Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

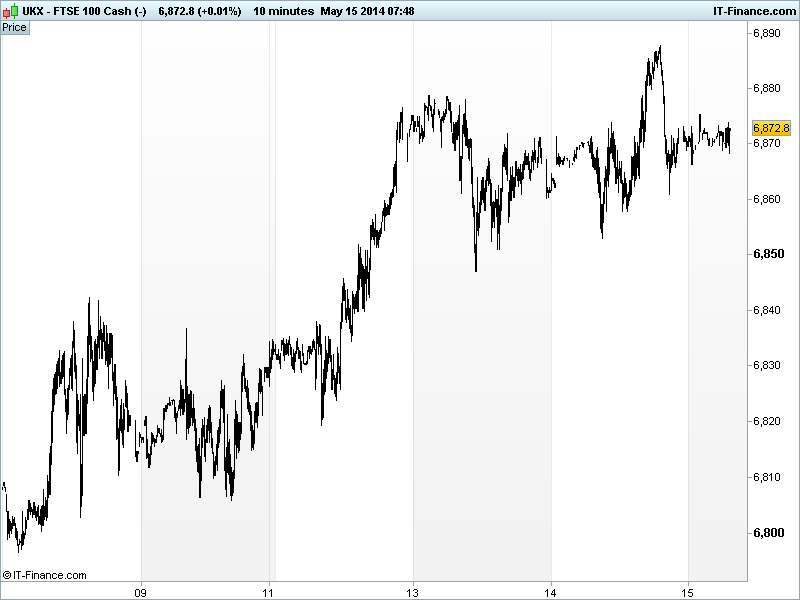

UK 100 called to -5pts at 6870 after US stocks came off their all-time highs to close lower as home-building and bank shares weighed on the broader markets and as the sell-off in small-cap and Internet names resumed. Note, however, Cisco Systems (bellwether for tech spend) shares up after hours thanks to smaller Q3 losses and an outlook which beat consensus, and the Ukraine situation showing little signs of improvement.

Losses in Europe small yesterday thanks to the Bundesbank’s Weidmann saying he would support ECB action if needed and that the bank would have acted in May had it been necessary but not every measure being discussed is suitable (QE?). Is he following Draghi and prepping us ready for June too?

Overnight, Asian stocks mixed with Japan’s Nikkei in the red due to Q1 GDP picking up so quickly. Consumers and companies likely brought forward spending ahead of April 1 sales tax hike, which could lead to a weak Q2. Nonetheless, expectations of a stronger economy and less need for stimulus strengthened the JPY, hurting equities, while corporates including Sony and financial Sumitomo Mitsui forecast weaker earnings.

Data overnight showed Japanese Q1 GDP going from breakeven to +1.5% QoQ growth and the annual rate from 0.3% to an incredible 5.9%. This along with the JP Tertiary Industry index in Mar rebounding more than expected and consumer confidence not deteriorating as much as expected in April. Aussie New Vehicle Sales were flat versus a decline in March.

In focus today we have more GDP from the Eurozone, after France and German delivered a Q1 miss and a beat respectively, even with the bar set pretty low for the former, as consumers tighten their belts and companies cut back on investment. Italy is up next at 9am before the Eurozone regional figure at 10am, along with its all-important CPI which could force the ECB to act with stimulus in June.

In the afternoon in the US, Weekly Jobless Claims are seen relatively unchanged after last week’s bigger than expected improvement. CPI for April is expected to have improved to 2.0% annual, taking the heat off the Fed a little with it back at target. Empire State Manufacturing is forecast to jump to a 4-month high in May, while Industrial Production is stagnant in April, the Philly Fed drops back a bit and the NAHB housing index ads 2 points.

The UK flagship index tried as high as 6888 late yesterday, beating Feb’s highs briefly although we are back at the 6870 level around which we oscillated yesterday. The rising lows of the last month are still valid and the appetite for risk is helping us grind on towards those all-time highs of 6950 from end-Dec 1999. More speculation of ECB and China stimulus could help. Weak GDP or CPI from the Eurozone this morning?

In commodities, Gold back up above $1390 level at a 1-week high, thanks to some analysts seeing safehaven buying due to Ukraine worries offsetting US optimism and the potential for stimulus measures in Europe.

US Light Crude off its $102.6 3-week highs after US inventories expanded as production increased to a 28-year peak. Brent Crude has gained to $110.2, last seen end-April supported by continued geopolitical uncertainty.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- JP GDP Beat, better rebound

- JP Tertiary Industry Index Beat, improved

- AU New Vehicle Sales Improved

- JP Consumer Confidence Beat but deteriorated

- FR GDP Miss, deteriorated

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Pub group Marston's posts 9.4 pct rise in first half profit

- Trinity says 2014 tracking in line with expectations

- Ophir Energy says to drill 10 wells before year end

- Restaurant Group upbeat on first half trading

- Dixons sees full-yr profit at top end of expectations

- Tullow, partner find oil in northern Kenya

- Rank Group sees operating profit hitting target

- AstraZeneca highlights oncology pipeline at ASCO

- London Stock Exchange sees 50 pct rise in revenue

- Kier named preferred bidder for 130 mln stg Anglian Water contracts

- Soco says production levels in line with expectations

- Aviva sees volatile life business in UK

- UK's Dixons and Carphone agree 3.8 bln stg merger

- Gold miner Centamin Q1 core profit falls as production shrinks

- Great Portland Estates JV lets space at 240 Blackfriars to Ramboll

- Hikma raises operating margin forecast for injectables unit

- JKX Oil & Gas says Q1 gas production rises to 55.2 mmcfd

- Informa's organic revenue rises 0.6 pct for first four months of 2014

- National Grid posts rise in full-year profit, increases dividend

- Premier Farnell's sales per day rises 2 pct year on year

- Card Factory prices IPO at 225 pence