Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

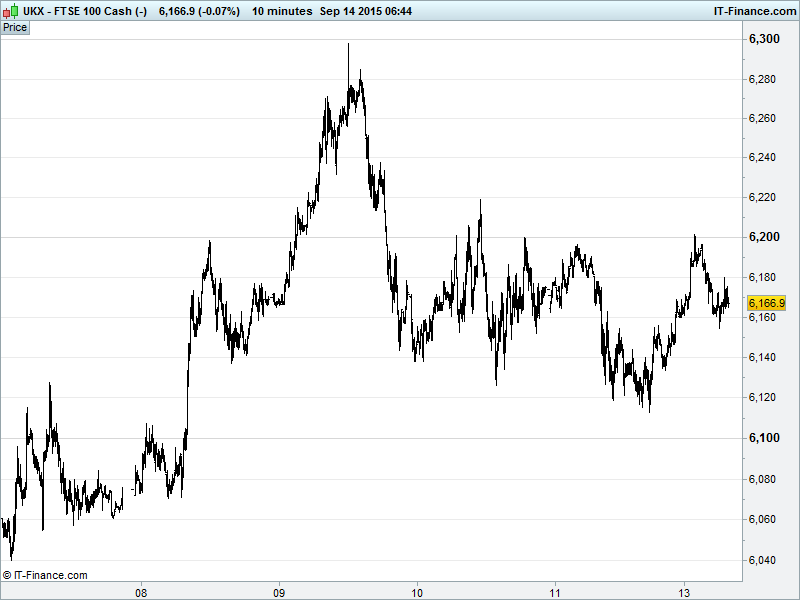

UK 100 Index called to open +35pts at 6145, but down from overnight highs of 6200 after the level served as resistance for a third consecutive day. The index is at a 6115 crossroads with rising lows from Aug 25 keeping the uptrend alive but the intersecting trend-line from Aug 28 ushering the index lower. Which will prevail? The limited upside progress at 6200 suggests downside risks. Updated watch levels: Bullish 6230, Bearish 6110.

The positive opening call is despite a largely negative session in Asia to start the new week following another bout of moderate US gains on Friday as the odds of a Fed Rate hike lengthen but uncertainty remains rife (USD weaker) and after yet more unconvincing Chinese data over the weekend serves to hamper already tapered risk appetite.

Chinese data for August was mixed with Retail Sales surprising to the upside, suggesting domestic confidence, but Industrial Production only improving slightly from July and Fixed Asset Investment growth slowing suggesting slowing global demand. It’s looking tougher to hit that 7% GDP growth for 2015 but be prepared for the propaganda machine to be working overtime come September’s update, when of course all will be deemed rosy.

Japan’s Nikkei in the red after Industrial Production slowed in July, a weaker USD meant a stronger JPY and the prospect of slower growing China continues to bite. While Chinese equities are also negative this is despite hopes of more stimulus, something which is helping Australia’s ASX (China is its biggest trading partner) which is also higher on a softer AUD from the prospect of political leadership change.

US equities posted a positive session on Friday while futures currently down a little with investors digesting poor Chinese Data as a brief aside to anticipation of Thursday’s FOMC meeting which is nonetheless likely to keep things muted in the first half of the week. As always, a decision on a US interest rate rise is expected to come down to the wire, but it’s not the type of decision to be made either hastily or in the absence of majority consensus within the US Central Bank, and therefore a delay until at least the next meeting (October) seems probable (maybe even December).

Data on Friday showed US consumer sentiment hit its lowest in a year in early September and producer prices were flat in August, signalling moderate economic growth and tame inflation that could weigh on the Fed's decision whether to hike interest rates. The jobs part of its dual mandate is fine, but inflation is clearly missing and external factors just can’t be ignored. Note also that central banks in the Eurozone, Sweden, Canada and Australia among others have tried to raise their own interest rates in recent years, only to backtrack and cut them again as their economies stumbled, something the US Fed will be none too aware of.

In focus today will be the fallout from the China data and Thursday’s Fed Update (hike or not?). Thereafter it’s quiet on the macro front with data limited to Eurozone Industrial Production for July which is seen improving.

Crude futures still suffering from global oversupply (Brent $48, WTI $44) despite fewer operational US drilling rigs (a la Baker Hughes Rig Count) with a drawdown in demand offsetting any perceived drop in supply. Goldman Sachs estimates Oil could fall to as low as $20 a barrel in order to clear out stockpiles. Support in the form of a weaker USD as markets increasingly expect no move on US interest rates also balanced by the underlying reasons for that – emerging markets concerns and volatile equity markets.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Russia's Global Ports H1 net profit down 62 pct y/y

- Trinity Mirror in talks to buy Local World Holdings

- Intertek Buys Denmark-Based Quality Assurance Firm DIC