Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

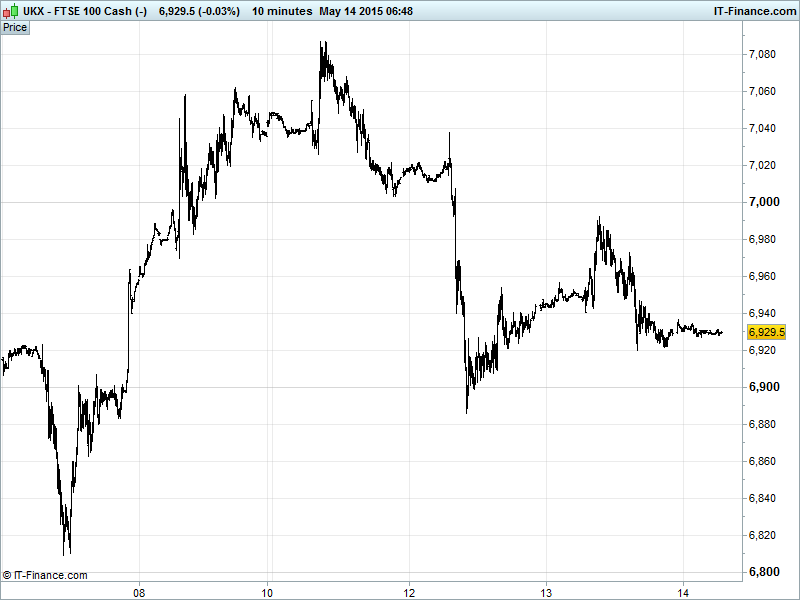

UK 100 Index called to open -30pts at 6920, having traded sideways overnight into the apex of a narrowing triangle pattern which normally serves as consolidation before a continuation of the prior trend. The 100-day moving average continues to hold at 6910, with Bulls still eyeing a return to the highs and the Bears a drop back to a more bargain-like level. Note many Euro bourses closed or likely to trade thinly due to Ascension day holiday. Watch levels: Bullish 6960, Bearish 6880.

The negative opening call comes as the UK’s benchmark index pulled back in futures trading overnight following an impressive rally on Wednesday as UK 100 corrected upwards, gaining 0.2% supported by Mondi and Hargreaves Lansdown shares, the latter having been volatile of late in the run-up to its trading statement on 20 May, and positive macro data in the form of the lowest Q1 unemployment rate since 2008 and a rebound in wage growth. Shares in Compass Group footed the index, posting their biggest losses in 10-months.

US bourses lacked direction for much of Wednesday. Disappointing US macro data led to a considerable pullback in the Dollar Basket and several financial institutions revised down their Q2 GDP estimates for the world’s #1 economy. Euro-worries took the form of ECB concerns surrounding the relationship between Greece’s government and its central bank where comments have been noted that appear to be challenging its independence under EU law. Greece fell back into recession in Q1.

Asian stocks in the red after a choppy/breakeven US session with the global bond slump continuing (prices down, yields up) in response to pending monetary policy normalisation. Asian equities hindered by regional FX strength as the USD index dropped to near 3-month lows on weaker than forecast US data (retail sales, import prices, business inventories) which compounded recent US data misses, raising concerns about the US economic outlook and further pushing back rate-rise expectations.

Japan’s Nikkei underperforming on a strong JPY/weaker USD as well as a raft of soft corporate earnings reports. Australia’s ASX bucking a 2-day rally as healthcare names send it lower while Hong Kong’s Hang Seng is underwater as Chinese markets trade mixed on poor lending data on the heels of yesterday’s Retail Sales and Industrial Production disappointments, even if both justify recent stimulus intervention.

In Focus today we have US Jobless and Continuing Claims, indications showing a rise in the number of people out of work. PPI looking largely flat, adding to worries from recent weak data that Q2 may not be as strong as many were anticipating and the US might not be ready for interest rate rises just yet.

Brent Crude ($65) may be settling into a sideways channel as it continues to trade just short of 2015 highs. A similar story for US Light ($60). Potential for yesterday’s breakouts from triangle patterns to lead to continuation of uptrends for both benchmarks, while a multitude of drivers in the form of recent data indicating a fall in US stockpiles for the second straight week while the global market remains oversupplied. Meanwhile, US Shale producers are ready to bring their rigs back online amid a supposed oil price recovery. Such mixed sentiment is creating volatile trading conditions with US reserves still about 90mn barrels higher than they were at this time last year while the second biggest US oil producing state, North Dakota, surprised to the upside with its output report.

Gold is back trading around recent $1215 highs thanks to USD weakness (metal cheaper to non-US buyers) driven by poor US data which accentuated questions over the strength of the US economic recovery. Concerns still abound regarding Greece, with the ECB questioning Greek central bank independence given the pressure from Athens and German Finance Minister supporting the idea of a Greek referendum. Support $1200, Resistance $1225.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK RICS House Price Balance Beat, improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Lookers says on course to meet FY expectations after profits boost

- Merlin Entertainments posts Q1 revenue rise

- Mitchells & Butlers posts 4.1 pct first half profit rise

- Vedanta Resources says FY EBITDA fell 17 pct

- British Land says NAV jumps, raises dividend

- British Land full-year EPRA NAV jumps 20.5 pct

- Old Mutual Q1 gross sales beat forecasts, up 18 pct

- Hikma reiterates 2015 forecast

- Digital Realty Trust says not to make offer for Telecity

- Growing supply to keep pressure on iron ore prices - BHP Billiton

- Keller expects FY results in line with market expectations

- Lower iron ore, oil prices hit Vedanta full-year core profit

- IP Group says to take stake in Oxford Sciences Innovation

- TalkTalk lifts revenue forecasts after strong 2015 earnings rise

- Stobart says FY revenue from cont ops rises 17.6 pct

- Vesuvius says revenue down 2 pct in the first four months of yr

- Restaurant Group sees trading momentum building in second half

- Aggreko reaffirms full year trading profit expectations

- UK private equity firm 3i sees strong returns on portfolio earnings growth

- Aldermore Group Q1 net lending rises 7 pct

- Building materials supplier SIG keeps 2015 outlook

- Balfour Beatty reaffirms cash target of 200 mln stg

- Alliance Trust unit buys stockbroking business from Brewin Dolphin