Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

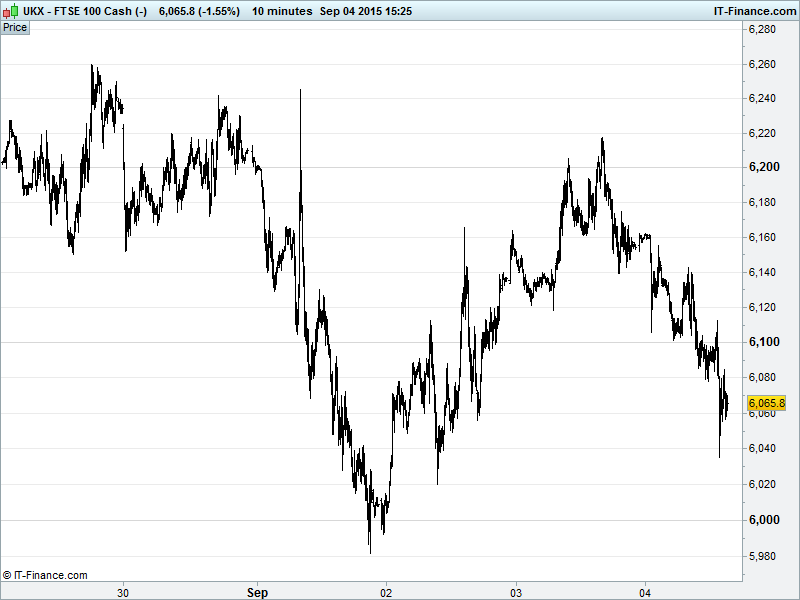

UK 100 Index called to open +110pts at 6255 having seen an overnight break above the recent bugbear trend of falling highs from 28 Aug at 6200. However, yet to exceed the 6260 high of late last month that we have been concentrating on. The breakout keeps alive the uptrend from 2015 lows in late August and raises hopes to a revisit of 6700 however, not without the breakout bettering the 6260 level highlighted. Watch levels: Bullish 6270, Bearish 6190.

The positive opening call comes after Asian markets rallied strongly overnight on hopes of more stimulus with Japanese PM Abe reiterating plans for a cut in corporation tax, China’s Ministry of Finance saying it would remain ‘proactive’ in terms of fiscal policy to stimulate a clearly slowing economy and the World Bank echoing the IMF by warning the Fed against rising rates.

The bullish combination has driven Japan’s Nikkei up a whopping 7.7%, its strongest performance since October 2008 and post Lehman collapse, following an already positive US and European sessions, while Commodities have extended recent gains on the prospect of China stabilising both its financial market and growth, in spite of USD resilience on rate rise uncertainty.

US bourses returned refreshed from their holidays to post impressive gains amid signs of returning stability in Asian markets. Three Democratic senators announced they will vote in support of the Iran nuclear deal taking the number of senators publicly backing the deal to 41, enough to keep those pesky Republicans from mucking things up.

Post-close Fed chatter from Narayana Kocherlakota went all academic on us – with the Minneapolis Fed chief saying there’s been a significant decline in the US long-run neutral real interest rate. Here comes the science bit: The neutral real interest rate refers to the real interest rate that would prevail if the economy was at maximum employment and inflation was at target – it’s unobservable because it’s in the future, but a nonetheless important number for economists. The upshot of a decline in this figure could be that employment and inflation targets will remain elusive in the longer term, making a data-led interest rate rise pretty difficult to qualify.

The debate on the Fed rate hike intensifies as we move into the final furlong before the September policy update next week with the World Bank warning against Fed risking triggering panic in Emerging Markets and should hold off until the global economy is on a better footing. This follows market volatility related to China growth fears and a summer rout for equities.

Data overnight included poor UK BRC Shop Price data which failed to recover (-1.4% v -0.2%e) as hoped and adds to recently weak BDO survey and BRC Sales data. It's tough on the UK High Street. Aussie Consumer Confidence dropped along with Home loans while Japanese Consumer Confidence improved.

In focus today will be UK Industrial and Manufacturing Production which are seen delivering muted growth in July although for the former this would represent a rebound, while we also get an update to the UK NIESR GDP estimate for growth in the 3 months to end-August. Better than 0.7% posted in July? Note speakers today include the EU’s Juncker, German Chancellor Merkel and Chinese Premier Li this morning.

Crude oil benchmarks rallied during the Asian session but off their highs this morning on that Iran nuclear deal coming 3 steps closer and a rallying USD basket, both of these testing the uptrend from 8 Sept lows. WTI ($46) has nonetheless seen overnight resistance turn support while Brent ($50) moving into a rising wedge pattern.

Gold ($1122) has broken below rising support from 7 Sept as a resilient US Dollar and renewed confidence in equity markets weigh down on demand for the safe haven yellow metal (no need for straw-clutching drivers like the Indian monsoon this morning…).

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- IAG, British Airways passengers, crew escape plane fire in Las Vegas

- Oil markets rise as Asian stocks soar

- Ryanair hikes annual profit forecast by 25 pct after strong summer

- Monitise says Elizabeth Buse to step down, Cameron appointed new CEO

- Quindell says to acquire remaining 50.1 pct of PT Healthcare

- Hargreaves Lansdown says FY pretax profit down 5 pct

- Barratt Developments year profit up 45 pct

- Max Petroleum gets Kazakh govt's approval for AGR Energy subscription

- Genel Energy updates on receipt of payment for KRI oil exports from Tawke field

- London copper hits six – week top as sentiment improves