Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

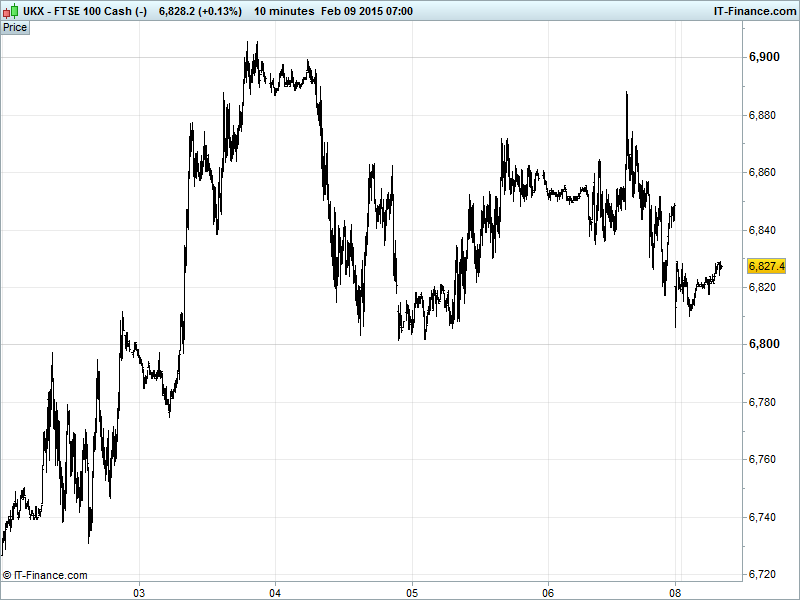

UK 100 Index called to open -30pts at 6820, back down at Weds/Thurs lows from a post-NFP foray towards 6905 recent highs on Friday. Support around 6800 keeps the index in the upper half of its recent 6720-6905 sideways range from Jan 21, which keeps alive the possibility of a breakout and test of all-time highs 6950. Bears looking for a breakdown. Updated Watch levels: Bullish 6880, Bearish 6790.

The negative open comes via revived global growth fears after Chinese Trade data disappointed with exports posting a surprise slump (difficulty with slack international demand and stronger currency) and putting an exports led recovery in jeopardy, while growth at home slows (imports crashed). This morning’s German trade data also offered mixed picture (exports rebound, imports contract).

With Friday’s strong US Jobs report increasing the likelihood of a June Fed rate hike and offering potential for US Q4 GDP to be revised higher, coupled with the recent RRR cut by the PBOC, recent data just goes to highlight the divergence in growth prospects and monetary policy among major nations and central banks.

The new Greek government’s hard-line stance on not seeking a bailout extension end-Feb and undoing the shackles of austerity is also keeping Eurozone jitters to the fore, putting the country on a collision course with international creditors, while S&P downgraded the nation’s debt further into junk territory. Geopolitical risk still highs with new talks (futile?) on a resolution to the Russia-Ukraine situation.

US stocks closed higher following the stronger than expected US jobs report, notably in upwards revisions to Nov/Dec and acceleration in wages growth, which stoked speculation of a Fed rate hike coming sooner than expected. The Fed’s Lockhart said the data put the Fed on-track for a hike in mid-2015 or a bit later.

Asian stocks mixed following poor China trade data, with the drop in exports and plunge in imports weighing on sentiment and putting an end to the recent run of gains for Australia’s ASX (China is its major trade counterpart) despite a weaker AUD, with political influences holding sway after PM Abbot survived a no-confidence vote but could face upcoming threats.

Japan’s Nikkei a touch higher thanks to a NFP-induced stronger USD and thus weaker JPY as well as better Japanese trade data and comments from the BoJ that the virtuous cycle is working in the economy, and although Consumer confidence improved, it missed consensus while Business sentiment was mixed.

In focus today will be the fallout from the China trade data and what it means for global growth sentiment and/or hopes of more stimulus from Beijing as well as the divergence with the strong US jobs report. Data of note is the Eurozone Sentix Investor Confidence reading with an increase expected.

Gold ($1237) regained some lustre over the weekend, having sunk below support at $1255 on Friday following glimmering US employment data that strengthened the USD and brought hunger for risk back to the markets at the expense of the yellow metal safehaven. Stabilisation came amid Greece’s continuing disagreement with the ECB and deepening worries about the escalating conflict in Ukraine. Watch for the breached support line reverting to resistance.

Despite the stronger USD following the US Jobs report, the price of Oil has held up after the Baker Hughes rig count again fell, fuelling further concerns over supply while the slump in demand from China put opposing pressure on the commodity. The news saw Brent crude ($57.99) levelling off +20% from 6-year lows reached in January. US Light Crude ($52.06) also stabilised this morning with support at rising lows from 30-Jan.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight/Weekend Macro Data: (Source: Reuters/DJ Newswires)

- China Trade Balance Beat, surplus grew

- China Exports Miss, dropped

- China Imports Miss, plunged

- Japan Consumer Confidence Miss, improved

- Japan Business Outlook Beat, improved

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Lund starts new BG CEO role early

- Max Petroleum says to be insolvent without debt restructuring

- Max Petroleum says needs investment, debt restructuring to stay afloat

- UK's Hornsea gas storage site in unplanned partial outage-SSE

- Land Securities says to proceed with Westgate Oxford development

- Rolls-Royce wins new $442 mln contracts for U.S. fighter jet

- ARM buys Dutch 'Internet of Things' software firm Offspark

- New Britain Palm Oil says Sime Darby shortens offer period

- Fastjet says January load factor at 69 pct