 7000, and could be repeated today. Note potential for 200-day moving average 6747 to act as support for any pullback. Updated watch levels: Bullish 6810, Bearish 6640.

The positive opening call comes thanks to the Greek parliament overwhelmingly, but needless to say reluctantly, passing tough austerity reforms to allow finalisation of a €86bn bailout to keep it in the Eurozone. The overnight vote should allow immediate disbursal of €7bn to tide it over and avoid default on an ECB bond which would otherwise see life support for its banks withdrawn.

This is despite violent public protests in Athens and political risk attached to rebellion by over a quarter of coalition leading Syriza members which may require a cabinet reshuffle if PM Tsipras (who says he will not resign) is to keep the party together despite admitting to mistakes and to putting a weight on Greek people but only through accepting the ‘least bad option.

US markets closed slightly lower after a lacklustre session on uncertainty over the Greek vote and USD strength (new July highs) from Fed Chair Janet Yellen’s testimony in which she gave an optimistic view of the US economy (in-line with Beige Book data) and said US interest rates could start rising later this year.

While she may have said this would be only if the economy is strong enough and that every FOMC meeting is ‘live’, taking into account current data and events, note more hawkish tones from the Fed’s Williams who talked of September lift-off and Mester saying ‘economy can easily deal with a rate rise now’.

Asian markets largely traded higher overnight spurred by the Greek parliament’s ‘yes’ vote, even though the poll exposed deep divisions within Syriza, and US Fed chair Janet Yellen’s reassurances that, even though US rates should be hiked sooner rather than later, the economy must be ready. Markets seemingly feeling that it isn’t, but the Fed had better get on with it if it wants to avoid shocking them…

The Shanghai Composite stabilised after an initial sell-off after 2 days of losses fuelled fears of another market rout while yesterday’s positive GDP print was largely seen as being, if not totally cooked, the result of the H1 stock surge that ended abruptly last week and thus raised doubts about what will happen in the second half of the year.

In focus today will be Eurozone June final CPI data, the US Philly Fed and US NAHB Housing Index. Closer to home, ECB President Draghi gives his press conference after central bank's monthly policy decision (any update on Greek bank’s life-line or bailout deal?).

Crude prices bounced off rising support overnight but suffered prior as Janet Yellen made the case for an interest rate rise this year which sent the US dollar basket to 3-week highs, adding pressure to already pressured oil prices after an Iranian nuclear deal was announced yesterday. Both Brent ($57) and WTI ($52) off overnight lows but struggling this morning with narrowing sideways ranges potentially indicating consolidation in advance of further losses.

Gold ($1147) has broken down and out of its continuation pattern as expected after the US Dollar strengthened off the back of Yellen’s hawkish rhetoric, and perhaps due in part to risk-offness following the Greek parliament’s vote to pass tough economic reforms in return for a third bailout package, though we note Gold’s unwillingness to perform in its role of safe-haven of late.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Anglo American plans up to $4bn H1 write-off

- Anglo American sees non-cash impairment at June 30 of $3-4bn after tax

- Dixons Carphone yearly profit tops forecasts

- Petroceltic says received request for EGM from Worldview

- Wincanton says continues to trade in line with expectations

- Experian says Q1 organic revenue rises 3 pct

- Telford Homes says current pipeline extends into 2019

- Hilton Food Group says trading in line with expectations

- British government's stake in Lloyds falls below 15%

- Premier oil says awarded two shallow water blocks in Mexico

- UK regulator to examine separation of BT network unit

- Sports Direct posts profit rise but cuts bonus scheme target

- Big Yellow Group says Q1 revenue £24.1m versus £18.9m

-----------------------------------------------------------------------------------------------