Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

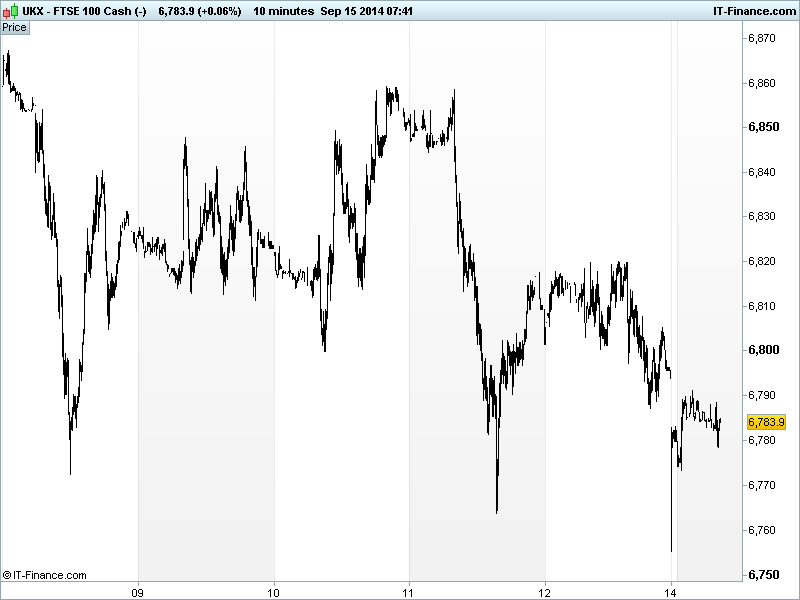

UK 100 called to open -20pts at 6780 after a weak close in the US on Friday offset a neutral European finish, as traders weighed up the prospect of a more hawkish rhetoric from the US Federal Reserve this week (interest rates to rise sooner than expected?) following some strong data stateside (consumer confidence, retail sales, UoM) and geopolitics continued to weigh heavily.

Asia bourses have started the week on the back foot following disappointing weekend data out of China, with Industrial Production slowing to its lowest level since 2008 and both Retail Sales and Fixed Asset Investment supporting ‘hard landing’ fears, adding to last week’s growth uncertainty and giving PM Li little choice but to simulate or miss 2014’s growth target even if he has distanced himself from the former of late.

Japan’s Nikkei outperforming thanks to PM Abe saying he had not decided on a second sales tax hike, while the strong USD (in anticipation of a change in Fed rate rise talk) has helped maintain JPY weakness giving Nikkei exporters a helping hand.

In geopolitics, there have been reports of heavy shelling in Eastern Ukraine despite the supposed 5 Sept ceasefire, which maintains tensions between Russia and the West. The US says several Arab nations have offered support in the bombing of Islamic militants in Iraq and potentially Syria, while yet another disturbing video from ISIS this weekend will add fuel to the fire.

Closer to home, the Scottish referendum still looks too close to call as saw both sides used the final weekend to drum up support while fear of the unknown/uncharted territory sees some traders adopt either a risk-off or wait-and-see attitude ahead of Thursday’s vote and Friday’s early morning result regarding the impact on some of the most traded London-listed equities with exposure north of the border and of course the pound.

UK Housebuilders could benefit from overnight Rightmove House Price data showing a jump in September after traditional contraction in August (buyers in holiday-mode) and “early signs of a bounce-back in demand after the summer lull”.

The UK 100 is off its worst levels of Friday night (6755) but remains in a corrective phase since making new 14yr highs (just) of 6905 at the beginning of the month, which could swiftly be revisited on any bullish revival. Support available again at 6750, but thereafter one must look back to August lows close to 6500.

The focus today will be on data which will go to either calm or intensify existing fears of an earlier Fed rate rise with US Empire State Manufacturing seen improving, while US Industrial Production is seen cooling a touch despite improved capacity use, and Manufacturing Production taking a breather from growth in August.

In commodities, prices fell to their lowest in more than five years on signs of weakening demand in China and on speculation that a rise in US borrowing costs is just round the corner. Gold has found a modicum of support above 2014 lows of $1216 on hopes of bargain hunting and some renewed safehaven seeking ahead of the Fed meeting this week. It’s a similar story for Silver with some support around 14-month lows of $1824.

In oil world, both US and Brent crude declined for a second day as China data lead to expectations of slowing growth and reduced demand taking the edge off any implied premium for geopolitical risk.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- CN Industrial Production Miss, growth slowed

- CN Retail Sales Miss, growth slowed

- UK Rightmove House Prices Growth accelerated

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Spirent buys Danish mobile analytics company Mobilethink

- Greggs sees full-year profits ahead of expectations

- Mwana Africa comments on Zimbabwe's gold royalty rate reduction

- Micro Focus agrees all-share merger with The Attachmate Group

- TUI Travel, TUI AG reach agreement on 6.5 bln euro merger

- Monitise sees full-year 2015 revenue growth of at least 25 pct