Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

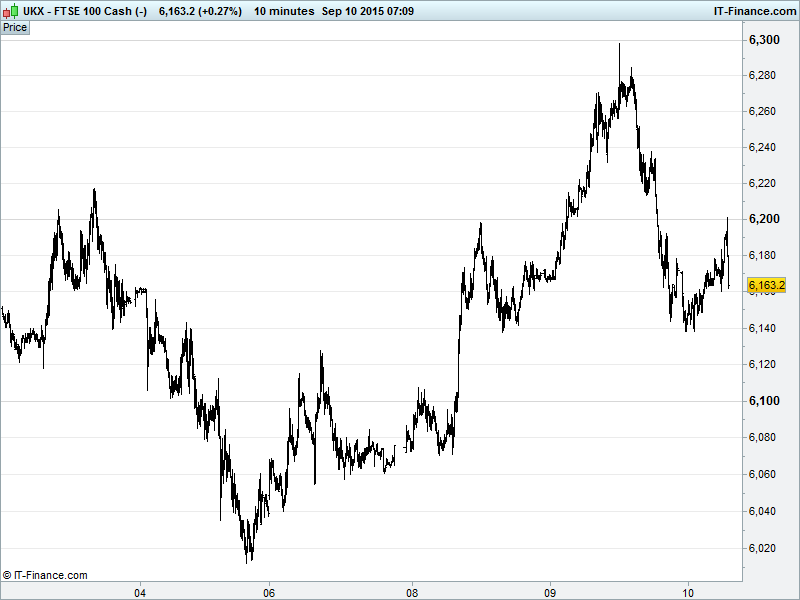

UK 100 Index called to open -65pts at 6160 having retreated from a breakout and test of 6300 yesterday to trade back below 6200 overnight. Support already found at 6140 which, coupled with rising lows at 6100, keeps the uptrend from late August and possibility of further gains alive. If 6200 proves resistant this morning, however, and we break below 6100 it could confirm a fake-out yesterday and the bears take back control. Watch levels: Bullish 6210, Bearish 6090.

The negative opening call comes as a rally inspired by Asian stimulus hopes was spoilt by intensified uncertainty from comments (journalists, Fed members, Central bank peers) about what the Fed FOMC will to do next week (hike or sit tight?) as external macro worries (notably inflation) add to global growth woes and outweigh US jobs market progress.

Asian markets in the red with Japan’s Nikkei giving up some of yesterday’s strong move higher, following a fading of US gains and despite JPY weakness on hopes of more BoJ easing at the October meeting and New Zealand cutting rates for the third time this year. Australia’s ASX underperforming in the region after yet more bad data from China hurt the commodities space and despite good jobs numbers.

Overnight data saw Chinese inflation underscore the nation’s slowing economy; solid Consumer Prices growth helped only by surging pork prices and Producer Prices maintaining their 4.5yr deflationary streak, hitting their worst decline almost 6yrs. Japanese Producer Prices also remained weak, highlighting the pressure from commodity sector correction and its knock-on impact round the world.

While IMF and World Bank have asked that the Fed hold fire, to avoid market panic and emerging market turmoil, several emerging market central bankers (are calling on the US to get on with it and start tightening monetary policy. They obviously see something the others don't.

US bourses edged into the red on Wednesday as an encouraging global rally lost momentum - buying pressure waning as the markets returned from oversold territory. The Fed’s Hilsenrath wrote in an article that agreement is still some way off among fellow Fed members on whether or not to raise interest rates as we head into a crucial week of private discussions ahead of the 16 & 17 Sept FOMC meeting. The data looks good but the global economic outlook is still a little jumpier than many would like.

In focus today will be the UK BoE interest rate decision (no change expected) and especially the MPC minutes for any change in voting and outlook among committee members. Thereafter US Import Prices data is sure to remain highly deflationary, adding to the Fed’s woes, as US Wholesale Sales remain muted and Inventories growth slows.

Crude oil in the red this morning after the Energy Information Administration (EIA) lowered its price forecasts for this and next year (WTI to average $49.23 per barrel; Brent $54.07), all but killing what bullish sentiment there was in the market, that despite also downgrading its forecast for US production. WTI now $44 while Brent currently $48.

Gold ($1106) has returned to test its ‘psyche’ level $1100, trading into a potential bearish pennant pattern that could lead to a break down to $1095, while a sharp rebound is unlikely given that volume likely to remain sparse ahead of the FOMC meeting.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Next reiterates FY sales outlook

- Britain's Next reiterates outlook on 7.1% profit rise

- Home Retail Q2 comparable sales at Argos down 2.8%

- Dixons Carphone Q1 sales climb 8% beat forecasts

- Profit slumps at troubled UK grocer Morrisons

- CLS Holdings sells 6 UK properties for £7.4mn

- Dunelm full – year store like for like growth of 3.4%

- Centamin updates on mineral reserve estimates for Sukari Gold Mine

- EMED Mining Public raises £64.9mn via a placing

- Summer sales lift Darty Q1 French sales