Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

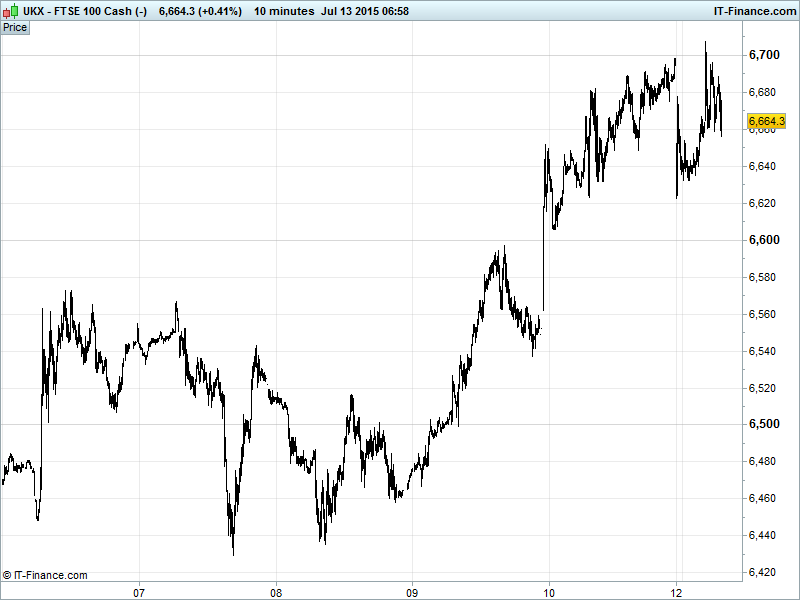

UK 100 Index called to open -35pts at 6635 with overnight resistance at round number 6700 preventing any test of falling highs from late May or any attempt to close the two week old gap at 6750. The bounce from October rising support at 6400 remains intact although we are seeing consolidation of the 250pts gains from last Tuesday. Watch levels: Bullish 6760, Bearish 6590.

The negative opening call comes from marathon overnight talks between Greece and Creditors failing to find compromise on a third bailout (€86bn). The €30bn increase on last week’s figure is due to frozen banks needing urgent recapitalisation if they are to reopen. China’s equity market bounce is offering some solace, buoying equities in Asia helped by better than expected China trade data as exports rebounded and imports contraction slowed.

Greek PM Tsipras, having conceded on pension and tax reforms, is fighting against IMF oversight and German-led demands for a Luxembourg-managed fund to sell €50bn in Greek state assets both considered crucial for a deal to avoid Grexit. It is unclear whether the German idea of a Greek 5yr ‘Timeout’/Temporary exit from the Euro to get its house in order is still on the table.

While ex-Greek Finance Minister Varoufakis compared Creditors to terrorists during his tenure, Syriza’s parliamentary spokesman has compared current talks to waterboarding. Others said Sunday discussions got very heated. No love lost between parties. Trust has become the biggest issue especially as Syriza party now so divided and parliamentary approval needed by Wednesday.

US stocks closed sharply higher on Friday (Nasdaq best gain since Jan), building on prior gains, as optimism rose that the weekend would see a Greek bailout deal and relief set in as that Chinese equities had begun to recover. The Fed’s Yellen maintained 2015 rate rise view but gradual, and labour market still not fully recovered. She also cautioned that external events could influence (delaying or bringing forward).

Asian stocks higher Monday in recovery mode from last week’s market turmoil and are outperforming despite lack of progress in Greek bailout talks, with China’s shanghai Composite re-inflating nicely towards another bursting point, buoyed by reports the government may unveil a CNY200bn loan to support infrastructure projects and increased margin-supported trading (up for the first time in 15 sessions).

Additional support in the form of aforementioned trade data while concerns about growth dipping below 7% in June largely failed to register concern with investors.

Japan’s Nikkei the top dog in the region with the safe-haven Yen weakening after earlier risk-off popularity waned, again despite still unresolved Eurozone issues, while Australia’s ASX retraced earlier losses helped by healthcare stocks yet remains 0.3% in the red this morning

Oil prices back on the back foot with 5 more US drilling rigs now pumping the black gold – still fewer working platforms than this time last year, but an increase of 17 in the last 2 weeks has big implications for production while Iran nuclear talks trudge on in the background, an imminent deal adding fuel to the fire of oversupply concerns. US Light currently $52; Brent $57.

Gold still failing in its duty as port-in-a-storm, sideways since Friday though we note rising lows since then, with resistance at falling highs dating back to 18 June converging – the stronger line of resistance and negative momentum indicating more potential on the downside than the upside for the yellow metal. Currently $1161.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Amplats says H1 earnings to rise by nearly 1,500%

- Genel Energy says H1 revenue estimated at $200m

- Genel Energy appoints Tony Hayward as chairman

- Chemicals maker Platform Specialty to buy Alent for $2.1bn

- Solar fund Bluefield eyes €200m London listing

- SThree's H1 gross profit up 10 pct

- Nostrum Oil & Gas approaches Tethys Petroleum for possible offer

- Arris continues to expect closing of Pace deal in Q4 of 2015