Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

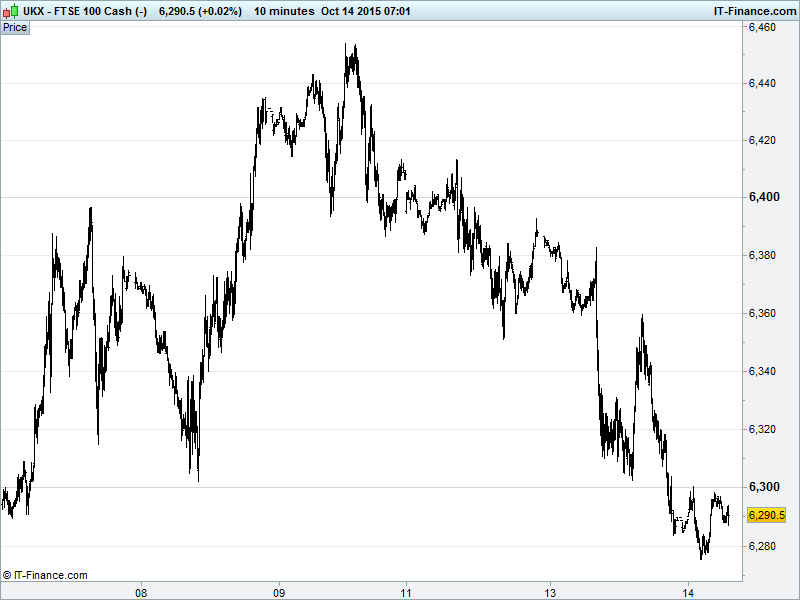

UK 100 Index called to open -50pts at 6290, now below the 6300 breakout level of last week. This extends the declines from 6450 where time was called on a 10% rebound rally from September lows. The breach of 6300 means we could see extension of this week’s weakness within a falling channel. however, with the 50% Fibonacci retracement of the April-Aug decline serving as resistance at 6450, there is potential for 38.2% to prove supportive at 6285. Updated watch levels: Bullish 6340, Bearish 6270.

The negative opening call comes as China makes it two days in a row for bad macro data and US Q3 results failed to inspire. While Chinese consumer inflation (CPI) slowed further , Producer Prices made it a record 43rd straight month of deflation. While inflation gives the PBOC room to ease monetary policy further to support the slowing economy, hopes of more stimulus are clearing failing to appease market concerns especially with Q3 GDP data only days away (Monday morning).

Add to this Q3 results disappointment from banking behemoth JPMorgan (JPM) and tech giant Intel (INTC), dented by poor trading revenues and a weak global PC market, respectively, and cautious/muted outlooks from both, and we have the recipe for a weak start in Europe as market fears are proved justified with financial results missing even downwardly revised guidance going into earnings season.

Asian stocks in the red, but to differing degrees with Japan underperforming (-2%) on continued weak China factory gate data and the implications for global trade but China and Australia (the former’s biggest trading partner) holding close to breakeven on bets for more PBOC policy assistance to fight deflationary risks.

US Stocks closed lower amid China concerns and earnings season worries which proved justified while Fed talk spiced up the rate rise debate with a couple of members becoming more vocal in their dissent towards a hike.

In focus today we have French and Spanish CPI adding to Eurozone deflationary woes while UK Employment data is seen positive with stable unemployment and wage growth accelerating to >3%. Eurozone Industrial Production expected weak in August.

In the afternoon, US Retail Sales and Business Inventories solid but Producer Prices weak adding to absent inflation calls to leave Fed rates unchanged a while longer. The US Beige Book update in the evening gives us the latest assessment of the US economy on a regional basis.

Gold has hit a 3-month high of $1172, breaking above August highs of $1170 on renewed China stimulus hopes, a weaker USD and continued Fed uncertainty as to the timing of a rate rise, coupled with persistent concerns about global growth and of course a slowing China for which the data of the last 2 days does little to offset. This break at $1170 could be enough to finally say farewell to the 8-month downtrend which had hindered the yellow metal.

Oil trades around a 1-week low, with Brent continuing to test the $50 mark above which it broke last week. The weakness comes ahead of US data expected to show stockpile expansion, more poor China data questioning global demand and negative OPEC comments (glut will persist through 2016) countering the bullish commentary (expect price spikes) of last week.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Hargreaves Lansdown says assets fall £500m on stock market flux

- Diageo sells US, UK wine interests for $552m

- Intertek buys US testing firm PSI for $330m

- UK's Domino's Pizza Group sees upbeat full-year results

- Just Retirement gets 34.5% acceptances for share offer

- Capita agrees to buy Xchanging for £412m

- Equiniti to raise £315m pounds in London IPO

- N Brown says confident of full-year outlook