Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

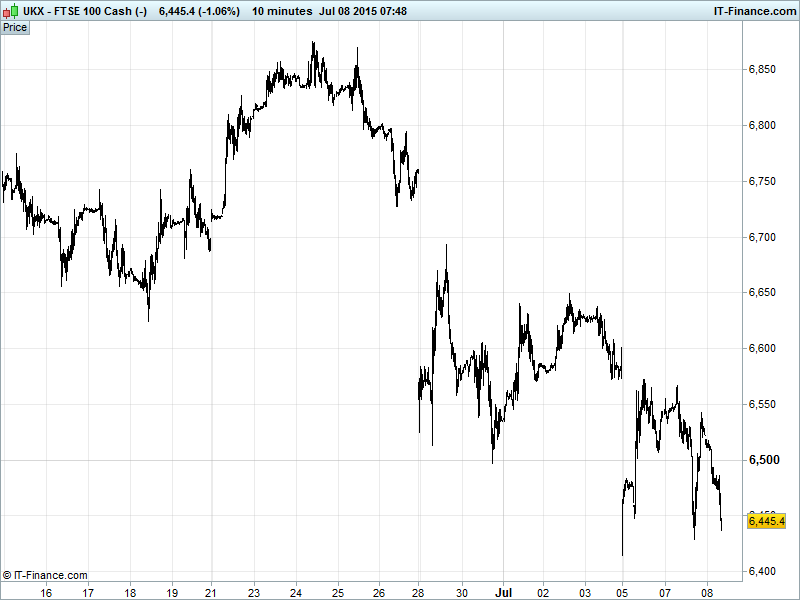

UK 100 Index called to open +5pts at 6435, however yesterday’s late 120pt bounce has all but evaporated after falling resistance again proved too much of a hurdle at 6550, keeping it in a clear short-term downtrend. The Bulls are clinging to the fact that the longer-term uptrend from October is unbroken with support at 6400. For the Bears, the current trend (down) is still their friend. Watch levels: Bullish 6530, Bearish 6390.

The positive opening call comes after an impressive rally stateside on Tuesday with markets shaking off early losses to bounce back seemingly on hopes that an end to the Eurozone / Greece showdown is on the horizon, Athens having been given until Sunday (ECB guaranteeing minimum liquidity for Greek banks until then) to come to the table with proposals while Grexit contingency plans are drawn up by Creditors.

Incidentally, the European Central Bank is now the hair holding the Sword above the head of the Greek economy that, in the event of a 20 July default on ECB bond repayments, may just break. Such a default is certain to ramp up pressure on Mario Draghi to stop accepting Greek debt as collateral for Emergency Liquidity Assistance (ELA) loans. Greece’s banks have precious little else, if anything, to put up and face instant collapse if no workaround can be found.

US bourses the comeback kings of yesterday with the Dow converting a 218pt loss to a nigh on 100pt gain as a China-inspired commodities rout abated to couple with Greece in causing massive swings in the markets. Elsewhere, the IMF gave the US economy a check-up overnight, concluding that the Dollar’s strength (Dollar Basket +20% in the past 12 months) makes a 2015 interest rate hike a genuine threat to growth while US share prices are nearing unsustainable levels.

Asian markets well bloodied overnight slipping into correction territory as China’s equity rout continues falling their most since 2007 to hit 3-month lows, denting regional sentiment. Fresh stabilisation measures proving fruitless (see what we wrote yesterday) as traders unwind at great pace. Mass trading halts will just worsen the panic when stocks eventually reopen as pent up demand to sell is released.

The prospect of more waiting for a Greek bailout decision is also weighing after Creditors were obliged to employ much more aggressive language than usual at last night's emergency summit giving Athens a final deadline of Sunday to accept a tougher rescue plan than proposed pre-referendum, or else they are out of the Euro. So asking the people was worth it, wasn’t it?

However, the fact that other world leaders (US, China) are weighing in does suggest that we could be at a more crucial point than we ever have been with them fearful of ramifications of a Grexit. Could their interjection help deliver a more market amendable solution?

Today’s main events consist of speeches – we’ve got the EU’s Juncker at 11am, George Osborne’s summer budget statement at 12.30pm while US Fed meeting minutes round off the day at 7pm. Macro-data (a quiet day on that front) has US mortgage applications and weekly oil stocks presenting the most likely market drivers – although other things should eclipse this particular oil print. See the live Macro-Calendar for a rundown.

Gold looks set to revisit mid-march and 7-month lows of $1142 as its declines persist and the safehaven metal is shunned despite plenty of uncertainty (China, Greece) to go round. Strong USD not helping. Now broken below shallow falling support at $1155.

Oil pared yesterday afternoon’s price plunge overnight but back on the back foot this morning having failed to reverse a 14-day downtrend (part of a much longer term one, of course). Bears will be looking to an Iranian nuclear deal this week and more ‘big trouble in little china’ to drive a return to Tuesday’s lows (WTI $50, Brent $55.5) where optimists will want to get in on a missed deadline (in Iran talks) and subsequent bullish double bottom reversal. Current levels: WTI $51, Brent $56

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Wincanton appoints Tim Lawlor as group finance director

- Stagecoach's UK rail franchises extended

- Monitise says Visa Europe to reduce stake in co

- SABMiller names De Lorenzo as CFO on permanent basis

- Booker Group says on track to meet full – year expectations

- Barclays announces departure of CEO Anthony Jenkins

- Rio Tinto Kitimat smelter begins production