Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

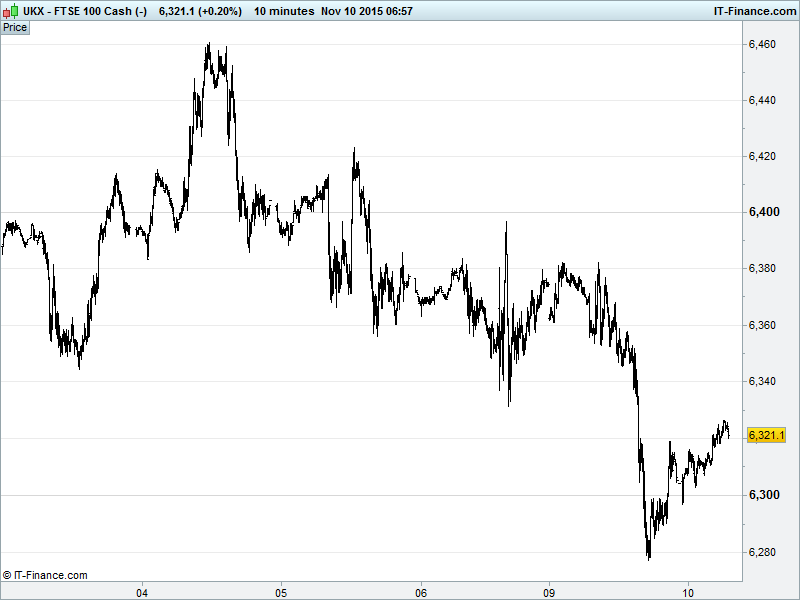

UK 100 Index called to open +25pts at 6320, having found support at 6270 overnight, still in a November downtrend and hindered by the 100-day MA since end-October. While we remain in a sideways shift from early October, there is still potential to fall back to the early October breakout at 6250 where we find intersecting support dating back to early Jan. Watch levels: Bullish 6340, Bearish 6240.

The positive opening call comes after more disappointing data from China, this time reiterating deflationary pressures, boosted speculation of more monetary easing to stem the declines. It also comes in spite of a largely mixed session for stocks in Asia, with Japan continuing to outperform on the back of a weaker JPY (2.5 month highs) thanks to USD strength from raised odds of a US rate rise by year-end.

The mixed session comes as European and US markets gave up ground on concerns about global growth (blame China data and OECD cuts to estimates), the prospect of a US rate rise confirming divergent central bank policy coupled with scepticism about equity valuations and the sustainability of the recent rally. Chinese stocks fell the most in 3 weeks after the nation’s inflation data exacerbated worries about weakening demand while Aussie shares remain hindered by depressed commodity prices, data suggesting China weakness as well as a drop in business confidence down under.

US bourses posted an average 1% loss on Monday in a bearish start to the week with investors crystallising both profits and losses – anything to get out of equities ahead of a possible December US interest rate rise and amid concerns of overvaluation. Note stateside bond markets failing to shine with US treasuries finishing just off Monday’s worst levels, though U.S. two-year yields are remain near their highest since 2010.

Markets are clearly moving to reflect the near certainty that the U.S. raises rates in December while the ECB talks up further easing of its own policy – the result is a Eurodollar rate at its lowest level since April. Elsewhere, Boston Fed President Eric Rosengren warned us not to concentrate too much on December since all future Fed meetings could be appropriate times to tighten policy, adding that possible risks from emerging and global financial markets have still not materialised (here we go! Could they be warming us up for yet another delay?)

Eurozone worries also returned after a period of calm, with Greece seeing its latest bailout tranche delayed due to disagreement on homeowner repossession protection which could delay urgently needed recapitalisation of its battered banks. On the other side of region Portugal faces political risk with two leftist parties agreeing to work together to create an alternative government although QE and the ECB backstop should contain any resultant volatility.

In focus today we have US Import Price data seen showing he nation’s own deflation pressures while growth remains absent for Wholesale Inventories and Sales. Elsewhere listen out for what the ECB’s Nouy, Coeure and Liikanen have to say in case it relates to more stimulus while the BoE’s Cunliffe speaks after the European close.

Oil prices are due to remain around the $60 mark for the next 3 years, according to BP’s Middle East regional president Michael Townshend, although where he got that figure from remains elusive to us – Brent Crude is struggling to consolidate above $50 in any meaningful way amid continued global supply overkill, with Saudi Arabia’s strategy looking like it’s ushering in a sustained period of low prices. Not the outcome Saudi Arabia wants (or any oil producers for that matter), but it doesn’t take a rocket scientist to calculate the consequence of market oversupply.

Gold still holding above 3-month lows around $1090. It’s all about the US jobs report, much reported on already. Bears will no doubt look for Goldman Sachs’ Eurodollar parity (and beyond) prediction to bear fruit towards the end of the year, though a surprise pop should the Fed not push the button in December could change all that.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Land Securities H1 adjusted NAV rises 5.7%

- Tyman sees underlying operating profit below market expectations

- UBM has trading in line with expectations

- Vodafone nudges up guidance after returning to earnings growth

- Globo says does not anticipate return from administration

- Britain's ITV trading in line, says 2016 looks encouraging

- National Grid to sell majority stake in UK gas unit

- National Grid plans stake sale in UK gas unit in second half

- Capital & Counties Properties on track for 2017 ERV target