Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

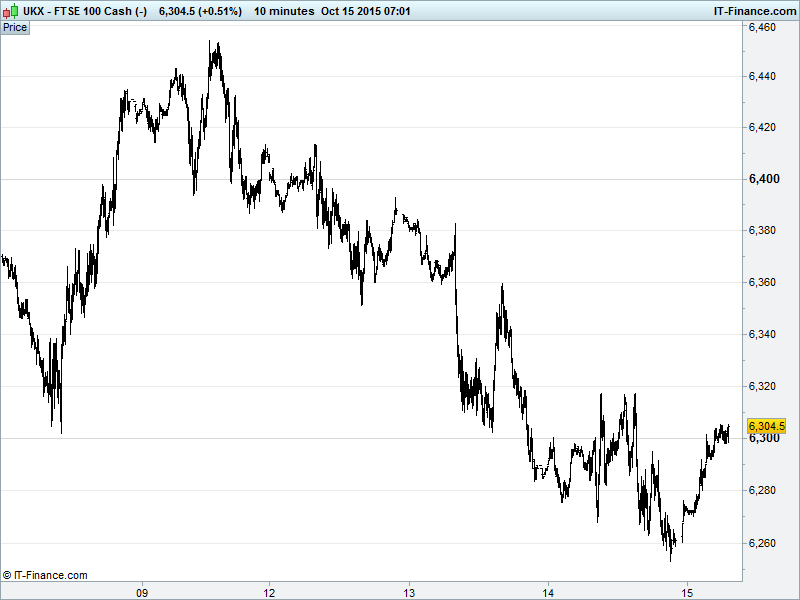

UK 100 Index called to open +30pts at 6300, making a bounce from 6250 overnight lows and breaking out of a 4-day falling channel to regain the key 6300 level. Is the falling channel pause/consolidation after a 10% rebound over? Do we resume the upward march towards 6600 and 7000? The 6300 level is important, the 2015 hinge point, having been Jan lows and September highs. Can we get back into the upper half of this year’s trading range? Updated watch levels: Bullish 6325, Bearish 6275.

The positive opening call comes after Asian bourses rallied (tech, telecoms) along with US futures with weak global macro data (notably US, China) reducing the odds of a 2015 Fed rate hike to their lowest since March. It would appear that Asia is moving on the bad data which is keeping the USD down and input commodities cheap.

Chinese stocks have jumped in Hong Kong after the government said it is reorganizing the telecom industry, heightening speculation that policy makers will accelerate reforms of state-owned corporates to bolster slowing economic growth. Japan’s Nikkei higher for the first session in 3 helped by pharma and tyre manufacturers.

US markets closed lower after the WalMart profits warnings dented sentiment and investors digested weak corporate results from the likes of JPMorgan (JPM) and a muted message from others while the US Beige Book suggested economic activity remained at modest expansion but while jobs improved wage growth was subdued and manufacturing downgraded.

Watch the UK Banks this morning after a Sky News article suggesting regulators will today say lenders need billions more in capital as part of industry reforms designed to protect taxpayers from anther crisis. Those with more investment banking operations like Barclays (BARC) could be more affected than Lloyds (LLOY)

In focus today will be the US Consumer Price inflation data which is seen remaining negative (deflation, rate rise negative) and the core print only just positive. US Jobless claims likely unchanged although Empire State Manufacturing and Philly Fed indicators may have improved quite a bit. Watch the read for average wages growth with concerns about this not flowing through to spending and consumers electing save. The Fed’s Bullard, Dudley and Mester all speak today to keep the communication waters nice and muddy.

Gold has delivered the $1170 breakout we had been watching for rising to $1190 3 ½ month highs overnight, attracting the bulls on the back of a weaker USD from belief in US rate hike delays and increased risk aversion from disappointing earnings season (estimates missed, guidance cut, outlook poor) and macro data (slowing/absent growth). Having broken above Feb falling highs, the yellow metal’s next stop could be June highs $1205.

Brent Crude Oil is holding its recent losses, back down below the key $50 level, as rising US inventories (API) add to global supply glut worries (China consumption slowing, OPEC and Non-OPEC all pumping at full whack. Note more US Crude stocks data today (EIA).

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Virgin Money 9-month gross mortgage lending jumps 38%

- Unilever Q3 sales top expectations

- Hochschild says on track to achieve 2015 production target

- Hochschild launches 3-for-8 rights issue to raise about £64.8m

- Burberry sales growth hit by China slowdown

- Man Group says assets under management -2.5% in Q3

- Game Digital says trading so far in line with co's expectations

- Tesco agrees sale of property sites for £250m

- Rank Group says confident in group's prospects for year

- Booker says trading in 4 weeks of H2 ahead of last year

- Gulf Keystone receives $12m for Kurdistan oil

- Ashmore assets under management drop by $7.8 bln in Q1

- WHSmith proposes £50m share buyback after profit rise

- Arbuthnot Banking sees FY results in line with market consensus