Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

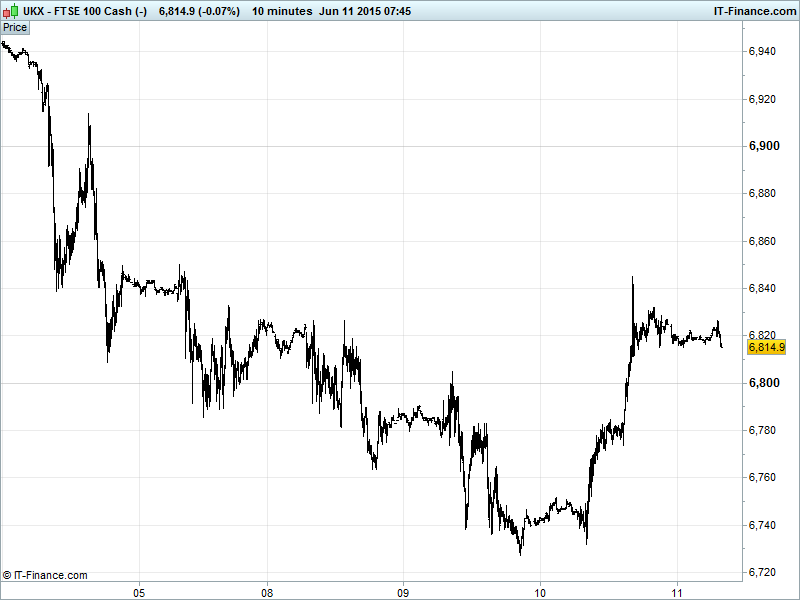

UK 100 Index called to open -15pts at 6815. While the bounce from the 200-day MA 6747 yesterday will have got the bulls excited, note the bears highlighting the trend-line of falling highs from 29 May at 6830 which has already served as resistance overnight and represents a near-term hurdle to overcome before a rebound can assumed. Watch levels: Bullish 6855, Bearish 6795.

The negative opening call comes after yesterday’s late optimism of a Greek deal and German concessions (one large reform will do, for now) was capped by overnight news that, once again, no deal had been reached and talks would - again – intensify. Ratings agency S&P also did its bit by downgrading Greece further into junk territory saying default likely within a year if no debt deal reached.

US markets closed higher with banks and tech surging thanks to the Greek deal optimism which saw European stocks rally into the close, with hopes that the current Greek-Creditor standoff would see a favourable resolution reached although the ECB move to help banks with additional emergency liquidity just suggests more time needed. We remain sceptical of anything happening before month end.

Asian equities positive for a second day, following their European and US counterparts higher (the Dow saw its biggest one day gain in a month), on the same hopes of a Greek deal being on the horizon (it always is) and renewed USD strengthening serving to provide a beneficial weakening to Asian FX.

Japan’s Nikkei in the green higher for the first time in five days, tracking global sentiment on Greece and thanks to renewed JPY weakening (USD found support) which has helped exporters. Note Australia’s ASX benefiting from better than expected jobs data with a drop in unemployment and surge in job additions.

China in the red after better than expected Retail Sales and Industrial Production data, although Investment was weaker. Let’s see if good data taken as good (for economy) or bad (stimulus negative) today. Data suggests government action helping stabilise things. Can a pick-up help global growth outlook?

In focus today we have US Retail Sales which will be looked to for signs that consumers are delivering a spending rebound via increased confidence in the economic recovery despite wages growth being lousy and one of the reasons the Fed is holding off from a rate rise. US Jobless Claims seen unchanged, US Import prices forecast to show an inflationary improvement while US Business inventories tick up again.

Overnight, the UK Mansion house speech saw Chancellor Osborne confirm that the UK government’s stake in bailed-out RBS would be sold back to the markets within months following successful reduction of holdings in bailout peer Lloyds. While the RBS stake would be sold at a £7bn loss, the government will still book a £14bn profit on all the bailouts (RBS, Lloyds, Bradford & Bingley and Northern Rock).

The Gold rebound got as far as $1192 yesterday before reversing to revisit $1185 as the USD found support. Still work to be done before downtrend from mid-May is a thing of the past, with global concerns aplenty in terms of driving safehaven demand, but overnight weakness could prove just a pause (bullish flag?) within the recovery from 3-month lows.

Oil remains big thanks to the recent USD pull-back making the fuel cheaper form relative standpoint. US Light holding around $61.5 while Brent rallied back to $66.2 early June highs.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Mulberry sees trading improve after big profits fall

- PZ Cussons says FY trading in line with expectations

- Engineering consultancy WS Atkins positive after profit rise

- DKSH and AstraZeneca expand relationship in South East Asia

- Shire appoints Olivier Bohuon to its board of directors

- Home Retail says Argos sales dented by poor electricals market

- Ophir Energy says production reliable during Salamander integration

- Spirit Pub says Greene King offer no longer conditional on CMA approval

- Petrofac Awarded Pact In Oman

- Salamander Energy published Independent Reserves Report

- Halma FY Pretax Profit Falls, Dividend Rises