Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

"Growth concerns and gaseous threats bring UK Index back from highs"

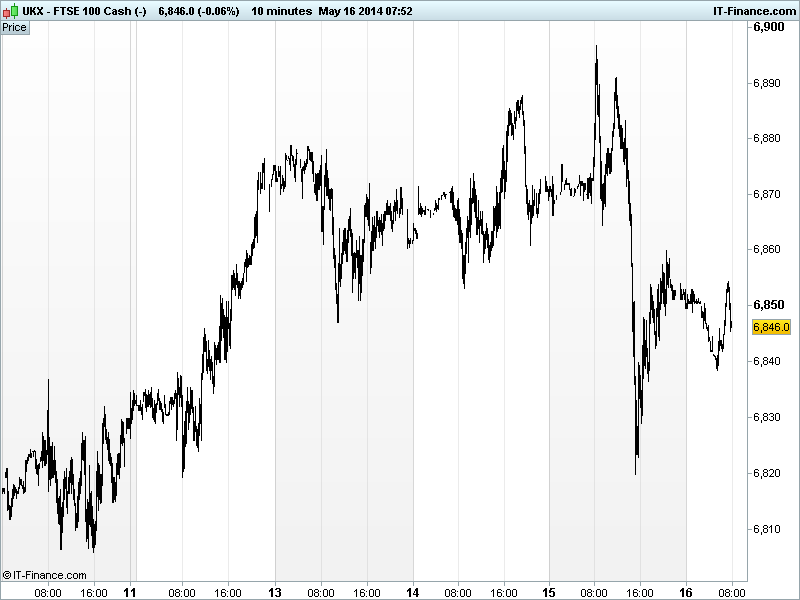

UK 100 called to +10pts at 6850, off its lows of 6820 yesterday following the sharp 80pt sell-off on soft corporate earnings (read Wal-Mart) and US data adding to global growth concerns after US Industrial production and Housing data missed expectations and offset improved jobless claims and a very positive Empire State Manufacturing. Lower Eurozone GD growth already had global growth concerns back on the radar earlier in the day.

The Russia/Ukraine situation reared its ugly head yesterday afternoon adding geopolitics back to the mix with the Slovakian PM saying Russian President Putin had informed multiple EU states that gas supplies via Ukraine would be cut off by 1 Jun if Ukraine doesn’t pay its bills. With current sanctions, is Putin fighting fire with fire? Concerns continued overnight and may well do so into the week-end.

US stocks (S&P & DJIA) closed around 1% down, in the red for the second day in a row, giving the benchmark indices their biggest losses in a month, with nervous selling linked to the reasons above and proximity to recent record highs; tech-biased Nasdaq and small-caps unable to escape another tumble.

Overnight Asia stocks showing losses, with Japan the underperformer due to a weaker USD/JPY on US growth concerns (USD weaker) as well as significant upward revisions to Japanese Industrial Production growth for March adding to the strong GDP and ‘end-of-stimulus’ presumption yesterday already strengthening JPY and hurting equities. India’s Sensex at record highs on hopes of a new government.

Fed Chair Yellen spoke overnight, reiterating her view that the US has more work to do before it can be classed as ‘healthy’ whilst pledging to “do our part” in promoting the recovery. Fed support still needed. Data overnight saw China’s MNI Business Indicator improve in May while Foreign Direct Investment in the nation rebounded in April.

In focus today, after the growth concerns from the US yesterday, all eyes will be in the US Housing Starts and Building Permits in the afternoon with growth of around 1m expected for both, before the week for data closes with the Uni of Michigan Consumer Confidence which is seen climbing from 84.1 to 84.5 in April.

The UK flagship index almost got as high as 6900 yesterday, but the global sell-off took it back sharply and breaking the 1-month rising lows. We have bounced off 6820 and found resistance overnight at 6850. The question now is whether we take another leg down, with this being a correction after gains of 400pts in a month or whether 6840 lows this morning (and recent breakout level) helps to get us back on a northerly course.

In commodities, Gold trading at $1294, below the $1300 mark despite concerns about Russia cutting Europe’s gas supplies off. US Light Crude holding around $102 and Brent Crude around $109, just below its recent highs of $110 on continued geopolitical uncertainty.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- CN MNI Business Indicator Improved

- CN Foreign Direct Investment Beat, rebound

- JP Industrial Production Improved, rebound

- JP Capacity Use Improved, rebound

- EU New Car Registrations Growth slowed

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Coca-Cola HBC Q1 loss widens, expectations unchanged

- Bovis Homes private reservations jump 78 pct for 2014 delivery

- SIG revenue from cont ops for first four months of year up 9.4 pct

- Petroceltic looks to raise $100 mln via placing

- Carphone agrees sale of Virgin Mobile France to Numericable Group