Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

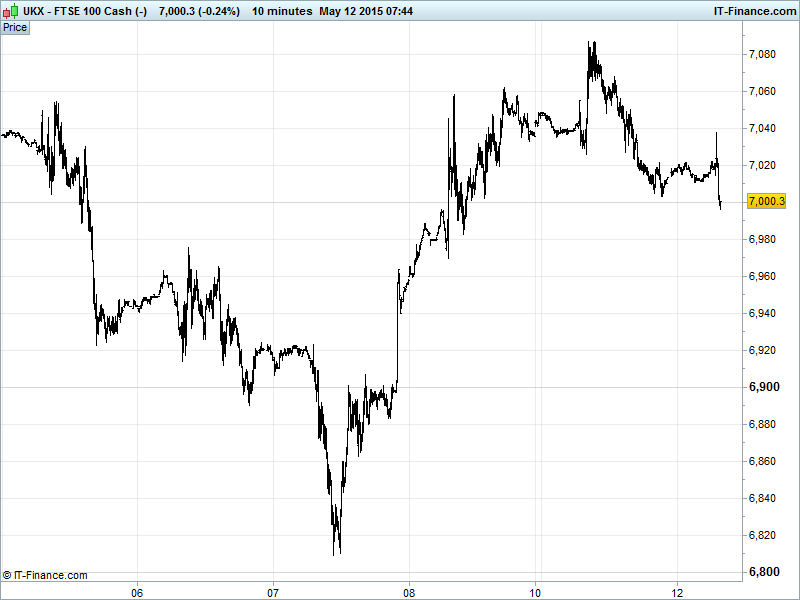

UK 100 Index called to open -35pts at 6995, testing the round number 7000 which also corresponds with support from a recently bettered intersecting trendline dating back to 27 April highs. Bulls eyeing yesterday’s attempt higher (7088), while Bears hope for a drop back into the recent falling channel 6850-7000. Watch levels: Bullish 7050, Bearish 6980.

The negative open comes as the UK settles back into reality this week after Friday’s general election. Strong business confidence following a Conservative win is tempered by a budget deficit of around 5% of GDP, which is over the EU’s limit of 3%, and the prospect of a referendum on the UK’s future in Europe. Retail sales also disappointed in May with the early Easter holidays largely blamed for the print missing consensus and deteriorating on last year.

US bourses obediently gave up Friday’s gains on Monday as the dollar strengthened against the Euro over the usual issues. Those being Greece related, of course. A friendly statement from the Eurogroup praised the progress that has been made so far in Greek bailout talks while conceding that much more needs to be made to get those final gaps on remaining issues bridged. Total reform implementation demands have morphed into partial reform requests in return for partial debt relief in what has been hailed as ‘considerable convergence’ by Yanis Varoufakis. An agreement will be reached in the next few weeks, he says. So what’s to worry about?!

Asian stocksmixed overnight with Japan’s Nikkei echoing profit taking on Wall Street and a revived bond rout as investors watch Greek bailout talks closely (enough cash for a fortnight?) and despite a normally beneficial weaker JPY. Equities in Hong Kong also lower despite Chinese stocks continuing to benefit from the PBOC’s weekend decision to cut rates to bolster the flagging economy.

In focus today we have the UK’s Industrial Production looking for no change on the month (but a slowdown on the same period last year) with a steady 0.1% increase on the year. Manufacturing Production is seen generally slowing. This afternoon in the US will be Small Business Optimism and Jolts Job Openings both looking for an improvement on the last prints. The UK’s GDP estimate comes in at 3pm.

Note Aussie equities higher ahead of its federal budget thanks to strong Home Loans data and a rise in Consumer Confidence, as well benefiting from #1 trading partner China’s post-rate cut rally. Note ratings agency Fitch saying falling commodity prices will hurt the Aussie budget bottom line but AAA rating not at risk.

Banks have been in the spotlight again, mostly for the wrong reasons as Nomura and RBS face $500mn in fines for what US Judges have coined ‘an enormous deception’ in the sale of mortgage backed securities in the run-up to the 2008 crash. HSBC, meanwhile, has been called a ‘value trap that is sleepwalking towards a break-up’ by Macquarie and is co-weighing, with RBS, on the UK 100 this morning. Damage limitation comes in the form of mining stocks which have found support in additional Chinese stimulus.

Following the Sunday Times article on a fast-track £35bn sale of the government’s LLOY & RBS bailout stakes, note today’s announcement that the UK’s stake in LLOY has dropped below 20% to 19.93%. For retail sector followers, note April UK BRC Like-for-Like Sales deteriorating markedly, although likely hurt by early Easter.

Brent Crude ($64.7) and US Light ($59) just about maintaining their uptrends with an oil sell-off from 6 May peaks having found support around $64.20 (Brent) and $58.9 (WTI). Barclays has warned that the recovery may not last, citing a large discrepancy between supply and futures market sentiment.

Gold is holding above $1180 (just) with a weaker EUR and thus stronger USD (1-week high) hindering progress, safe-haven demand lacking in the face of Greek debt crisis talks (progress very slow) and despite equities selling off on Wall Street and delivering a mixed Asian session. Cautious demand for the asset class of the wary? Support $1180, Resistance $1193.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK BRC Sales Like for Like Miss, deteriorated

- Aussie Home Loans Beat, accelerated

- Japan Sentiment Indicators In-line

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Rockhopper resumes Falkland Islands drilling work

- Britain cuts Lloyds Banking Group stake to below 20 percent

- UK says total raised by Lloyds sales now above 10 bln stg

- Grafton reports growing revenues in four months to April

- Enterprise Inns to accelerate managed pubs expansion

- Hiscox says Q1 gross written premiums increased by 12 pct

- easyJet swings to a profit in weaker season

- Speedy Hire says FY profit rises to 21.9 mln stg

- Barclays says Barclaycard CEO Val Sorranno Keating to leave

- Barclaycard CEO to leave bank to pursue "new professional challenge"

- Experian expects margins for year to be stable

- Falkland Islands oil explorers resume drilling work after repair

- IP Group says portfolio now consists of holdings in 93 intellectual property – based cos

- Hilton Food says performance has been in line with its expectations

- Genus says trading in line with expectations for financial year 2015

- SkyePharma says remain confident of FY outlook

- James Fisher buys assets, IP rights of X-Subsea for 14.8 mln stg