Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

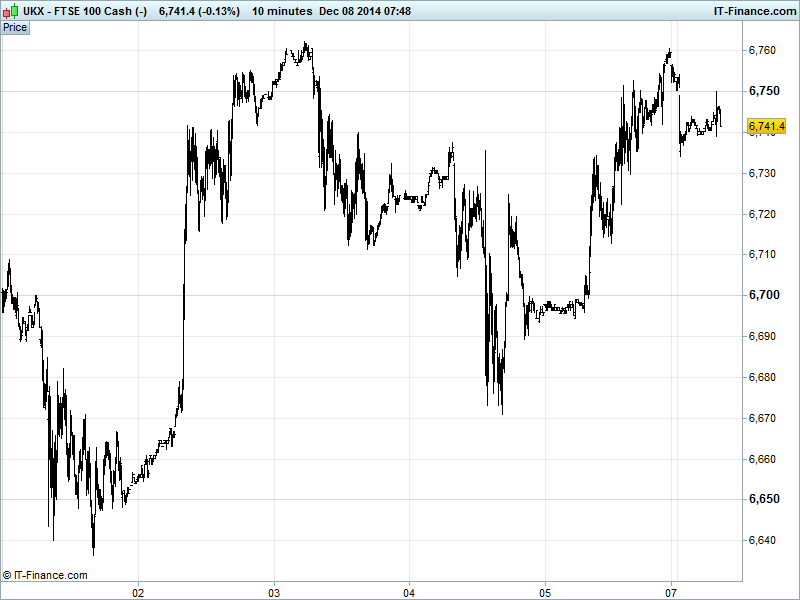

UK 100 Index called to open flat at 6747, back from Friday’s highs and another failed attempt at 6760 following the US Jobs reports. On the hand is suggests the level is building as resistance, on the other hand as we move sideways above 6700, there is potential for this to be a pause before a resumption of the Oct/Nov uptrend/recovery. Watch levels: Bullish 6780 and Bearish 6660.

The flat opening call derives from uncertainty following a host of disappointing macro-economic data overnight with Japanese GDP confirming that Q3’s recession is worse than previously estimated (annual and quarterly) along with a worsening October Trade deficit and decline in November business sentiment surveys.

This is coupled with a Chinese November Trade Surplus rising to an unexpected record high, but at the expense of growth in both exports and import, with the former slowing markedly and the latter actually dropping into contraction suggesting a worsening of the slowing growth trend in the world’s #2 economy. Note the China’s People Daily reporting that China can accept growth a bit lower than 7.5%.

As we write, and after last week’s poor Eurozone PMI readings and the Bundesbank halving its German growth forecasts, the region shows it remains troubled and in need of intervention by the ECB, with German Industrial Production slowing in October and missing estimates, in contrast to last week’s Factory Orders which surprised to the upside with a better rebound.

US Stocks closed higher on Friday after the blowout US Jobs report (321K jobs created vs 230K forecast; prior month revised higher), even if the unemployment rate was unchanged. After the European close an S&P upgrade for Ireland helped Eurozone recovery sentiment, but this was countered by a cut for Italy on recent weakness.

Overnight, Asian equities positive thanks to positive lead from US equities with the US Jobs report boosting optimism, and despite disappointing data for Japan (GDP) and China (Trade), with Australia’s ASX positive (helped by Banks on financial reform and airline Qantas upbeat guidance on a return to profit thanks to lower oil prices) Shanghai still benefiting from last week’s gains (but not without volatility) and Japan’s Nikkei flat along with Hong Kong’s Hang Seng.

Interesting to see no great weakness there or in European opening calls following the German Industrial Production prints. Hopes still high of the ECB delivering QE in the New Year and maybe even US Jobs reports suggesting recovery but not enough to bring about a very early 2015 rate rise, with markets still relying on accommodative central bank stances for the near future.

In focus today, we have little major data bar the Eurozone Investor Sentiment which is seen improving in December while any improvement in the Lloyds UK Employment Confidence and US Labour Market Conditions will be welcome. Speakers include the BoE’s Weale and Gracie and the Fed’s Lockhart.

In commodities, Gold has fallen below $1200 after the US jobs report on a stronger USD on expectations of recovery leading to a rate rise and higher borrowing costs. The price of Oil remains under continued pressure with US Light Crude at $65.3 and Brent at $68, both near recent lows on the trade-off between rising production and waning demand.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan GDP Miss, deteriorated

- Japan Trade balance Miss, deficit grew

- China Trade Balance Beat, surplus grew

- China Exports Miss, growth slowed more

- China Imports Miss, contraction

- Japan Sentiment Surveys Miss, deteriorated

- Germany Industrial Production Miss, growth slowed

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Centrica makes Norwegian sea gas discovery

- Songbird Estates shareholder Madison backs Qatari bid

- Illegal strike forces Avocet Mining to halt Inata mine operations

- BHP Billiton names spin – off company South32

- UK insurer Esure to buy remaining 50 pct stake in Gocompare.com

- Quindell says resources sufficient to deliver management's current plans

- IHG agrees to sell Paris – Le Grand to Constellation

- Segro sells German industrial estates to Hansteen for 46 mln eur

- Carillion signs 75 mln stg contract for Liverpool Football Club