Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

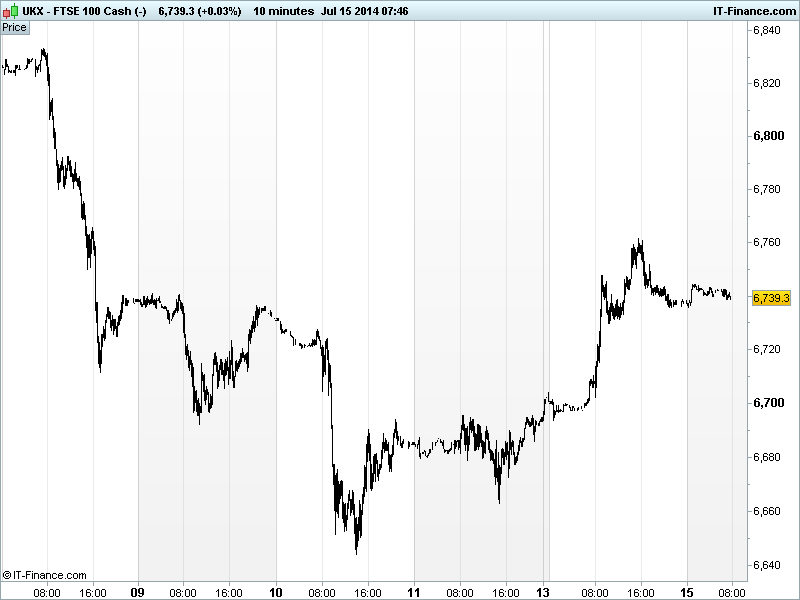

UK 100 called to open -10pts at 6740, taking a breather after a 120pt bounce from 6640 support despite US markets closing around 0.5% to the good, rebounding from their biggest weekly drop since April and remaining within touching distance of recent all-time highs.

US bourses helped by better than expected Q2 results from Citigroup (excl. legal charges) boosting financials, M&A news continuing to flow, Goldman Sachs upping its year-end call for the S&P500 (2,050 vs 1,900 prev) and EUR/USD weakening despite ECB President Draghi saying economic risks remain to the downside with EUR strength threatening a sustainable recovery. Portugal also seen continuing financial woes.

Asia-Pacific largely positive overnight, following the US lead, even if the BoJ policy statement and minutes from the RBA failed to inspire. Australian shares end a three-day winning streak due to declines in banks after a government-backed financial system inquiry raises concerns about capital adequacy for so-called systemically important banks.

Traders look to be awaiting, 1) more insight into US monetary Policy from Fed Chair Yellen’s Senate testimony this afternoon, hoping she will continue to support easy policy despite economic improvements, and, 2) the China data dump on Weds morning, although optimism is rife thanks to US earnings season so far surprising to the upside which, with equities deemed fully valued, is likely to be to be the next market driver.

Overnight data failed to excite with UK BRC Sales falling as consumer worries about the prospect of higher interest rates were cited as the dampening factor, with continued weakness in food sales due to a supermarket war and an early England exit from the World Cup.

China June refinancing and money supply was generally better than expected (PBOC supporting growth) but Foreign Direct Investment barley grew. Markets more focused on China’s GDP update tomorrow morning.

In focus today we have UK inflation data where CPI is again seen weak in June even if the annual rate and Core are expected to have ticked up. PPI is seen rebounding while RPI goes flat on the month and UK House Prices rise 10% over the year. German ZEW surveys are forecast to have moderated in July.

In the afternoon, US Empire State Manufacturing is seen lower in July, while US Retail Sales rebound in June and US Business Inventories deliver the same growth in May as in April. After Citigroup yesterday, it is the turn of JPMorgan and Goldman Sachs to report Q2 results around midday and Yahoo and Intel after the US close.

In commodities, Gold has continued its retreat, near its biggest drop in almost seven months with positive data - economic and corporate – reducing demand for the safehaven and low inflation negating desire for it as a hedge. Support at $1305 as highlighted yesterday, helped by speculation the recent decline may spur demand as holdings in the largest exchange traded product (SPDR) expanded to their highest levels since April.

Oil found a bit of support near 2-month lows ahead of US inventory data which may signal the strength of fuel demand in the US. The forces of potentially higher supply still influencing but markets less worried about supply disruptions in the Middle East.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK BRC Like-for-like Sales Miss, deteriorated

- JP Monetary Policy Unchanged

- AU New Motor Vehicle Sales Improved

- CN Money Supply/Financing Improved

- JP Machine Tool Orders Solid

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- GVC raises quarterly dividend

- API Group says CFO Chris Smith to resign

- Michael Page Q2 profit up by 8.9 percent

- Independent News & Media appoints Robert Pitt as Group CEO

- McBride names Chris Smith chief finance officer

- Bowleven ends strategic alliance agreement with Petrofac

- Utility firm Telecom Plus says customer base rises 15 pct

- Dragon Oil sales rise 4pct in first half of year

- Dairy Crest says outlook for full year remains unchanged