Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

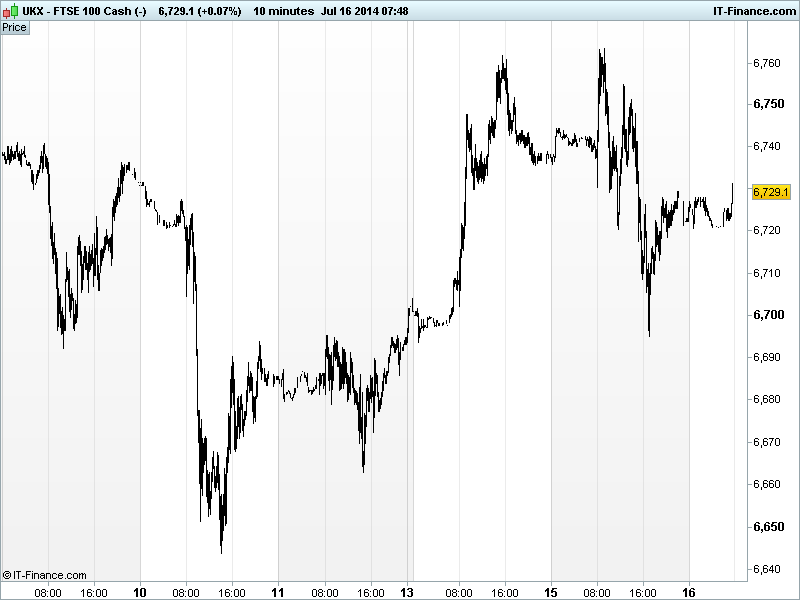

UK 100 called to open a muted 10pts higher at 6730, echoing cautious Asian trading despite better than expected China GDP data which suggested the growth slowdown may be bottoming out and offer a platform for recovery in the second half of the year, as well as positive US results and more M&A.

China GDP growth accelerated from 7.4% YoY in Q1 to 7.5% in Q2, which is in-line with the government’s full-year target, while Industrial Production also grew faster than in Q1 and beat forecasts but Retail Sales was just below consensus. The question now is whether more stimuli is needed.

Market Sentiment in Asia was already shaky after US markets closed mostly lower, back from recent highs, following Fed Chair Yellen’s testimony to the Senate Banking Committee where she said an accommodative stance was still appropriate but highlighted concerns of stretched equity valuations, notably small social media and biotech which saw the Nasdaq close as the standout underperformer.

In Europe markets closed lower after reports that the Rioforte holding company for Portuguese Espirito Santo (the group, not the bank BES in which it has a 25% stake), was preparing to file for creditor protection which suggests that the market reaction we saw last week may have legs. Portugal on the ropes?

Following Yellen’s prepared speech, the Fed’s hawkish George urged rising rates from zero soon on the back of a stronger economy and warned against waiting too long while noting potential excesses in financial markets. Pimco’s Gross also tweeted that Yellen is focused on inflation/wages rather than unemployment with wages growth of 3.5% being the trigger for first rate rise.

On the results front, Intel beat expectations and offered a strong outlook, Yahoo! missed but Rio Tinto (RIO) shares +1% in Australia overnight after it announced a 23% rise in Q2 iron ore shipments after expansion at several vast Australian Outback mines even as prices tumbled and upped 2014 Copper output guidance.

In focus today we have UK Unemployment with expectations of a drop back to 6.5% thanks to a fall in jobless claims, but with average weekly earnings still growing well below inflation. After more better than expected US Q2 bank results yesterday (JPMorgan, Goldman Sachs), today it’s the turn of Bank of America.

In the afternoon consensus is looking for a slowdown in US Industrial and Manufacturing Production but an increase in capacity usage. The Fed Chair speaks again, but there will likely be more focus on the release of the Beige Book for an update on the US growth picture. ebay reports Q2 results after the US close.

In commodities, Gold back below $1300 after the USD strengthened on the prospect of higher borrowing costs following the Fed Chair’s testimony which dampened demand for the metal.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- CHINA GDP Beat

- CHINA Industrial Production Beat

- CHINA Retail Sales Miss

- CHINA Fixed Asset Inv (ex-rural) Beat

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Fresnillo says on track to achieve 2014 guidance

- Fresnillo reports flat second – quarter silver output

- Britain's Severn Trent says on track for dividend rise

- Big Yellow Group says Q1 trading in line with expectations

- Royal Mail receives notice of French antitrust probe

- Gem Diamonds says Letšeng probable reserves up by 67 pct

- Sports Direct's Ashley withdraws from 2015 bonus share scheme

- Hochschild Mining says on track to meet 2014 production target

- London Stock Exchange says q1 income rises 16 percent

- Balfour JV wins 300 million stg Hong Kong contract

- Oxford Instruments first-quarter orders ahead of last year

- ICAP says Q1 revenue dips 14 percent

- Wincanton says continues to trade in line with expectations