Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

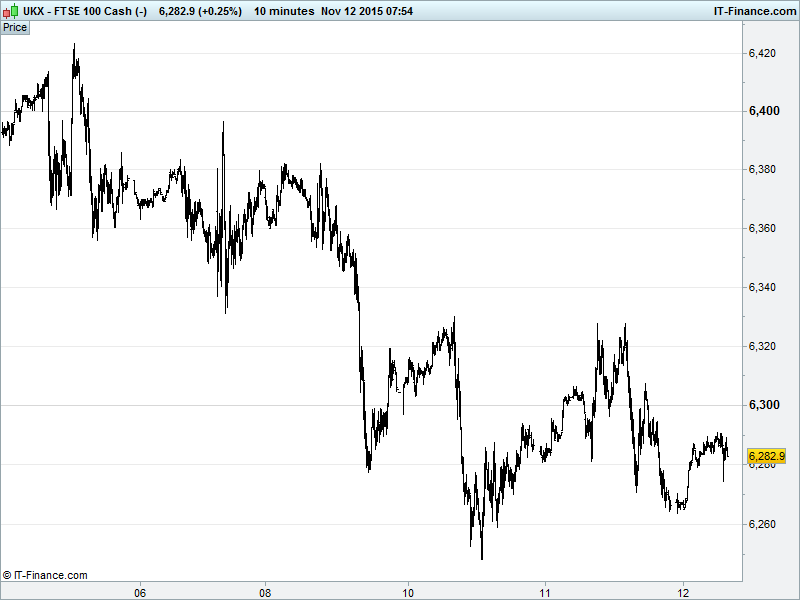

UK 100 Index called to open -15pts at 6280, still in a 7-day downtrend but with a higher low yesterday offering potential for a bottom to have been found around 6250-6260, and for a rebound from the lower bounds of its 1-month sideways shift. While a rebound towards 6400 is possible, falling highs around 6300 need to be overcome first. Watch levels: Bullish 6310, Bearish 6255.

The negative opening call comes after a muted session in Asia following a negative US close (all spookily -0.32%) as markets continue to fret about Chinese growth, the price of oil slipped further, and markets prep for a raft of US Fed speakers today, including Chair Yellen, who could shift the odds on a December rate hike and after much ECB chat yesterday, which President Draghi is set to continue today.

Australia’s ASX flat after a strong jobs report cut the chance of another RBA rate cut, while the index’s key commodities/energy space remains in the doldrums on China/global growth worries and a Fed strengthened USD. Japan’s Nikkei also flat, its rally stalling despite strong machine orders data , as a weak JPY comes off its lows to hurt exporters and investors await Fed clarification.

China weak and Hong Kong strength at odds with each other, with the former hindered by a technology stocks slump and concerns of an overdone rally of late, as well as mixed macro data all weak dampening sentiment.

US stocks posted another negative session on Wednesday with more disappointing China data and declines in the energy sector weighing on equities. Almost surprising to see the NASDAQ performing in line with peers given that the technology sector should be benefitting from rock bottom copper prices. More likely, however, is the prospect of higher interest rates potentially capping growth potential, or at least seen to be.

In focus today will be the improved German Inflation which is at odds with recent calls and expectations for more QE, although it depends whether France shows similar progress. Elsewhere, watch for better Eurozone Industrial Production. However, the highlight will be all the 6 Fed speakers destined to muddy the waters on the ‘stick or twist’ rate-hike decision next month. Oh, and after avoiding the subject of monetary policy yesterday, much to the annoyance of those wanting clarity on a Dec rate cut/more stimulus, President Draghi has tow more opportunities today. Super Mario?

Markets await further Fed updates this afternoon for added clarity on December, which is unlikely to be forthcoming. Nonetheless, Gold traders appear to be betting on an imminent rate hike with the yellow metal just off 3-month lows, helped a bit by bargain hunters in both physical and futures markets. Volume likely to remain light ahead of said Fed updates.

Oil prices off their overnight lows with the USD off its own corresponding highs. Potential for further dollar weakening on technicals to help oil (and commodities in general) today, but more likely to have an effect will be weekly EIA data forecast to show further increase in US crude stockpiles while lurking fears about Iranian supply are keeping the medium-term oil outlook bearish.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- BAE Systems Sees Good Sales Growth In 2015

- Beazley 9–month gross written premiums +6%

- Beazley reports 6% jump in gross written premiums

- BHP fights $205m royalty bill on Australian coal sales

- Burberry Raises Dividend to 10.2p

- Luxury brand Burberry says sales picked up in third quarter

- Card Factory Reports 7.9% Growth in Revenue, Retains FY Views

- FirstGroup Sees FY Trading Performance £15M Higher

- IMI sees FY adjusted EPS towards lower end of range of market estimates

- Kier Group Trading on Course to Meet Board's Views

- Norcros says H1 pretax profit +11% to £7m

- Premier Oil reduces investment costs, beats production target

- Restaurant Group Sees to Meet Full Year Market Expectations

- Rexam 3Q Global Beverage Can Volumes +3%

- Rolls-Royce 2015 Guidance Unchanged But Profit Expected To Be At Lower End Of Range

- Rolls-Royce CEO Says Activist Investor ValueAct Has Asked for Board Membership

- Rolls-Royce May Cut Dividend

- SABMiller reports Q2 acceleration as forex weighs

- Spire Healthcare cuts full-year revenue guidance

- TBC Bank says Q3 profit +11%

- Wincanton says H1 revenue +5.8%

- WS Atkins Posts 38% Jump in 1H Pretax Profit

- Young & Co's H1 profit before tax +3.7%