Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

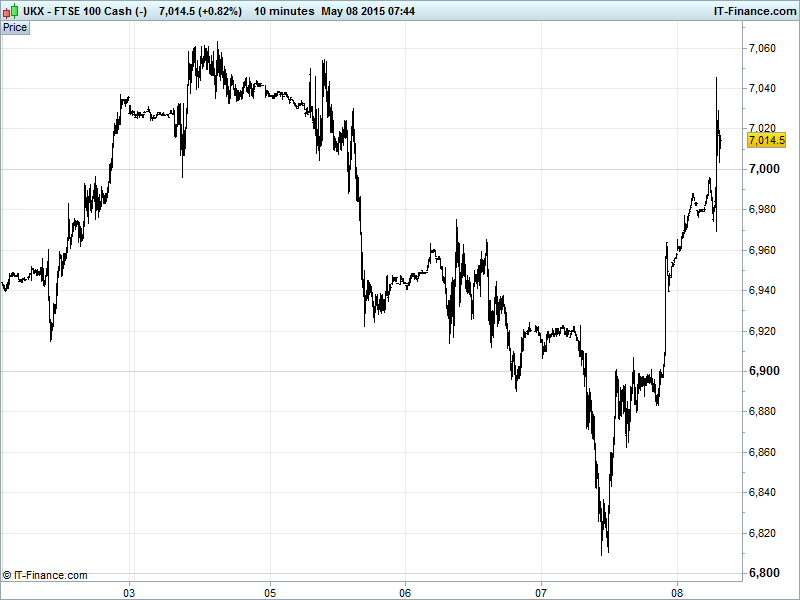

UK 100 Index called to open +130pts at 7015, making a significant recovery from the recent Fed Chair Yellen-fuelled sell-off to near 6800. This comes thanks to exit polls from the UK General Election suggesting the Conservatives could win an outright majority and maintain power. A move back to 7000 gives that all-time highs, achieved with Tories in power can be repeated. Watch for resistance at ceiling of recent falling channel at 7025. Watch levels: Bullish 7065, Bearish 6940.

The positive open comes after the Conservative party look to have won the UK general election by a wider margin than expected leaving open the possibility of an outright majority for incumbent prime minister David Cameron. The Pound Sterling has surged at the prospect of a further five years under a ‘pro-business’ government looking to finish the job of overseeing the UK’s economic recovery. In what many have seen as rather shocking results compared to the neck and neck polls conducted in the run up, Labour has done much worse than expected having lost Scotland to the SNP, while the Liberal Democrats have been absolutely slaughtered.

US bourses shrugged off Yellen’s comments about ‘quite high’ equity valuations to close ‘quite higher’ on Thursday, although the Dow Jones sits some 300 odd points below all-time highs hit on 2 March. Potential for the index to make gains today in reaction to the UK’s election result but more pressing will be the in-focus macro data for today: the Change in Non-Farm Payrolls where consensus is for 230,000 new jobs to have been created in April. We note last month’s print came in disappointing, arguably stalling May advances in US equities somewhat. Will today’s data return some confidence to the markets? In other news, the Fed’s Evans has been speaking, remaining dovish on a US rate hike and, while confident in a second quarter bounce-back from a disappointing first, reiterating his stance: A rate rise should not take place until 2016.

Asian stocks largely positive albeit cautious, tracking US equities higher on hopes of bond market stabilisation after the recent sell-off ahead of the April US jobs report, with equities seeing an element of bargain hunting. Australia in the red after Chinese trade data painted a bleak picture with exports failing to rebound and imports again contracting strongly with continued economic headwinds, both domestic and global. Japan’s Nikkei rebounded helped by robust performance by Nintendo delivering its first profit in 4 years.

Central banks in Asia saw Japan’s BoJ gave no easing hints (gradual recovery, QE working) while Australia’s RBA statement failed to provide any forward guidance in the wake of its recent rate cut (to boost consumer demand), but gloomily trimmed 2015-16 GDP forecasts to below trend.

Brent Crude ($65) has dropped out of what was an encouraging rising channel for oil bulls yesterday, finding support at May lows $65 following a bounce in the US Dollar Basket – which is nonetheless in a downtrend. Potential for a recovery to test resistance at the rising trend line that has was support until Thursday morning. US Light ($59), meanwhile, has had a similar pullback, though less far to travel to recover its own uptrend having found support around $58. Note both benchmarks have made double bottoms at respective support.

From the UK election result, watch for the stronger GBP as well as potential gains for sectors like Utilities and Real Estate/Property and Bank shares which should benefit from the Conservative status quo after fears of Labour introducing tougher regulations in each industry. Note this morning’s March German Industrial Production coming in weaker than forecast.

Gold hovering around $1185 with equity markets’ recovery and a stronger USD muting any demand for the safehaven even as uncertainty from the UK election appears misplaced, Greece once again takes debt negotiations down the wire, we await the latest update on the state of the US jobs market and China trade data revives concerns about economic slowdown. Support $1180, Resistance $1200.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- China Trade Balance Miss, lower surplus

- China Exports Miss, dropped

- China Imports Miss, dropped by more

- Germany Trade Balance Miss, flat

- Germany Industrial Production Miss, weaker than expected

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Man Group seeks new chairman as Aisbitt plans May 2016 departure

- Man Group funds under management rise 7 pct to $78 bln

- Rolls – Royce keeps guidance, eyes currency drag to revenue

- Just Eat to buy Australia's Menulog for 445 mln stg

- Monitise and IBM win Société Générale's mobile banking contract

- Laird reaffirms full year outlook

- BG earnings take further hit from weak energy prices

- Royal Mail CEO Moya Greene joins Great-West Lifeco Inc as Non-exec