Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

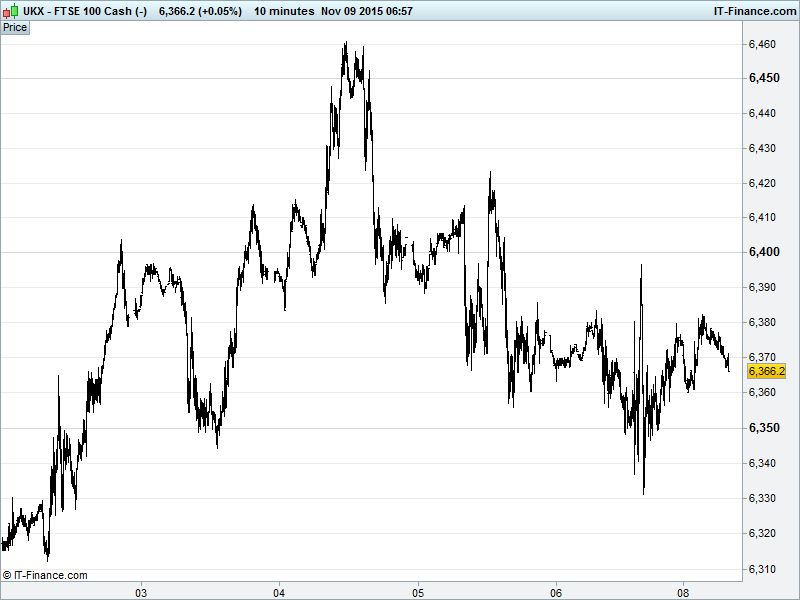

UK 100 Index called to open +5pts at 6360, maintaining its 1-month 6300-6450 sideways shift which the bulls still hope is a pause after the end-Sept breakout at 6270. Still potential for a strong bounce to result in a breakout from a 5-week bullish ascending triangle which could take us back to 6700. While Friday lows preserve rising support since 22 Oct, note however falling highs from last Wednesday. Watch levels: Bullish 6385, Bearish 6320.

The tepidly positive opening call comes despite weekend China trade date providing yet more evidence of slowing growth, with both exports and import contraction missing expectations. Hope burns eternal when it comes to more stimulus. The gains are also in spite of Friday’s strong US jobs report which increased speculation of a Fed rate hike next month. Friday’s flat US close and the positive start to the new week suggests markets either don’t believe it’ll happen or are confident the US economy, and indeed the world, can cope with it.

Asian stocks saw Chinese and Japanese stocks hit 11-week highs with the former moving further into bull market territory on hopes of more stimulus and plans to lift an IPO ban by year-end, while a Fed-strengthened USD/weaker JPY is doing its bit for Japanese exporters and banks. Aussie stocks are the underperformer with losses as the commodities space remains under pressure from a stronger USD, BHP Billiton (BLT) plumbing 7-year lows after the Brazilian dam disaster and the China data highlighting weakness from its biggest trading partner.

US stocks finished flat on Friday yet posted a 6th successive week of gains. Friday’s flat close, however, indicated market indecision regarding a December Fed rate hike after a stellar non-farms print. While a sell-off is often observed when data supports the hawks, it seems that many participants are now expressing confidence both in US economic growth and the Fed’s approach to normalising policy. Over the weekend, the Fed’s Williams said that the decision not to move in October was close and that attention will be firmly on data between now and December.

In focus today, amid a light calendar, will be the fallout from the China trade data and what it means for the slowing economy and further stimulus. While German Trade Data was better than expected, calls for more Eurozone ECB stimulus will be weighed and Eurozone Sentix Investor Confidence will be watched for the hoped for improvement. Note an update to the OECD Economic Outlook is due this morning, while the Fed’s Williams and Rosengren are speaking later this afternoon.

Oil sold off again over the weekend with Saudi Arabia intent on keeping production as is in order to maintain its market share, despite the financial pressure this is putting on its economy. Could we be set to see OPEC whittled down to just one member in the years to come?! Clearly if Saudi is feeling the pinch, many of its fellow OPEC members will be feeling it a lot more.

Gold has made a bounce off $1090 support which could prove to be consolidation ahead of a further slide below $1080 on the back of a surging US Dollar and weakening Euro, making the yellow metal even more expensive to those not using dollars. Could divergent policy between Europe and the US push the gold price below $1000?

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Lonmin announces rights issue to raise gross proceeds of $407mn

- Globaltrans says CEO Sergey Maltsev to leave

- National Grid says Massachusetts electric rate filing submitted

- Elementis says Waterman to take over as group CEO on 8 Feb.

- Underwriter Hiscox reports rise in gross written premiums

- Serco says Australian Armidale contract to end early

- Capital & Counties says conducting strategic review

- InterContinental Hotels says not considering potential sale or merger of co