Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

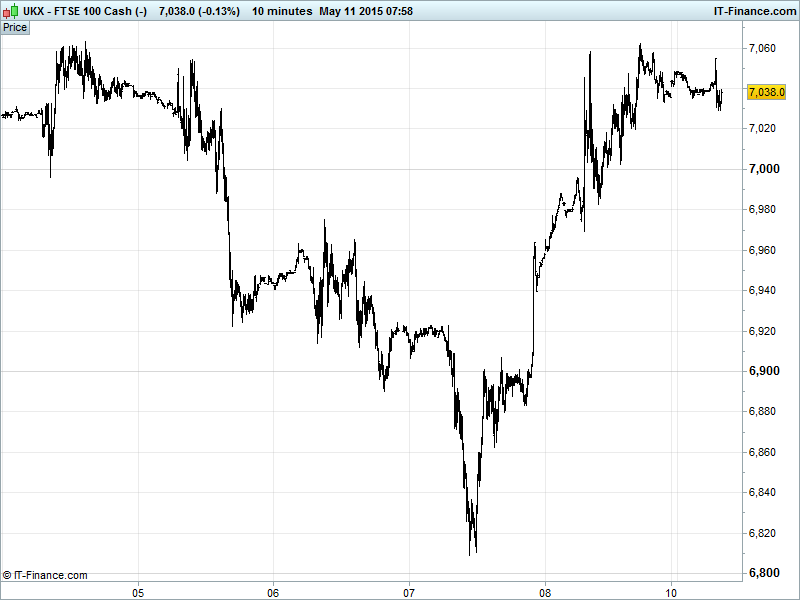

UK 100 Index called to open flat at 7040, still buoyant following the surprise UK Election result and helped by weekend China stimulus, back above the 7020 ceiling of its recent falling channel and showing appetite to make another test of recent 7063 highs even if this level proved resistant again late Friday. Could Greek news on debt negotiations be today’s driver? Watch levels: Bullish 7070, Bearish 6995.

The flat opening call comes after a strong rally on Friday following the surprise all-out Conservative win in the UK’s general election. Markets also reacted to a ‘solid’ US Non-Farm Payrolls report that was nonetheless not seen as good enough to warrant a June interest rate rise.

In Europe, Greek officials have been preparing for today’s Eurogroup summit in Brussels following a weekend of ‘feverish’ negotiations as the pressure mounts on Athens to take action to avoid defaulting on its debt. PM Tsipras’s government is due to repay €750mn to the IMF on Tuesday this week. Eurogroup officials are concerned that a very real chance of Greece going bankrupt exists at the current time. Note the third interest rate cut in 6-months by the People's Bank of China will likely benefit mining stocks in the UK Index this morning and into the week ahead.

US bourses closed noticeably higher on Friday after the good but not that good Non-Farm Payrolls print which, while an improvement on March’s report, lacked the accompaniment of the desired wage growth to warrant a tightening of monetary policy any time soon. The result buoyed equity markets as the possibility of a June rate hike retreated with September presenting the next opportunity.

Following Friday’s UK election result, watch out for further moves in beneficiary sectors such as Utilities, Real Estate/Property, Banks, Outsourcing, which are seen doing better from a Conservative majority government. Note a Sunday Times article talking of plans for a fast-track £35bn sale of the government’s RBS and Lloyds bailout stakes back to the private sector following last week’s Conservative victory.

Asian stocks positive overnight thanks to China’s central bank (PBOC) cutting interest rates for the third time in six months as it bolsters support for the struggling economy (slowing growth, below target inflation, property slump, worrying debt, poor recent trade data) and after US equities closed higher following the latest US jobs report which below neither hot nor cold in terms of changing expectations for a September rate rise.

Weekend data showed Chinese Consumer Price Inflation (CPI) rising slightly in April, but still below target, and Producer Price Inflation (PPI) falling for the 38th straight month, vindicating stimulus and the aforementioned rate cuts. Aussie Business surveys showed confidence holding strong, but conditions giving up ground.

Gold continues to tread water around $1188, failing to make headway due to equity gains and the USD Index rebounding from 94 support (largely positive US jobs report, EUR weakens on lack of optimism of quick Greek debt agreement) dampening demand for safehaven yellow metal in spite of uncertainty linked to Greece and the state of the global economy. Support $1180, Resistance $1200.

Brent Crude ($65) still trading around that $65 support while US Light ($59) has recovered its uptrend and begun following the trend line that was acting as support in a rising channel last week. Drivers affecting prices at the start of the week came in the form of Friday’s Baker Hughes rig count which posted shrinking declines in US operational drilling rigs, allaying somewhat fears of a supply glut while a Saudi-brokered ceasefire in Yemen dealt with supply-shortage worries in that part of the world. Prices for both benchmarks little changed from the end of last week.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Consumer Price Inflation Miss

- China Producer Price Inflation Miss

- Aussie NAB Business conditions Deteriorated

- Aussie NAB Business Confidence Unchanged

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Afren fails to make 2019 bond interest payment

- Lonmin posts smaller first half loss, keeps sales guidance

- Spain's Sabadell sees acceptance for TSB offer of over 71 pct

- Cairn Energy expects one billion barrels of oil offshore Senegal

- Spirax – Sarco organic sales rise 4 pct in first four months

- UBM names Marina Wyatt as CFO