Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

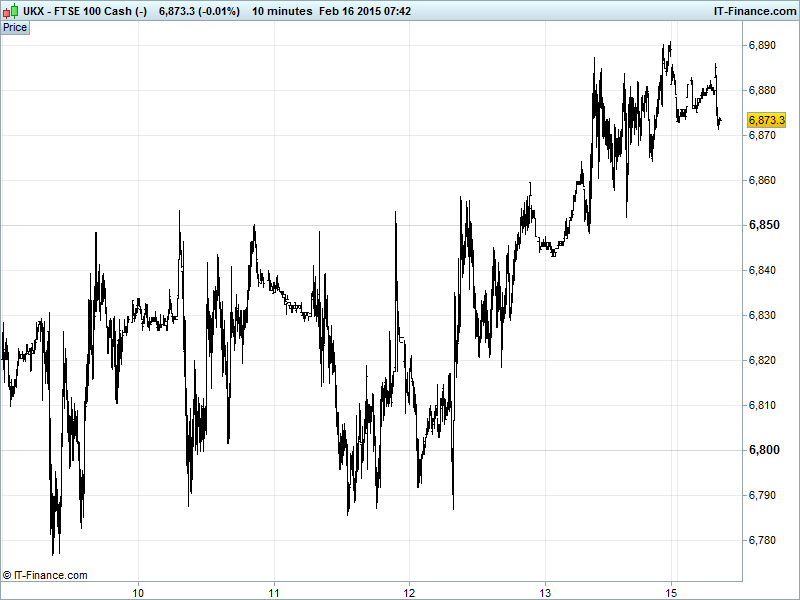

UK 100 Index called to open flat at 6875, still holding just below 6900 with desire to test and breakout above recent 6905 highs to allow for a revisit of 6950 all-time highs. The break above 6850 could mean this level becomes support for any near-term weakness. Still within sideways channel from 22 Jan. Still potential for this to be a pause within the uptrend from mid-December. Watch levels: Bullish 6910, Bearish 6840.

The steady open to the new week comes courtesy of last week’s strong gains driven by positive Eurozone data but investors still waiting for proof of real progress on both the Greek debt negotiations (extended talks expected, still significant gaps between both sides) and the ceasefire in Ukraine (tentative at best). Note Asian equities failing to get too excited by Japan’s exit from recession and ratings agency DBRS confirming Germany as AAA stable.

US bourses ended higher with Dow Jones toping 18,000 for the first time in 2015 and the S&P500 registering a new record intraday and closing highs and Nasdaq at highest level since 2000. This despite pessimistic sounds from Brussels/Ukraine, with positive German/Eurozone GDP, a higher oil price and continued hopes of delayed US monetary policy tightening/more stimulus from other central banks offsetting mixed end-of week US prints (Consumer confidence, Import prices).

Asian stocks benefiting from the news that Japan’s economy pulled out of recession on Monday, though the comeback was weaker than forecast, showing that PM Abe’s administration may be starting to get things right even if GDP growth of 0.6% QoQ/2.2% YoY missed expectations of 0.9% QoQ/3.7% YoY, while improving employment and income data and lower energy costs are expected to further assist in the recovery.

China stocks boosted by rise in Foreign Direct Investment (FDI) grew by 29.4% to $13.9B in January and Asian market sentiment was generally hopeful despite internal warnings from the State Administration for Foreign Exchange about Chinese capital outflows and, further afield, the ongoing Greek debt talks and a seriously shaky ceasefire in Ukraine.

In focus today will be Greek negotiations on its bailout extension as well as the tentative ceasefire in Ukraine. These geopolitical risk points dominate a quiet macro calendar on account of it being President’s Day in the US which sees many stateside bourses closed.

Gold ($1230) still bouncing from recent $1215 lows, supported by the weaker USD (mixed macro data, hopes of delayed US tightening) and much geopolitical uncertainty (Greece, Ukraine). Still in lower half of falling channel from Jan 22 with major support (3-month rising, 18 month intersecting) possible around $1200.

Oil little changed around recent highs after its bounce saw Brent hit $62 and US Light crude sits just shy of $54, supported by another drop by the Baker Hughes Rig Count (-30% from October to lowest since 2011 although production stull rising), a weaker USD and continually conflicting growth data from round the world. Talk of demand being revived by Libyan conflict offsetting some of global supply glut fears.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan GDP Miss, but improved

- UK Right move House Prices Mixed

- Japan Industrial Production Growth Slowed

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Aer Lingus names Stephen Kavanagh as new CEO

- Fidessa Group FY pre – tax profit falls 9 pct

- Balfour Beatty sells majority stake in offshore project

- Trading software maker Fidessa's profit hit by strong pound

- Mecom says shares to be delisted from LSE on Feb. 17

- Landlord Hammerson's NAV rises on increased leasing activity