Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

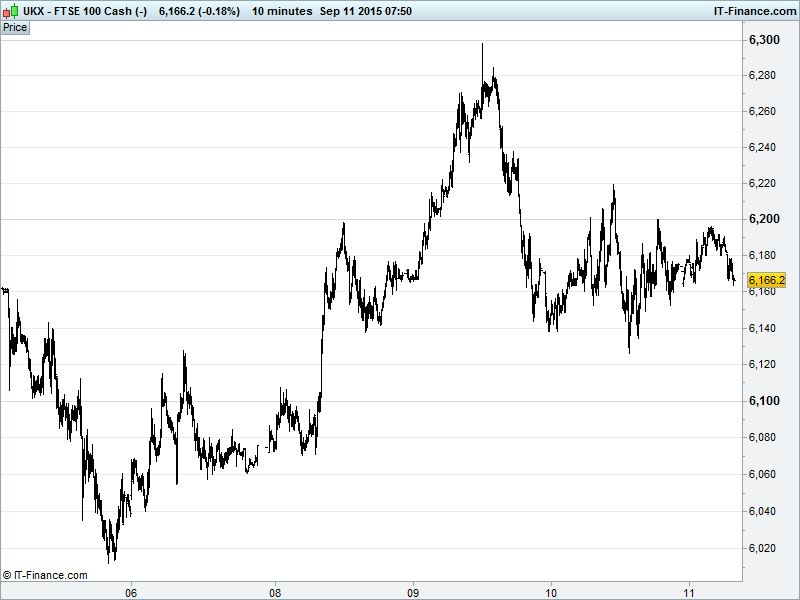

UK 100 Index called to open +15pts at 6170 in a narrow 6130-6200 range as we move into the weekend. We are still holding above rising lows from 25 Aug which keeps bullish potential alive, helped further by the intersecting trend-line from Aug 28 highs becoming supportive around 6140 following Tuesday’s breakout. Note, however, 6200 proving an upside struggle since early yesterday. Watch levels: Bullish 6230, Bearish 6110.

The positive opening call comes despite a mixed yet calmer Asian session overnight following moderate gains by US bourses in the wake of more deflationary data (import prices; blame commodities rout), flat jobless claims and a recovery by Oil.

Uncertainty still rife about what the Fed will do next week although we remain convinced it will do nothing, there being little margin for error and too much going on outside the US (economic concerns, market volatility). Calls to hold off are multiplying. Note potential for risk appetite to wane into the weekend as a result of the raging debate on the potential fallout from a rate hike.

Stocks in China in the red despite signs that authorities remain committed to stabilizing now volatile financial markets. Japan’s Nikkei close to breakeven despite data showing improved business confidence in Q3, with US demand offsetting Chinese concerns, the latter being something economy minister Amari alluded to. Australia’s ASX underperforming major regional peers.

Both US equities and treasuries finished up on Thursday (treasuries outperforming slightly), reflecting the current looseness of monetary policy and a fairly even divide between the risk-hungry and risk-averse investor ahead of next week’s much anticipated FOMC meeting where a US rate rise may just materialise, however unlikely that might be.

Further gains into the weekend possible after Yellen’s former aide Andrew Levin commented “We’re not home yet - we’re not back to full employment” in an interview with MarketWatch, citing research he’s conducted with former BoE economist Danny Blanchflower. If it’s employment he’s worried about then what about inflation, which is way further from the mark?

In focus today will be BoE/GFK UK inflation expectations at 9.30am followed, in the afternoon, by surely more deflationary data from the US in the form of US PPI worsening in August and Uni of Michigan US Consumer Confidence pulling back slightly, ever closer to 2015’s May lows. The evening’s US Baker Hughes Rig Count is likely to remain of interest to Oil traders.

Oil back on the agenda with Barack Obama all but able to sign off on the Iranian nuclear deal having seen off Republican and Democrat opposition. Crude prices obediently off their overnight highs this morning (WTI $45, Brent $49) after rallying yesterday on strong demand with EIA inventory reports (overall US stockpiles up; refinery activity down) pointing towards a continued supply glut and adding to indications that Iran is set to join the party, not to mention a stubborn as ever Saudi Arabia seeing no reason to talk to its mates about prices.

Gold ($1110) flat since yesterday’s close having retraced gains to trade back into a potential bearish pennant. Buoyancy may be found, however, in the form of risk-off moves into the weekend, especially with the FOMC meeting next week.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- G4S wins security contracts in Iraq and Afghanistan

- AstraZeneca buys manufacturing facility in U.S. from Amgen

- Labour's Corbyn pledges UK windfall tax in 2020, targets RBS

- Rovi Video Continues to Be a Metadata Market Leader across the Globe

- Faroe Petroleum Says Norway's Portrush Well To be Abandoned

- Pub Operator Wetherspoon Posts Record Fiscal 2015 Revenue

- Galliford Try Wins Leeds University Contracts Worth £37.8m