Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

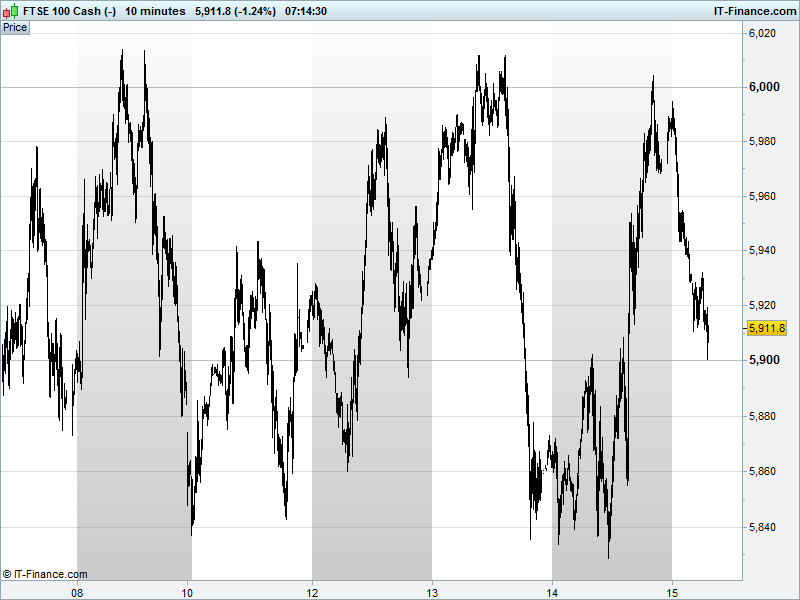

UK 100 Index called to open -10pts at 5910 having sold back from another test of 6000 to keep us in a 7-day sideways range 5850-6000. That JPMorgan call to sell any rallies is proving profitable so far. Potential for support at 5900 via highs of early yesterday. Note, however, equal potential for this sideways move to be consolidation before either a rebound or another leg down to continue the downtrend from April 2015 all-time highs. Watch levels: Bullish 5935, Bearish 5890.

The negative opening call comes after another retreat by Asian equities to 3yr lows from early US-inspired gains as Oil turned on its heels to fall back below $31/barrel retracing a significant portion of its recent rebound. Regional energy stocks were held back by continued US dollar strength and China/global growth anxiety. Once again, same old, same old.

Chinese bourses extended losses to their longest losing streak since Oct to join the bear market party, despite another flat Yuan fix, with some banks refusing small cap stocks as loan collateral. New credit jumped to its highest since June adding to fears the nation is overstretching itself, heading towards crisis as the government tries to avoid an economic hard landing amid slowing growth.

US equities closed in positive territory yesterday - yet again, talk of ‘oil price strength’ graced us with its presence as WTI crude prices recovered a staggering $0.72/bbl - but this morning sees futures lower once again as oil prices resumed their slide. We heard from the Fed’s Bullard, who said that the resultant decline in inflation expectations is becoming worrisome such that neither the FOMC nor the markets are entertaining thoughts of a January rate rise while March remains up in the air (unlikely in our view - things will have to pick up significantly very, very soon for a March hike).

Corporate-wise headwinds include a poor set of results from Intel (INTC) as Q4 fourth-quarter EPS fell 1% amid continued weakness in the PC market. BHP Billiton (BLT) highlighted sector woes and global oil supply glut problems with a mammoth $7.2bn write-down on US shale oil assets. Could a dividend cut be next? Oh and Goldman Sachs (GS) has taken a $5.1bn hit for its handling of US mortgage-backed securities, reminding us of the initial financial crisis.

In focus today we have only US data with Retail Sales for December seen dipping, similar to what we saw in the UK, with warm weather hindering winter clothing purchases and after a successful Black Friday. US Producer Price Inflation is also seen easing, adding to the arguments for the Fed to hold off from hiking again too soon. Industrial Production is also seen weak, albeit less bad than November, along with Business Inventories while Consumer Confidence is expected flat. Fed speakers include Dudley and Kaplan.

Iranian sanctions due to be lifted imminently should put more pressure on Crude into the weekend, as if the Chinese slowdown and a stubborn OPEC (sorry, that should read Saudi Arabia) aren’t enough. At best we could see yesterday’s breakouts above falling highs maintained but with down trending support. At worst, a break down into the $20s.

Gold is naturally benefiting from renewed China worries overnight. The yellow metal did retreat to $1071 as indicated yesterday, as equity markets rose into the close, but has bounced off that level as futures retreat, keeping the 2.5-month rising channel intact.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- UK's FCA temporarily suspends Telecity Group shares pending announcement

- Credit checker Experian expects foreign exchange hit

- BT says £12.5bn EE deal to close on 29 Jan.

- Fiat-Chrysler Automobiles Sales in Europe December and FY 2015

- Bovis Homes Expects Significant Rise in 2015 Revenue, Pretax Profit

- Moneysupermarket.com Sees Strong 2015 Results; Well Placed

- Clydesdale Bank says latest quarter trading in line with expectations

- John Lewis weekly dept store sales up 15.6%