Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

The UK 100 Index is called to open +45 at 6540pts after a strong session overnight from the US and Asian markets.

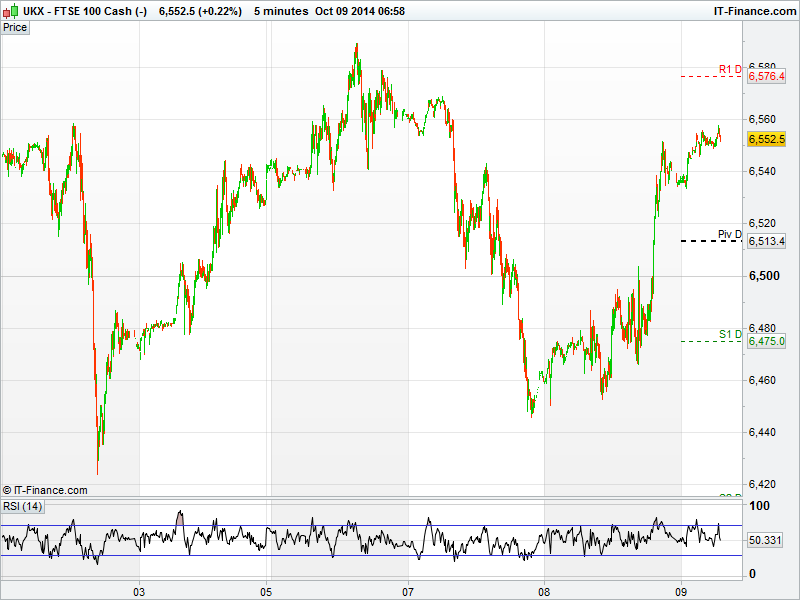

Overnight we have seen some bullish moves in the futures market seeing the UK Index hit highs of 6560, the Dow Jones back over 17,000 and the Dax over 9,100 again. This was due to the comments from the Fed minutes which signal rates would remain low for an extended period of time and as US earnings season kicked off with strong results from Alcoa.

Alcoa reported its highest earnings in three years after prices rebounded and demand around the world increased more than expected. The could have a knock on effect to the European listed miners to power houses like Rio Tinto (RIO.L), Glencore (GLEN.L) and BHP Billiton (BLT.L) this morning.

The UK Index managed to claw back a lot of its losses towards the close, setting up an interesting day to see if the UK Index can sustain the 6550 level again, with stocks reacting to the US earning season.

The best performer was London Stock Exchange (LSE.L) +2.2% as they announced the launch of the UK Index AFSA Australia Bond Index Series, a comprehensive set of fixed-income benchmarks that cover the different sectors of the Australian bond market.

Yesterday the biggest decliner was Tullow Oil -4%, as the Ivory Coast seek investors for seven new ultra-deep water blocks in the Gulf of Guinea which notoriously neglects the production of oil and gas.

Today we have updates from Hays (HAS.L), John Wood Group (WG.L), and PepsiCo in the US. Watch out for any more ‘out of the ordinary movements’ after Alcoa’s result last night.

Asian stocks rose for a third day this week as Federal Reserve concerns over a global economic slowdown spurred bets that U.S. interest rates will remain low. The Dow Jones finished positive up 1.6%, just shy of the 17,000 level having rebounded from lows for its biggest one day gain this year.

In commodities, WTI traded nearest lowest levels since June 2013 and London’s Brent was at the weakest level since June 2012 after crude stockpiles surged more than forecast in the U.S. Gold after recent trouble is heading for the longest rally also since June as Federal Reserve officials expressed there could be a slowdown globally, weakening the dollar and boosting demand for a haven. FX – the dollar fell to a two week low against the euro as investors pushed back bets for when the fed increase interest rates.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- JP Machine Orders Better

- AU Employment Change Worse

- AU Unemployment Rate In-line

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- John Wood says trading in line with expectations

- Centamin ramps up gold production at Sukari mine

- Polar Capital assets rise to $13.4 bln over six months to end Sept

- N Brown Group H1 revenue down 0.6 percent

- Hays posts 4 percent rise in first quarter net fees

- Old Mutual says OM Asset Management IPO priced at $14 per share

- IGas teams up with partners to bid for new UK shale gas licences

- Vernalis licenses V2006 to RedoxTherapies

- Rolls-Royce selected by Norwegian for nine Dreamliner engines