Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

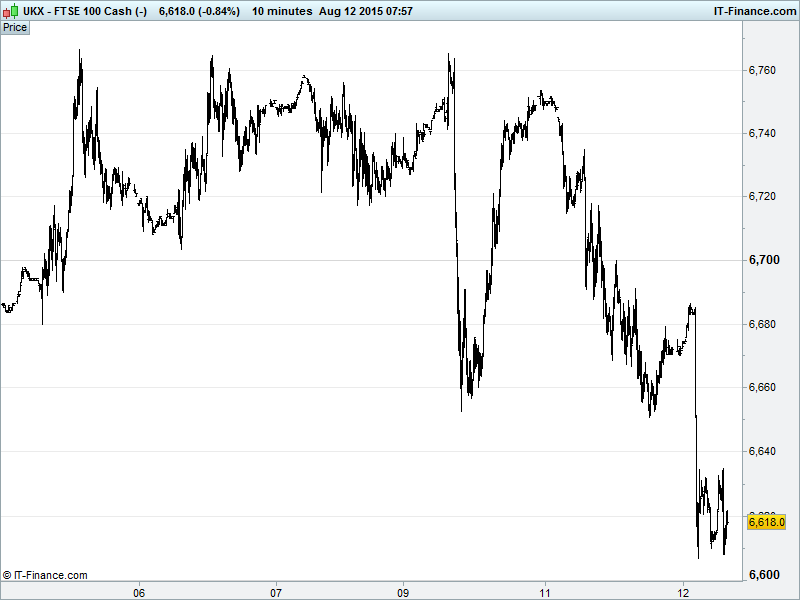

UK 100 Index called to open -45pts at 6620 having broken below this week’s 6650 support, which compounds the pull-back from 2-month falling highs resistance at 6750 and, as mentioned yesterday, increases the likelihood the correction goes as far as July rising lows at 6550, or maybe even 10-month rising support at 6500. Watch levels: Bullish 6660, Bearish 6595.

The negative opening call comes after China allowed market forces to push the Yuan lower for a second day (so much for yesterday being a one-off; says no basis for further devaluation but can we believe that?) fuelling concern that market volatility from a new round of ‘currency wars’ could curb global growth outlook. Speculation also rising that the Fed may avoid a September rate hike with the Chinese intervention keeping the USD strong in relative terms.

With yesterday’s move giving rise to worries that growth in the world’s #2 economy is even slower that thought/published, today’s move just before another round of weak China data just adds fuel to the fire with Retail Sales, Industrial Production and Fixed Asset Investment all missing consensus and slowing in July.

All this is easily taking the shine off apparent progress towards a Greek deal being reached ahead of schedule with concerns about political hurdles, with Germany wanting more negotiating time and a bridge loan rather than a hasty agreement, the IMF less involved, the problem of debt sustainability still a major issue and chance of snap elections still high given coalition rifts from imposition of another three years of harsh austerity.

Asian stocks lower overnight, having taken negative cues from Europe and Wall Street, as regional FX suffers (6yr lows vs USD) from China’s second devaluation move, commodities continue to get crushed on a questionable Chinese and thus global growth outlook and Oil is hindered (March ‘09 lows) further by a negative OPEC statement on global supply/demand.

Japan’s Nikkei lower on prospect of less demand for its exporters’ wares to China and poor Producer Price Inflation even if Industrial Production improved and BoJ minutes offered no surprises. Note China and Hong Kong weakness from domestic and international growth fears, along with declines in commodity prices, Miners and Banks all weighing heavily on Australia’s ASX despite weaker AUD.

US stocks closed lower Tuesday with futures selling off this morning after the PBoC surprised markets and again allowed the Yuan to devalue, having said that yesterday’s intervention to move the daily fix would be a one off. This raising further growth concerns regarding the world’s #2 economy and a potentially forthcoming ‘currency war.’

Stateside macro data came in mixed: Unit Labor Costs beat while Non-Farm Productivity fell short. US wholesale data was also mixed with inventories beating and trade sales missing. We now await the next round of Fed commentary amid tremendous rumblings in the currency markets, reinforced growth worries pertaining to both China and the rest of the world and a Greek deal that is this morning described as ‘utterly unachievable.’

Companies wise, Hertz reported a $58m decline in profits yesterday. The car rental firm (profits down by $58m, share price -37% YoY), not to mention the sector at large, continues to battle disruptive newcomer Uber and fellow ride sharing competition.

In focus today will be UK Employment and Earnings data likely for the wages growth more than the unemployment read and potential read-across for now delayed UK rate rise. The update for Eurozone Industrial Production is seen showing another month of contraction in June while comments from the Fed’s Dudley will be sure to keep things spicy given his currently neutral stance.

Gold ($1114) benefitting from China’s Yuan being allowed to devalue again, with the prospect of a currency war drawing risk averse investors into the safer haven of an alternative currency that sets its own price (no central bank for gold; no government). Yesterday morning’s resistance now support. Potential for the yellow metal to have at last found some buoyancy amid foreign exchange volatility?

Crude prices fell to multi-month lows in early trading with USD strength vs. Asian currencies stifling demand, notably of course from China where doubts are mounting as to the validity of its growth data, raising concerns about demand. OPEC adding downward pressure with a 0.3% MoM rise in output while raising its forecasts for US offshore production in 2015. Brent $49; US Light Crude $43.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- APR Energy takes Q2 write – off of about $24m on Yemen woes

- Tullow says Jubilee output returns to previous rate after issues resolved

- Lookers says H1 pretax profit +6% to £39.9m

- Interserve confident of growth after H1 profit rises 12%

- Balfour Beatty sees contract issues stretching into 2016

- Zoopla says has started winning back lost agents

- Aquarius Platinum's FY headline loss $51m vs $11m

- Petroneft says current gross production at licence 61 about 2,600 bopd

- Galliford Try JV named on public buildings contract worth up to £3bn

- Centamin Net Profit Rises; Declares Higher Dividend

- Colt Group Update on Fidelity's all cash final offer

- Pearson Sells 50% Stake in the Economist Group

- G4S 1H Pretax Profit Dips on Restructure Costs; Ups Dividend

- Capital & Regional NAV +12% in First Half; to Step Up Capex Plan