Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

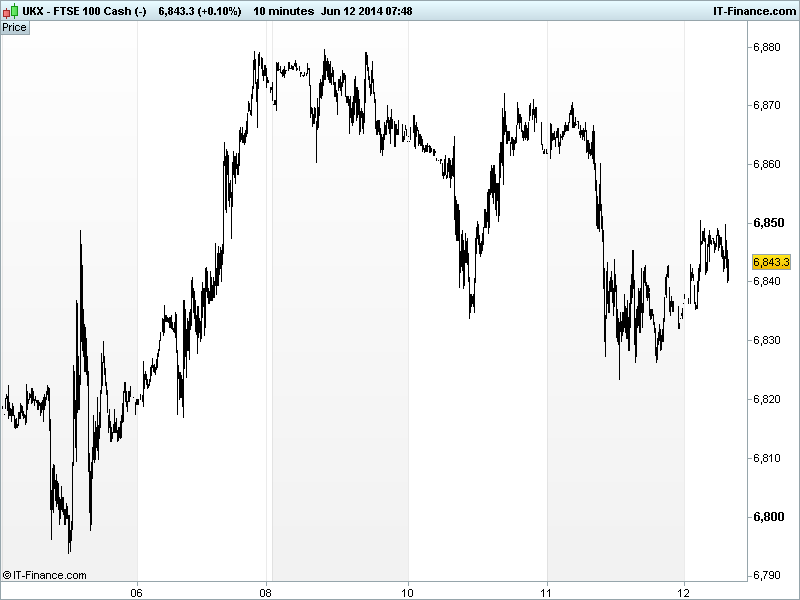

UK 100 called to open +10pts at 6845 with another recovery from the sell-off, but this time with only limited gains, and anther failure to regain the prior highs which adds to the trend of recent falling highs. Major bourses have also come back from their record highs, suggesting the momentum that was inching them higher has fallen. A pause for breath all round. The UK Index ’s 1-month trading range 6770/6887 is unchanged. Note Euronext delaying the open of equity markets (FR, NL, BE, PL) due to a ‘critical issue’.

US markets closed the most bloodied in 3 weeks with DJIA the underperformer and Nasdaq the outperformer, retreating from their recent record-setting run as traders book profits on flagging momentum, exacerbated by the World Bank’s cuts to global growth forecasts and US political risk being revived after House majority leader Cantor (Republican) lost his seat to a Tea Party Challenger Brat.

With the situation in the Ukraine slightly less tenuous (still negotiating on gas supply), geopolitical risk has also resurfaced with militant Al-Qaeda splinter groups overrunning two major cities and an oil refinery town in Iraq which has seen the price of a barrel of WTI and Brent regain their recent 1-month highs. Additional support came from OPEC leaving its production ceiling unchanged, leaving output below forecast demand for the rest of the year.

Overnight, stocks in Asia have taken the negative lead from the US and retreated from 6yr highs as concerns mount about market complacency (inching higher on less and less) and the emergence of risks (hazier growth outlook, geopolitical risk, US politics). Note New Zealand hiking interest rates as expected but offering a surprisingly less dovish statement suggesting potential for more hikes later in the year.

Macro data provided no additional support for the Australian ASX with its jobs report showing a stable unemployment rate but a surprise drop in jobs added and a lower participation rate. Japan’s Nikkei offered no help from a less weak reading for machine orders. After the ECB bazooka of last week, note German Wholesale Price inflation going negative in May.

In focus today, following the ECB’s move to fight the threat of deflation, will be French Consumer Price Inflation which is seen flat to just positive in May after a flat reading in April. Eurozone Industrial Production is seen improving from a negative read in March.

In the afternoon US Jobless Claims are seen unchanged but it’ll be US Retail Sales growth, expected to show improvements across the board in May, which will get more attention given its indication of consumer confidence. To close the day, US Business inventories are seen posting the same growth rate as in March.

In commodities, Gold is hovering around the $1260 level supported by a trend of rising lows from 5 May as well as the emergence of some risk factors which have increased interest in the yellow metal as a safehaven. Note the test of $1265 yesterday. Many asking if it can get back to the $1290 from whence it fell.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK RICS House Price Balance Beat, improved

- JP Machine Orders Beat, not as weak

- AU Jobs report Mixed

- DE Wholesale Price Index Deteriorated

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Halma profit up 15 percent

- B&M sees market cap at 2.7 bln stg after IPO pricing

- AstraZeneca licenses rights to Synairgen asthma drug

- UK's Pets at Home posts 12.4 pct rise in earnings

- Carillion consortium secures Scottish road contract

- UK approves Premier Oil's North Sea Catcher development

- Home Retail on track to meet year profit forecasts

- Boohoo.com reports 63 pct jump in FY revenue

- Kingfisher says CEO of Castorama & Brico brands to step down

- Avocet mining says financing talks ongoing

- WS Atkins confident for the year ahead after 2014 profit jump

- PZ Cussons says full-year results in line with expectations