Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

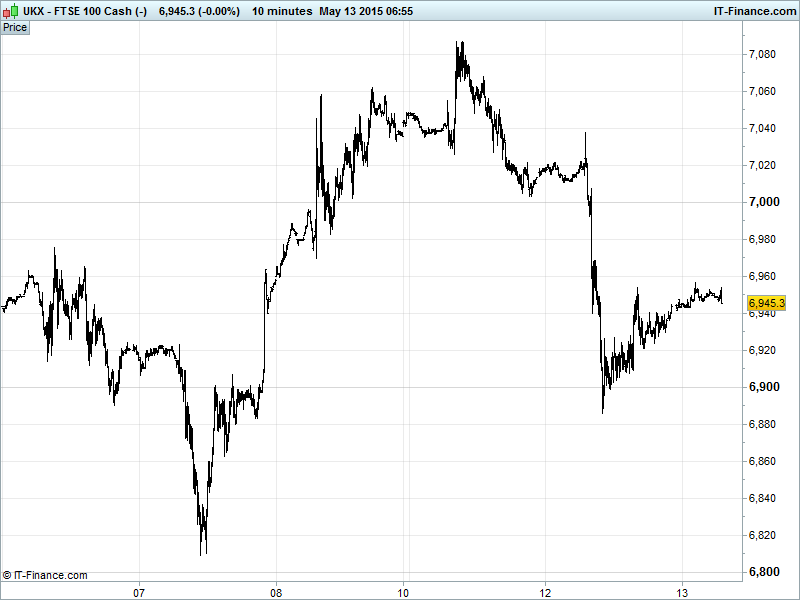

UK 100 Index called to open +30pts at 6965, having found support around the key 6900 and the 100-day moving average yesterday amid another sharp sell-off. The higher low could bode well as a platform for another attempt at recent highs 7088, however, we already note the struggle overnight around 6950 which could hinder progress. Watch levels: Bullish 6980, Bearish 6880.

The positive opening call comes as JP Morgan bigged up UK stock markets yesterday as a perceived trend change in the past few months – namely a UK 100 catching up with and surpassing its European index peers – is seeing UK equities with a dividend payout rate that is almost double the 10-yr Gilt yield as increasingly attractive to yield-hungry investors hit by negative bond yields elsewhere.

UK Oil & Gas stocks were in focus after the Obama administration gave the go-ahead for Royal Dutch Shell to start drilling in the Arctic. Shares nonetheless fell 3% while BHP Billiton shares picked up 3p each as plans emerged to streamline its operations next year.

US bourses stemmed their losses but nonetheless closed lower yesterday as bond prices corrected upwards, yields went down and investors turned their attention to the equity markets. Continuing concerns about Greece’s ability to repay debts – compounded yesterday by revelations it used its reserves at the IMF to repay the IMF - continue to weigh despite the ECB giving Greek banks some breathing space in the form of an increased ELA ceiling.

Asian stocks mixed overnight after another bond market wobble (Fed comments, rate rise concerns, post-QE world) and heightening of concerns about Greece’s perilous debt situation. While this lead to US equities delivering another weak session, sentiment given a boost by suggestions that the ECB increasing its ELA (emergency lending) and maintaining collateral levels to Greek banks, providing the beleaguered nation with some much needed breathing room.

Aussie stocks helped by retailers after the federal budget saw small business taxes cut igniting hopes of a spending spree down under. Japan’s Nikkei higher on hopes of the BoJ maintaining its stimulus course amidst improving economic fundamentals such as its current account surplus winding to the most in 7 years. Hong Kong in the red as Chinese stocks trade static.

Investors cautious after weak China data (Retail Sales, Industrial Production) vindicating the PBOC’s weekend rate cut stimulus but adding weight to existing worries about slowing growth in the world’s #2 economy. European data this morning also shows a divided core, with French Q1 GDP beating expectations and showing a welcome acceleration in growth. Neighbouring Germany however, failed to deliver the same message with Q1 growth slowing and inflation readings mixed.

Today’s macro data will be looking to improve upon some already disappointing Chinese and German prints, with UK employment numbers hoping to show an improved unemployment rate – down 0.1% to 5.5%, and average weekly earnings growing by 2.1% on the year which is above where inflation has been since last April. Later on we have Eurozone industrial production and GDP while the US will release its Retail Sales and Business Inventories.

Gold has made a step move higher to trade $1194, helped by Greek dire straits and a weaker USD Index, but still below that key $1200 level with panic very much absent. Note the rally from $1180 serves to bolster the level as support for any subsequent sell-off. Support $1180, Resistance $1200.

Brent Crude ($67) has broken out of a triangle pattern to the upside, hoping to recover recent 2015 highs hit on 6 May while US light ($61) is trying the same but sparring with resistance at its current level. The positive moves come after OPEC increased its global demand growth estimate and saw further growth as we move through 2015, and despite Goldman Sachs expressing concern about the rate of recovery when compared with the demand/supply outlook.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan Econ Sentiment Beat, improved

- China Retail Sales Miss, slower growth

- China Industrial Production Miss, slower growth

- China Fixed Asset Inv ex-Rural Miss, slower growth

- France GDP Beat

- Germany Consumer Price Inflation In-line

- Germany GDP Miss

- Germany Wholesale Price Index Mixed

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Hansteen Holdings sells UK industrial trust for £192mn

- Severn Trent agrees to sell water purification business

- Lloyds redeems all outstanding 6.09% 2015 preference shares at par

- Acromas prices placement of Saga shares at 195p each

- TUI Group profit growth on track, to sell LateRooms

- Admiral Group says Henry Engelhardt to step as CEO in one year

- Renishaw Q3 pretax profit £53.2mn

- Galliford try says expects FY results in line with expectations

- Private jet operator Air Partner buys broker Cabot Aviation

- Compass posts first half revenue growth of 5.7%

- Strong demand helps builder Barratt to lift completion rate

- Gold miner Centamin's core profit rises 55%

- Premier Oil cuts spending plan further over weak oil prices

- Partnership Assurance Q1 new sales drop 61% to £99mn

- Centamin says Q1 core profit up 55%

- John Wood Group sees FY EBITA broadly in line with estimates

- Mondi Q1 underlying oper profit up 29%

- Wood Group's JV with Massy Holdings gets $250mn BP contract

- SABMiller profit beats expectations, sees another tough year ahead

- Exillon Energy avg daily production was 17,037 bbl/day in April