Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

UK 100 called to -5pts at 6865 after US stocks closed mixed following disappointing US retail sales which fed speculation of slower economic growth holding back inflation, and investors monitored the situation in Ukraine. The DJIA made a marginally improved record high while the S&P500 closed just below its test of the record 1900. The Nasdaq tech slide resumed, led by Cisco which reports tonight.

Asian equities have seen Japan and Australia follow the US lower, the former despite decent inflation data and possibly waiting for results from the likes of Sony and the latter weighed down by banks going e-div and after the budget. Hong Kong benefiting from reports of a potential relaxation of double stamp duty on second home owners and PBOC told lenders to expedite home loans.

Japan lower despite a decent Domestic Corporate Goods Price Inflation print and improvement in Machine Tool Orders. Note the German CPI confirmed as negative in April which will add to the weight of expectations that ECB President Draghi needs to pull the stimulus trigger next month, although the annual rate did improve.

Note the Euro’s weakening yesterday after poor ZEW surveys and a WSJ report that the Bundesbank would support ECB easing if inflation forecasts are lowered. The IMF’s Lagarde also said Eurozone inflation too low.

In focus today, we have CPI from France and Spain which will be used along with this morning’s German reading to gauge the situation in the Eurozone region as a whole and allow traders to update their bets on whether the ECB will indeed be forced to intervene next month (rate cut? QE?) to stave off the current disinflation/deflation.

The UK’s quarterly Inflation report from the BoE will be keenly watched for any updates on a rate hike, with the Telegraph suggesting this morning that Governor Carney will give a clear signal rates will rise before the 2015 election, with tightening endorsed from Q1, three months earlier than expected.

UK Jobless data for April is seen improving a notch again this month with the claimant count and ILO unemployment rate falling by a basis point with stable additions to employment over the past 3 months. Eurozone Industrial Production is seen weaker in March, following the recent trend we saw in Germany. In the afternoon, April US Producer Price Inflation is expected to have slowed both at the headline and core.

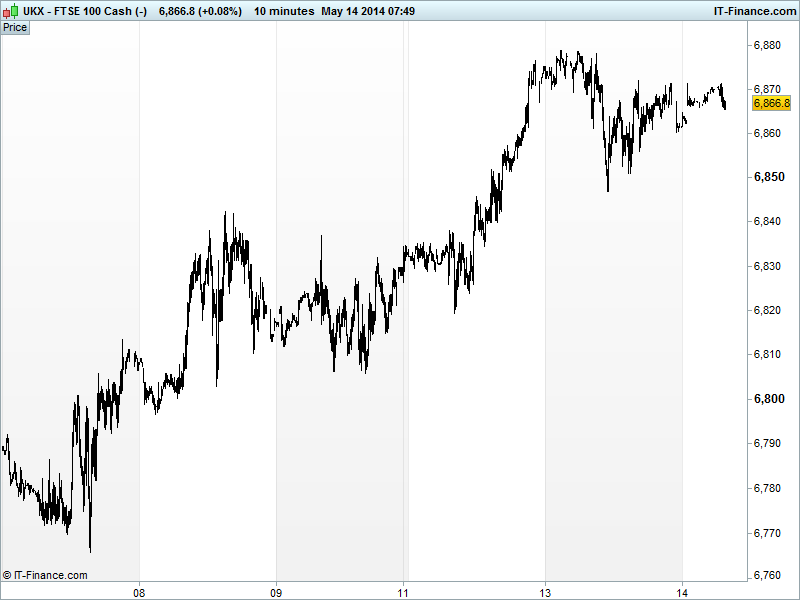

The UK flagship index almost made it to Feb and 2014 highs of 6886, finding resistance around 6878. Support still valid around 6840. Equities holding up around recent highs thanks to hopes of ECB stimulus, and China's disappointing manufacturing and property data reveal fresh signs of weakness that could pressure Beijing to prop up the economy. All eyes still in the index making a record high like its US peers.

In commodities, Gold still to-ing and fro-ing around the $1290 level thanks to geopolitical worries from Ukraine and uncertainty about global growth, but safehaven gains hindered by continued shrugging off of macro concerns and appetite for risk benefiting equities.

US Light Crude rallied up to recent highs of $102, advancing for a third day, the longest rising streak in more than three weeks, after a report showed stockpiles fell at the biggest U.S. oil-storage hub. Brent Crude also up above $109 supported by geopolitical risk.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- JP Domestic CGPI In-line, Improved

- JP Machine Tool Orders Improved

- DE CPI In-line, deflationary

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- BHP Billiton in talks to sell Australian nickel business

- Lookers sees full-year results ahead of forecasts

- Broker ICAP sees 4 pct fall in pretax profit

- Renishaw Q3 revenue increases to 84.5 mln stg

- S.Africa's NUM says intimidation preventing Lonmin return

- Caterer Compass hands back 1 bln stg to shareholders

- Ultra Electronics says Forensic Technology deal gets U.S. approval

- Galliford Try upgrades profit forecast on housing boost

- Britain's 3i completes $1.13bn exits in FY

- Premier Oil production rises on strong UK, Vietnam output

- Galliford Try upgrades profit forecast on housing boost

- Gulf Keystone lifts Shaikan forecasts, revenue outlook uncertain

- AstraZeneca and Incyte to study cancer drugs together

- British Land NAV jumps 15 pct as UK property market recovers

- UK motor insurer Admiral's turnover dips in first quarter

- ITV sees second-quarter advertising boost from World Cup

- Wood Group maintains 2014 outlook on strong North Sea, US shale demand

- Centrica drills dry wells in Norwegian North Sea

- Catlin Q1 gross premiums written rise 9 pct