Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

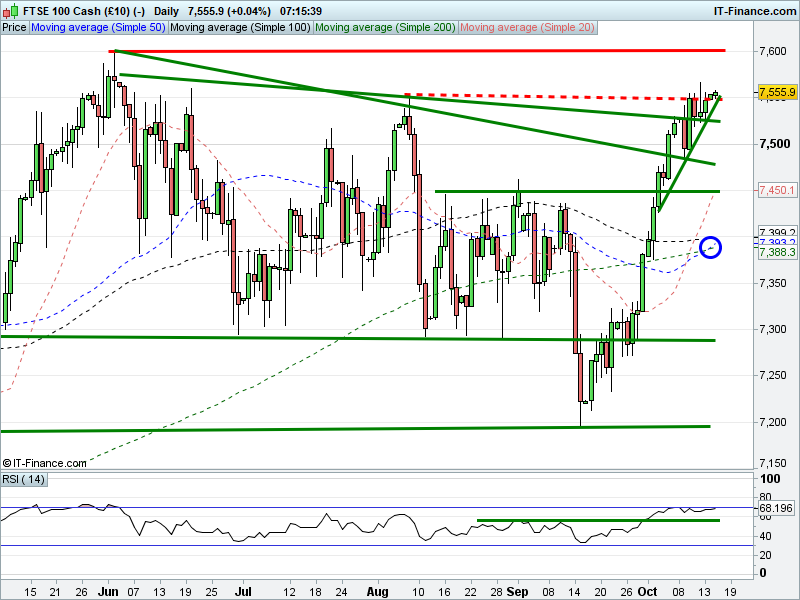

UK 100 Index called to open +20pts at 7555, holding an October rising channel and showing appetite to push north for meaningful breakout beyond August highs. Bulls still need to see Thursday‘s highs of 7565 exceeded. Bears need a breach of rising support at 7535. Watch levels: Bullish 7565, Bearish 7535.

Calls for a positive open come after Wall St closed higher on Friday as mixed Bank earnings and slower US inflation data fueled hopes of a slower Fed hiking cycle. Asian bourses have made a solid start to the week thanks to supportive Chinese inflation which has helped metals prices higher (helpful for UK Index Miners) while oil has rallied on fears of supply disruption amid conflict between Kurdistan and Baghdad after last month’s referendum.

While USD was dented on Friday, Fed Chair Yellen’s weekend reiteration of a strong economy and labour market has seen the dollar recover, to the detriment of GBP, hence a higher UK Index opening call. GBP is also off its highs after an EY forecast that the Bank of England would hold off from raising interest rates next month and UK Rightmove House Price data showing a new North/South divide, the North faring better than London/SE amid Brexit uncertainty.

Australia's ASX outperforms thanks to China data supporting base metals, the oil price rally boosting Energy and the combination of a weaker USD and geopolitics (Trump, Iran, NK, Catalonia, Austria) sending Gold back above $1300. Japan’s Nikkei is performing almost just as well helped by Energy and a USD rebound pushing the Yen lower to help exporters.

UK Index headlines include ConvaTec lowering full year guidance. Sources say 3i Group buys Smarte Carte for $385m Including Debt. Ultra Electronics PCS awarded $16m in contracts for additional HiPPAG stores ejections systems. Polymetal reports record production of 470 Koz of gold, +26% YoY. Hilton Food Invests NZ$54m in New Zealand Packaging Plant. Interserve confirms that it is engaged in constructive and ongoing discussions with its lenders

Crude Oil prices have extended their rebound (WTI $52.1, Brent $57.6) helped by a lower Baker Hughes Rig Count on Friday, US President Trump threatening to rip up the Iran nuclear accord, fighting in Kurdistan and the weaker USD. There is potential for a return to recent $53/59 highs. Gold is back above $1300 amid the combination of a weaker USD and geopolitical risk. This test of intersecting resistance could open the door for a rally back towards $1350.

In focus today - macro data distinctly lacking - Eurozone Trade Balance (10am) may offer clues as to the strength of the economic area’s economy while US Empire Manufacturing (1:30pm) is expected to continue to retreat from August’s 3-year high.

With the dearth of macro data, greater impetus is sure to fall on geopolitics with Trump threatening to rip up the Iran nuclear deal, generating concerns among co signatories like the UK, France and Germany. Is he trying to send a message to North Korea? Odd with the EU set to further tighten sanctions.

China's 19th Communist Party Congress starts Wednesday, with delegates converging on Beijing to vote in new officials, although President Xi and Prime Minister Li are expected to serve another 5yr term.

We also have the deadline for Catalonia to clarify its decision on independence (9am) before Madrid decides whether or not to revoke the region’s long held autonomy. Thereafter, UK PM May is visiting Brussels to gee up Brexit negotiations from their current deadlock ahead of a two-day summit (ex-UK) to discuss preparations for a transition period.

Don’t forget also that earnings season continues at full pace with the likes of Morgan Stanley, Goldman Sachs, IBM, GE, J&J, Amex, Netflix and P&G all reporting stateside this week. Closer to home we have production updates from Miners Rio Tinto, BHP Billiton, Hochschild & Evraz and results from Reckitt Benckiser, Unilever, Travis Perkins and Bellway.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.