Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

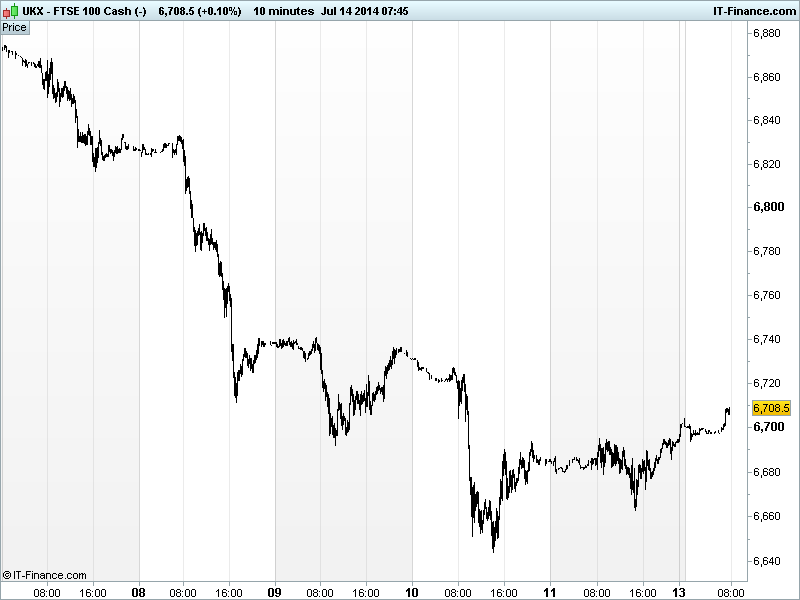

UK 100 called to open +25pts at 6705, after Asian stocks continued to rebound from last week’s jitters about Portugal and its struggling bank Espirito Santo (missed a debt payment) reviving the Eurozone debt crisis, a faltering Eurozone recovery thanks to weak data, rekindled fears of equities being overvalued and continued geopolitical risk with fighting in Ukraine, Libya, Iraq and Israel.

Investors are looking ahead more positively to the new week though, hoping major data releases from Europe, the US and China can restore confidence and put last week’s woes behind them. Japan has already helped out with upward revisions to its May industrial Production prints.

US stocks closed slightly higher on Friday, ending their worst week since April, with investors less worried about the chance of a corporate debt crisis in Portugal and interpreted Fed chatter positively - Lockhart saying he wants more time to see if US inflation goes to 2% and Plosser saying the FOMC is closer to hiking rates than the markets think. The rate debate on the timing of a rise continues.

Note the Portuguese PM playing down the risk of a crisis at Banco Espirito Santo and Portugal as a whole, especially after exiting the bailout programme, as well as Russia threatening retaliation after shelling by Ukraine left one dead. There may be more RU-UKR crisis talks with Russia and Germany today.

In focus today, we have Eurozone Industrial Production at 10am which will be keenly watched given the weak readings by France and Italy last week which added to investor fears. Thereafter its quiet until ECB President Draghi speaks at 6pm.

After US bank Wells Fargo reported Q2 results last week, be aware of Citigroup reporting today - the US banks can have a real knock-on for UK banks – and peers (GS, JPM, BoA, MS, BoNY) reporting all through the week. We also have and American Airlines, which will be of interest in terms of US consumer/business spending and following the profits warning by Air-France-KLM.

For the rest of the week watch out for UK June Inflation, US Retail Sales and Fed Chair Yellen’s testimony to congress on Tuesday followed by China Q2 GDP, Industrial Production and Retail Sales, UK Unemployment and US Production on Wednesday. The China readings could well be the driver for the week after stronger export data last week. Thursday sees an update to Eurozone Inflation and US Housing which Friday closes with an update on US Consumer Confidence.

On the M&A front, after Shire was the top riser on Friday, note AbbVie revising its proposal and making a fifth offer of 5320p/share.

In commodities, the price of Gold has continued to slip back from its $1345 4-month highs (Silver following suit) as investors temper their safehaven demand derived from last week’s fears and ahead of a heavy economic data and earnings slate for the week starting tomorrow. Support still possible around $1305. Oil still under pressure from the prospect of higher supply and muted demand as well as the threat of supply disruptions in the Middle East abating.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- AU Credit Card data Positive

- JP Industrial Production Revised higher

- JP Capacity Use Less weak

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Shire confirms in talks with AbbVie on takeover bid

- easyJet selected CFM as engine supplier for new aircraft

- Quindell H1 revenue rises 117 pct

- SThree H1 gross profit at 100.8 mln stg

- Sports Direct to launch in Australia, New Zealand with MySale

- AIB appoints Co-Op bank chairman

- TT Electronics to buy Roxspur Measure & Control