Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

UK 100 called to open +15pts at 6870 with Asian markets boosted by weekend Chinese trade data that showed faster growth than expected in May (exports accelerating, trade surplus widening) and Japanese Q1 GDP was revised higher this morning adding to the positive reaction to Friday’s US jobs report which beat expectations and saw the number of Americans in work pass the pre-crisis peak milestone.

The US closed higher on Friday after Non-Farm Payrolls beat expectations (217K vs 210K est) and the US unemployment rate (6.3%) stayed at its recent low which was seen as enough to maintain the Fed’s easy policy and existing market risk momentum, helped by S&P saying the US could regain its AAA rating if there is additional evidence of bipartisan efforts that signal reduced political brinkmanship.

Encouraged by US data and positive close to the week, Asian markets delivering similar performance to US counterparts with Japan’s Nikkei opening at a 7-month high (weaker JPY) after upwardly revised Q1 GDP data while Hong Kong’s Hang Seng is following Shanghai higher on the strong Chinese Trade data which is in turn benefiting Australian equities - watch the miners in particular with China being the largest trading partner.

Over the weekend the new Ukrainian President was sworn in and pledged peace with Eastern Ukraine whilst calling on illegal arms to be surrendered, stating Ukraine will not compromise on Crimea or on EU choice. Russian president Putin said an immediate ceasefire was needed if talks are to be had and that Russia will implement protectionist measures if Ukraine signs the EU deal. Welcome back geopolitical risk.

After the big ECB move of last week (rate cuts negative deposit rate, TLTRO) note Coeure saying rates close to zero for an extremely long period versus US and UK which will enter rate rise cycles. Stateside, the Fed’s Fisher refrained from giving a timeframe for a rate hike (depends on economic conditions) but said he would call for an end to QE in October as it does not make sense to taper only $5bn in December.

In focus today, with many European markets closed for Whit Monday, will be the Eurozone Sentix Investor Confidence figure for June, which is expected to inch higher and the UK Lloyds Employment Confidence indicators. In the afternoon, the Fed’s Bullard and Resengren are speaking.

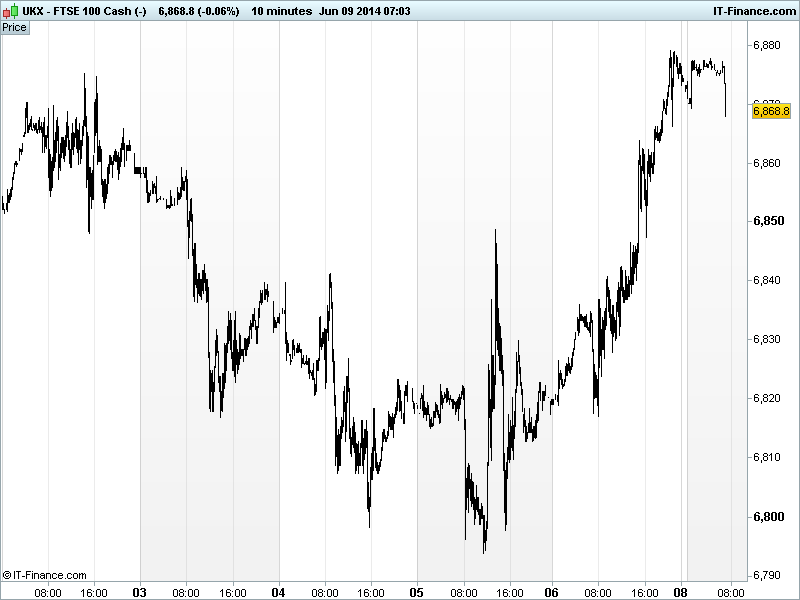

The UK index made a late Friday attempt at recent highs 6883, helped by US markets holding higher on S&P’s talk of a US upgrade if political brinkmanship was reduced and better than expected US consumer credit data. Nonetheless, 6880 remains to be beaten overnight, even with the better Chinese trade data: Imports slump highlight growth risk. Resistance 6883, support at 6795.

In commodities, Gold continues to trade $1250-1255, off its lows of $1240 following the ECB easing and US jobs report but unable to get back above the $1260 mark. Whether it is safehaven demand or bargain hunters doing the bidding, we look to have simply moved from one sideways range to another with today’s lack of data not helping things in terms of drivers.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- CN Trade data Beat, Improved

- JP GDP Beat, Accelerated

- JP Sentiment indices Beat, Improved

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Falkland Islands Holdings underlying pretax profit rises 10.8 pct

- Sound Oil says Italian reserve estimates rise

- Costain wins new gas terminal contract with Centrica Energy

- Green Dragon says FY revenues rise on higher output

- Lloyds Bank prices TSB stock market listing below book value

- Sports Direct convenes vote on 2015 bonus scheme for Ashley