Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

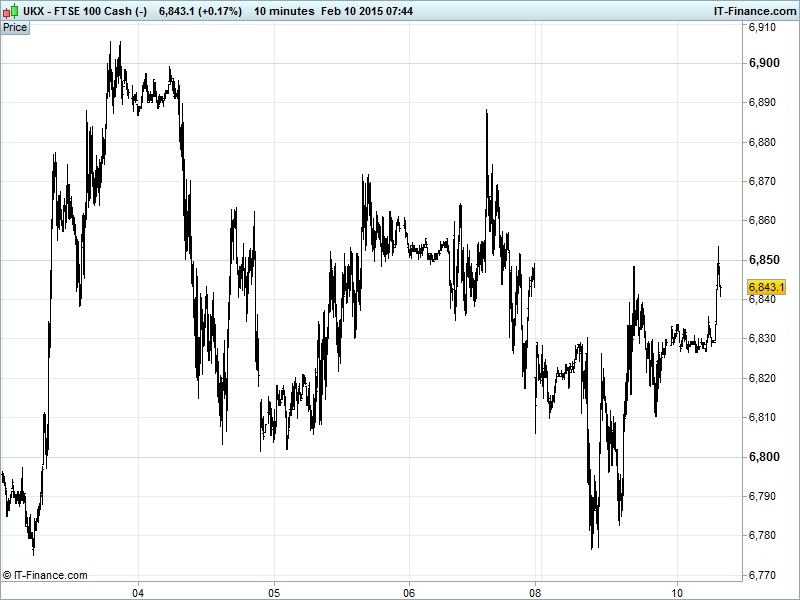

UK 100 Index called to open +5pts at 6842, back above 6800 after spending most of yesterday testing the support level. This brings the index beck into the upper half of its recent 6720-6905 sideways range and while Bulls are hopeful of a revisit of recent highs 6905 the Bears have their eyes on falling highs from 3 Feb. Updated Watch levels: Bullish 6860, Bearish 6770.

The muted open comes from more disappointing China data, this time from January inflation data missing expectations, delivering yet further disinflation signals and suggesting weak demand (international and domestic) but suggesting room for more stimulus. Will UK-listed Miners hold up as well again today? China data showed Consumer Prices (CPI) rising at their slowest pace in more than 5 years while Producer Prices (PPI) made it 35 down months in a row, dented by lower commodity prices. However timing is an issue with many pointing to Chinese New Year falling in January last year and so potential for a rebound in February.

US stocks lower on rising Greek concerns regarding painful and protracted debt negotiations with Eurozone peers and despite Oil climbing on optimism for improved supply/demand dynamics and mixed Fed comments. While German Chancellor Merkel met with Obama regarding Ukraine, she signalled little willingness to compromise with Greece which seeks a bridging loan to tide it over until June while it negotiates with international creditors.

Asian stocks mostly lower, pulled back by mounting concerns that Greece’s standoff with creditors will get messier as well as another bout of poor China data weighing on sentiment. Note mixed Aussie Business surveys and House Price data. Shares in Nissan surged after it upped guidance thanks to a weaker JPY and strong US growth.

In results, Swiss investment bank UBS reported better than expected Q4 earnings (helped by a tax gain) which allowed it to double its full year dividend, although it warned about a strong Swiss franc. Elsewhere, note Deutsche Bank’s FX trading platform being monitored by New York’s banking regulator as part of a probe into currency manipulation.

In focus today we have UK Industrial Production growth expected to again be weak in December and Manufacturing Production to have deteriorated. US Wholesale Sales and Inventories expected to show a slowdown and contraction respectively. The UK NIESR GDP Estimate will be watched given the institute’s upgrade to 2015 growth estimates (2.9% vs 2.5% in Nov) on account of cheaper oil boosting domestic spending.

Growing tensions in Ukraine, bad Chinese data and the increasing likelihood of a Greek exit from the Eurozone have encouraged investors back into safe haven gold for the time being in the face of mounting global uncertainties. The precious metal posted small gains overnight to trade around the $1241 mark this morning following heavy losses last Friday amid glowing US jobs data. Gold remains in a downwards channel from 22-Jan highs. Watch the breached $1252 support level for becoming resistance.

Crude prices have levelled off this morning as oil major CAPEX cuts, falling rig counts and OPEC/IEA predictions of rising demand for its product in 2015 compete for market sentiment with growing US stockpiles and no slowdown so far in OPEC production. US light and Brent crude ($52.16 and $57.62, respectively, this morning) both remain in an uptrend from January lows that is losing steam today. How long can this continue?

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Consumer Price Index Miss, deteriorated

- China Producer Price Index Miss, deteriorated

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Hornby posts 5 pct rise in Q3 group sales

- TUI Group sees earnings up 10-15 pct this year

- African Minerals says lacks funds to meet $400 mln bond payment

- Anite says Q3 trading was ahead of board expectations

- Bellway's housing order book value rises 25 pct in first half

- Hotel chain M&C FY pretax profit falls

- Babcock flags impact of oil price on 2015/16 contracts

- Catlin Group to pay special dividend post sale of auto insurer stake

- Halma sees FY adj pretax profit in line with market expectations

- ICAP Q3 reported revenue falls 2 pct