Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

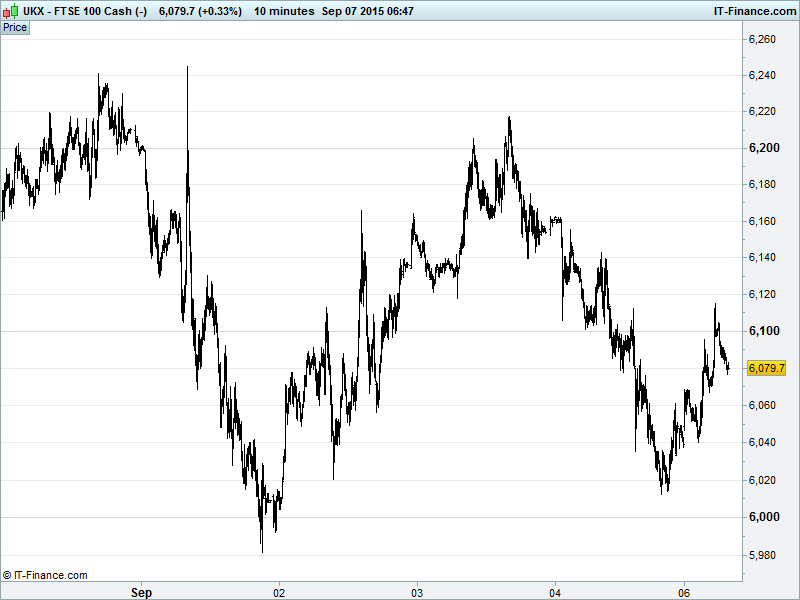

UK 100 Index called to open +45pts at 6085 having rebounded from 6010 late on Friday which gives us shallow rising support from 26 Aug, however, still held back by falling highs from 21 Aug which puts resistance around 6190. We still think Bulls need a break above late Aug highs 6260 before getting really motivated, while the bears are watching for a meaningful breach of 6000. Updated Watch levels: Bullish 6270, Bearish 5970.

The positive opening call as Chinese stocks resume trading on a positive note after a 2-day holiday and despite 2014 official growth for the world’s #2 economy being revised down to 7.3% from 7.4% (already below target 7.5%) adding to debate about slowing growth and whether 2015 will manage 7.0%. Confident comments (rout nearly over) from the PBOC helped buoy sentiment while G20 meeting sought to dispel China fears (nothing to worry about) with a rosy economic outlook.

Confident comments (equity rout nearly over) from the PBOC helped buoy domestic China sentiment initially while the weekend’s G20 meeting sought to dispel China fears (nothing to worry about) with a rosy economic outlook and belief in a limited negative knock-on, which sounds rather optimistic especially after the downbeat message delivered by ECB President Draghi last Thursday.

Stocks in Asia mixed overnight with China and Australia in the red (stronger AUD) on global growth concerns and still depressed commodity prices while Japan’s Nikkei in the green but having swung between gains and losses after a US jobs report provided little comfort to those seeking clarification on whether the Fed will move to raise rates this month and Toshiba slashed earnings for the past 7 years after accounting irregularities which came to light earlier this year.

US stocks fell on Friday after a soft US jobs report (lowest gain in payrolls since March 2015) shone little light on a 2015 Fed rate hike while we note that August usually proves a notoriously bad month for the first payrolls estimate, leaving the possibility open that an otherwise encouraging set of employment numbers (jobless rate lowest since 2008) could lead to an upwards revision next month. US markets closed today for Labor Day.

On the corporate front, big news this morning comes from mining giant Glencore (GLEN) which has announced fresh plans to cut its $30bn debt pile by a third with a $2.5bn rights issue and dividend cut as well as asset sales. Elsewhere, Tesco (TSCO) is to sell its South Korean operations Homeplus for £4.2bn which goes some way (enough?) to cut £22bn debt-ridden balance sheet and avoid a rights issue after sale price expectations for Dunnhumby data analysis business (Clubcard) were scaled back sharply last month (£700m vs £2bn) following results showing reduced profitability.

In focus today, in the absence of any US macro data (Labor Day holiday) and Eurozone data limited to the Sentix Investor Confidence (9.30am; forecast to decline), will be the fallout from Friday’s mixed and messy US Jobs report and its impact on the Fed’s decision whether to hike rates (it won’t in our view) as well as the return to trading (and volatility) by Chinese markets after a 2-day national holiday. Given the refugee crisis gripping Europe, note EU President Donald Tusk speaking after the European close.

Crude prices down slightly despite an overall fall in the number of operational US drilling rigs – traders clearly looking at a rise in the number of offshore rigs. Russian deputy PM said that OPEC producers are starting to suffer the ricochet effects of attempts to flush out rivals by flooding the market and that they can’t stomach low prices for much longer which means some form of change in policy may come about. Brent $49; WTI $45, both in a downtrend since end-Aug.

Gold ($1123), up a little from Friday but now well back from August highs $1170 as many expect a US rate rise in 2015 – still unlikely in our view – with USD strength dulling demand for the non-interest bearing yellow metal and a certain amount of relief and affirmation regarding China keeping investors risk-on.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Glencore to announce plan to cut debt, shares halted

- Tesco sells South Korean unit to MBK–led group for £4.2bn

- Primark owner AB Foods maintains year guidance

- UK's North Sea loses 5,500 jobs in oil market downturn - regulator

- Man Group China head says she was not investigated by authorities

- Australia's Starpharma soars on drug delivery license with AstraZeneca

- London copper firms in thin trade; China data deluge eyed

- Segro considers selling office portfolio in Slough

- Faron Pharmaceuticals says to float on AIM

- Shield Therapeutics to float on LSE, seeks to raise £110m

- Dechra Pharma FY revenue +10%

- Worldview says exercising right to convene Petroceltic EGM

- Quindell confirms CEO appointment

- APR Energy gets govt approval of extension on 250MW power project

- Britain's main manufacturing lobby has halved its forecast for growth this year after overseas orders fell to their lowest since the financial crisis, while recruiters said skills shortages were leading to higher wages but slower job growth.