Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

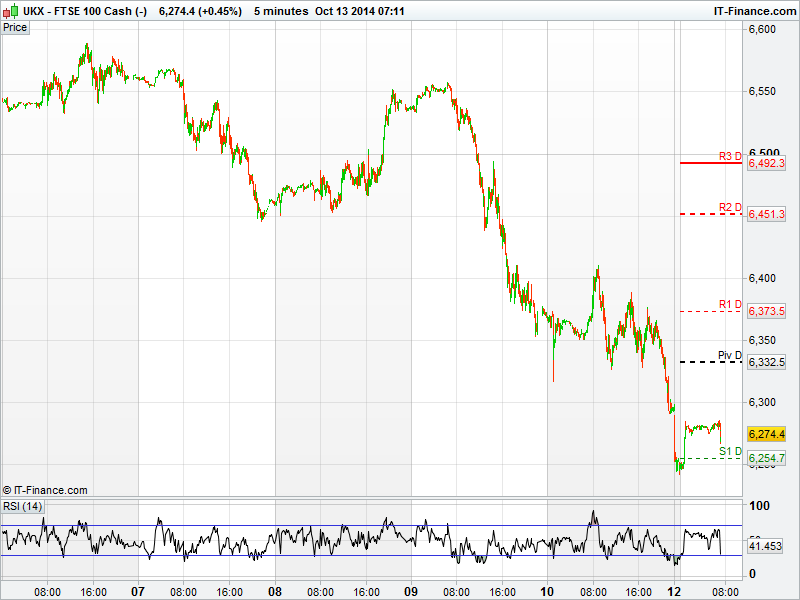

The UK 100 Index is called to open down by 68pts as it appears the rout on stocks is not yet finished.

The UK 100 closed lower by 92pts on Friday as the market failed to shake of concerns of a global slowdown. The UK 100 has now lost 620pts in less than a month.

Tullow Oil (TLW.L) led stocks lower, closing in the red by 7.88% - the market unconvinced by the company's "encouraging results" from early drilling activity at its well off the shore of Gabon.

Commodity related stocks were obvious victims, often hit when economic growth is questioned. Antofagasta (ANTO.L), BHP Billiton (BLT.L) and Glencore Xstrata (GLEN.L) represented the worst performers in the sector having recorded losses between 3-4% for the session.

Travel companies continued to decline on concerns the deadly Ebola virus could be spreading. Shares in TUI Travel (TT..L) lost 3.5% while Carnival (CCL.L) and International Consolidated Airlines (IAG.L) both lost 2.5%. EasyJet (EZJ.L) bucked the trend closing the session higher by 0.5%, the City seemingly prepared to take advantage of the 14% decline witnessed in the preceding days.

The travel sector is likely to be in focus once again today with a new case of Ebola reported in the US over the weekend.

US markets closed lower again. The Dow Jones lost over 100pts and is now almost 900pts lower in just a month, currently trading at 16,463pts and in negative territory for the year. The S&P 500 fell over 1% to close at 1,906pts which will have technical traders glued to the screens watching for a bounce off of the 200 day moving average at 1905pts.

Tomorrow represents an important day for the US reporting season as the first of the US banks deliver trading updates. Citigroup, Wells Fargo and JP Morgan will publish numbers late morning (GMT). Watch for reactions in UK listed banks as a result.

Asian markets continued to trade lower across the board as global slowdown fears meant they followed US peers. The Nikkei led the way down by 1.1%, with the Hang Seng down 0.7% as traders came out of shares into sovereign bonds. The MSCI Asia Pacific index was on course for its lowest close since March this year.

In commodities, as the equity rout continued gold advanced to a four-week high trading at $1235. Gold has gained 2.7% since last week which was its best weekly gain since June. WTI followed Brent Crude and fell into bear market territory having falling more than 20% since its peak in June, trading as low as $84.25 a barrel.

In FX the yen hit four week highs against the dollar on its appeal as a safe haven currency, trading at 107.20 per dollar having rallied 2% this month alone.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- CH Trade Balance Worse

- CH Exports Better

- CH Imports Better

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Essentra Q3 revenue rises 8 pct

- Smith & Nephew ulcer therapy fails to meet primary endpoint

- Hikma Pharma says in partnership with Eisai for epilepsy treatment drug

- Publicis to buy 20 pct of digital ad group Matomy

- Quindell Q3 revenue rises to 198 mln stg

- UK Rough gas storage site undergoing unplanned outage-Centrica

- Oxford Biomedica buys Windrush Court Office for 3.2 mln stg