Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

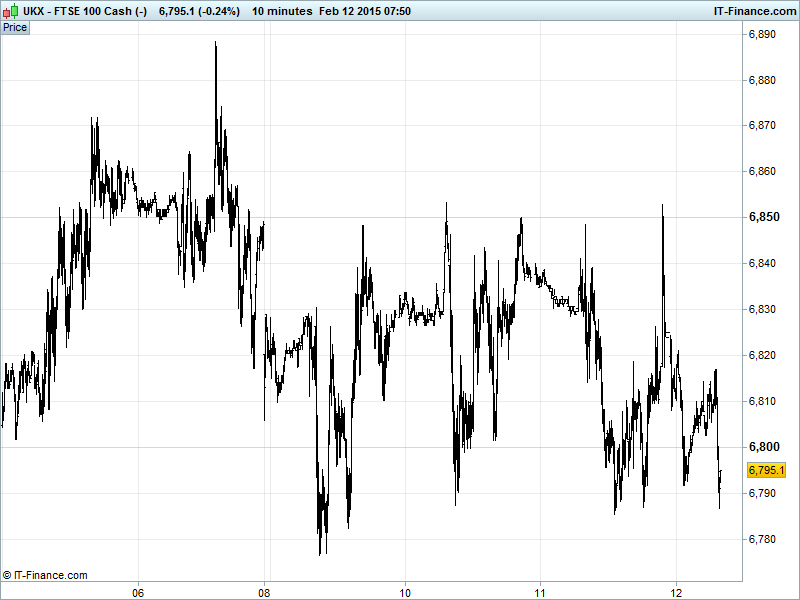

UK 100 Index called to open -30pts at 6790, managing to hold its position within a 4-day sideways shift, continuing to test the 6800 level and rising lows from 2 Feb, but again failing to break above recent resistance around 6850. Still in the upper half (just) of the 6720-6905 sideways channel from mid-Jan (pause?) amid an uptrend from December lows. Unchanged watch levels Bullish 6860, Bearish 6770.

The negative opening call stems from a lack of progress in both Brussels and Minsk with overnight debt talks between Greek and Eurozone finance ministers breaking down while investors keep an eye on the geopolitical situation in Ukraine (fighting + ceasefire talks), more hawkish Fed chatter and oil coming under more pressure after another US crude inventory build.

Even though we’d be warned not to expect a Eurogroup/Greece outcome (that’s it guys, set the bar nice and low) it takes us a step closer to a self-imposed Monday deadline for a bailout extension (unwanted by Greece) and the country’s bailout programme expiration at the end of the month which could see it sail into March without financial assistance for the first time in 5 years. However, as always, participants still hopeful of a positive outcome

US stocks closed mixed around breakeven after a choppy session, recovering from weakness following the EIA US Crude oil inventory report (another build, another record high), helped by reports of a positive outcome in Minsk (still unproven) with FR, DE, RU and UKR leaders set to sign a joint declaration supporting Ukraine’s territorial integrity and sovereignty and a ceasefire until September.

Asian stocks are drifting as investors digest a disappointing Australian employment report, more deflationary PPI in Japan, the absence of European/Ukraine progress and hawkish Fed chatter (Fisher; early and gentle hikes. Bullard; earlier rather than later).

Note Japan’s Nikkei helped back from holiday by a weaker JPY and rebound in machine orders, while Australia’s ASX hindered by bad jobs data which highlight struggles and add to expectations of another rate cut by the RBA. China stocks in the red.

In focus today we have Eurozone Industrial Production seen stable in December, much like US Jobless Claims and US Business Inventories in January, while headline US Retail Sales remain stifled although the core could rebound. The UK BOE inflation report and speech by Governor Carney will be analysed for clues as to rate hike trajectory while the Eurogroup meeting of finance ministers will be closely watched for progress regarding Greece.

Gold ($1222) polished up its act this morning after Greece failed to strike a bailout deal in Brussels yesterday, somewhat tipping the safe-haven-demand balance away from the strong USD. Hopes that a deal has been struck in Ukraine abound this morning (details unknown at this moment) are keeping desires for the yellow metal largely muted and it remains in its downward channel from 22-Jan highs

Oil recovered slightly this morning having fallen again yesterday following the EIA stockpile report which put US commercial inventories up again for the week ending 6-Feb. Falling rig counts, oil major capex cuts and refinery runs in Europe have all helped support the commodity in recent weeks and continue to do so. Brent and US light crude were at $55.05 and $49.71 respectively this morning, just about maintaining their trend of February rising lows.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan Producer Prices Miss, deteriorated

- Japan Machine orders Beat, bigger rebound

- UK RICS House Price Balance Miss, deteriorated

- Australia Consumer Inflation Expectations Accelerated

- Australia Employment Miss, deteriorated

- Germany Consumer Price Inflation Miss, deteriorated

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Rio Tinto plans $2 bln buyback as H2 profit dives

- Rio Tinto says FY underlying earnings $9.3 bln vs $10.22 bln last year

- Informa FY revenue rises marginally

- Darty Q3 group revenue rises 2.4 pct

- DCC reaffirms full year guidance, flags milder weather impact

- SuperGroup COO to leave firm

- APR Energy says commissioned power plant in western Australia

- BT launches 1 billion pound placing to fund EE deal

- Insurer Lancashire posts 4 pct rise in FY pretax profit

- Morgan Advanced Materials says FY revenue drops 3.8 pct

- Zoopla says trading robust after rival platform launch

- Circle Oil says oil price impact moderated by Morocco gas production

- Imperial Tobacco stands by full-year dividend goal

- Royal London sees strong new business in 2014, assets up 12 pct

- John Laing offer price set at 195 pence per share