Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

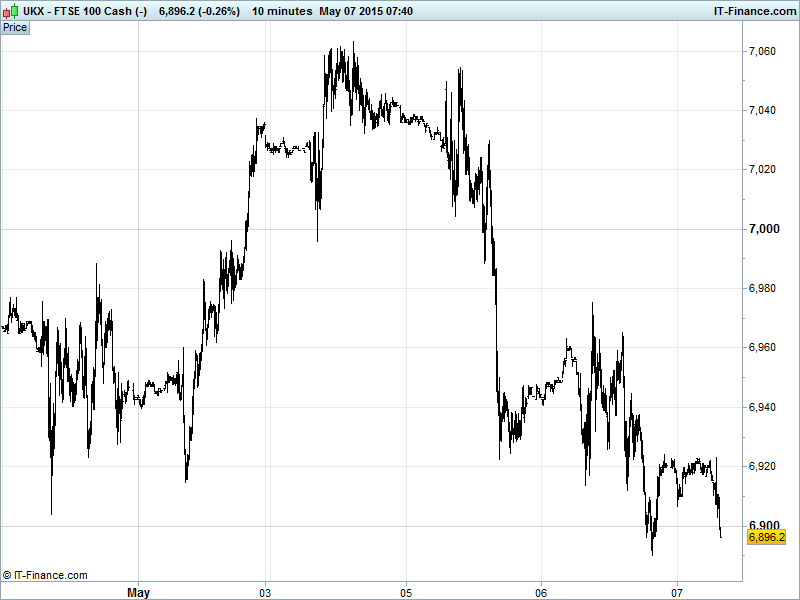

UK 100 Index called to open -30pts at 6900 having given up ground late yesterday following a positive but volatile pre-Election session before finding overnight support at 6890. Index still in falling channel since mid-April. Still potential for bounce towards 7040 ceiling of falling channel pattern, but also for further downside from bearish head & shoulders pattern after break below 6920. Watch levels: Bullish 6990, Bearish 6875.

The softer open comes in the run up to the closest run UK election since World War 2. Significant losses on Wednesday from a poor set of J Sainsbury results were offset by gains in Vodafone and Imperial Tobacco shares as the former benefited from a broker upgrade while IMT restarted quarterly dividends after posting an increase in 1st half profit. Eurozone woes tipped the balance to the downside, however, despite Greece making a €200mn payment to creditors yesterday and the ECB increasing ELA for Greek banks as Eurogroup chief Dijsselbloem wrote off the possibility of a deal by Monday 11th, leaving the Athens government under significant financial pressure ahead of another debt repayment deadline next week.

US bourses failed to recover fully from Wednesday’s early losses after Fed chair Janet Yellen warned about the potential dangers of ‘quite high’ equity valuations. The comments took investors back to Alan Greenspan’s 1996 ‘irrational exuberance’ speech, which was followed four years later by the 2000 stock market crash. Yellen also warned about the possibility of sharp long term interest rate rises coming soon after a decision to start hiking in the first place. Lockhart took things further and suggested the FOMC would soon be considering policy change, playing down a weak first quarter performance by the US economy and expecting a bounce back in the second.

Asian stocks in the red, with the regional benchmark headed for a 1-month low on sluggish US economic concerns, Fed Chair Yellen’s warning on overvalued equities, continued worries over the Greece and China and tomorrow’s US jobs report. Japanese stocks see exporters hurt by a stronger JPY (driven by USD weakness on mixed econ data) as they reopen after Golden Week holiday, ignoring an improvement to growth for PMI Services and echoing US market declines.

Shanghai stocks extended losses ahead of tomorrow’s trade data with Morgan Stanley and BNP Paribas sounding the alarm on Chinese stocks, citing weaker corporate profits growth and margin debt worries. Note ratings agency Fitch saying “China slowdown as expected but downside risks mounting”. Australia’s ASX lower after disappointing jobs data and contraction in construction vindicated the RBA rate cut.

In focus today is, surprisingly, the UK general election. It really is anybody’s guess as to who will team up with whom in the aftermath of what is hotly tipped to be a hung parliament, with polls suggesting neither the incumbent Cameron nor his main challenger Miliband will secure the majority needed to govern alone. It is left to British business leaders now to weigh up which combination will be ‘least bad’ for them, assuming the execs’ favourite Cameron won’t be getting in without a little help. Or a lot of help.

Gold ($1188) fallen below $1190 following Fed comments which heightened speculation that a jump in bond yields after a US rate rise could hurt bullion demand. Safehaven demand muted despite plentiful uncertainty related to Greek debt, China slowdown, US rate rises and the UK election. Falling highs could find some support around $1185.

Oil off its best levels after further advances yesterday but maintaining its uptrend with WTI and Brent spiking to hit $62 and $69/barrel respectively helped by the weaker USD. Sentiment checked after fresh comments from Fed (rate rise) and Iran (output to increase if sanctions lifted; deal by end-June?) as well as a surprise drawdown in US stockpiles. Demand supported by fears of fighting (Libya, Yemen) disrupting regional supply.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Australia Construction PMI Improved, back above 50

- Australia Employment Mixed

- Japan PMI Services Improved, back above 50

- Germany Factory Orders Mixed

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Trinity Mirror reaffirms full year expectations despite revenue fall

- Millennium & Copthorne Hotels' Q1 Rev PAR up 5.8%

- IMI first – quarter revenue falls 4%

- BT Group raises free cash flow outlook after strong year – end

- Aviva posts 14% Q1 rise in value of new business

- TBC Bank says Q1 profit rises 27%

- BT full – year earnings beat forecasts helped by fibre broadband

- BAE Systems maintains 2015 outlook

- RSA posts small rise in net written premiums, says low rates hurting

- Ineos completes purchase of shale gas licences from UK's IGas

- Randgold's mining profit falls due to lower gold prices

- Easyjet monthly passengers up 3.8% cancelled more flights in April

- esure says Q1 gross written premiums up 5.8%

- Acquisitions push Kingspan sales to end – April up 28%

- Wizz Air passengers up 23% in April

- Derwent London says Q1 vacancy drops to 1.9%

- Equinix confirms talks with Telecity Group

- Telecity, Interxion deal in doubt as Equinix weighs in