Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

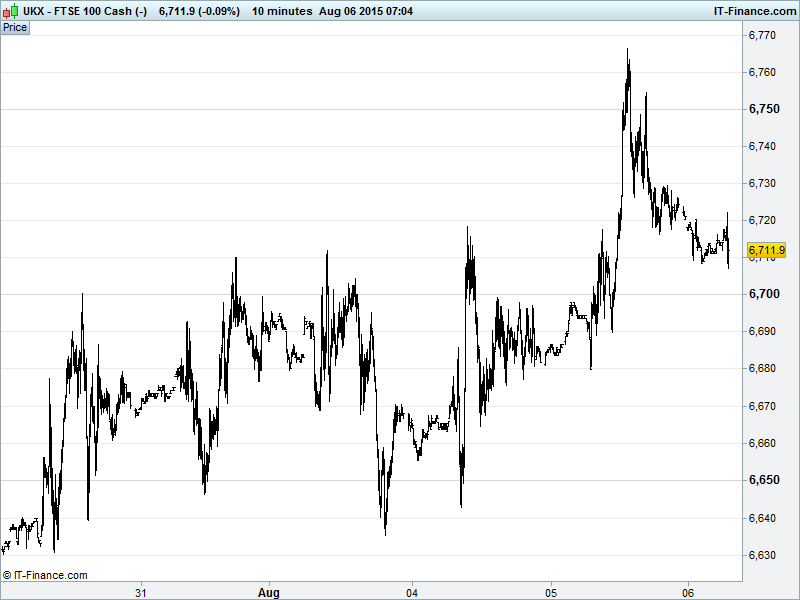

UK 100 Index called to open -40pts at 6710, having retraced towards 6700 after a breakout at 6750 failed after encountering the 6770 resistance duo of falling highs from June 4 and the 200-day MA. If 6700 can remain supportive, this should keep alive the uptrend from 6500 lows, however, a breakdown could see us revisit prior lows circa 6650. Updated watch levels: Bullish 6775, Bearish 6675.

The negative opening call comes despite gains in Asia based on US economic optimism with a weaker JPY boosting prospects for corporate earnings as expectations mount for a September Fed rate hike. Another leg down for Oil is weighing on global sentiment despite Copper stabilising after a bounce from bear market territory, while a weak ADP number yesterday is hampering bullishness about tomorrow’ Non-Farm Payrolls.

Asian trading under pressure with Japan’s Nikkei posting small gains (Topix near 8yr high) but Hong Kong and China extending declines on Chinese economic jitters and government intervention to prop up stock prices losing momentum. Australia’s ASX dented further by commodity price weakness, a disappointing jobs report and weakness in banks after a A$3bn cash call by ANZ.

Optimism still rising of a Greek bailout agreement ahead of the 20 Aug deadline (PM Tsipras says talks in final stretch, deal in coming days), while the ECB says it will maintain emergency liquidity assistance (ELA) for Greek banks for the next fortnight. Note the ECB’s Jazbec saying Greek debt relief (sticking point for IMF) not on the table.

On the M&A front note Zurich Insurance (ZURN) profits -43%, missing analyst expectations, and it saying it may return capital to shareholders if it doesn't buy the UK’s RSA Insurance (RSA), a deal designed to boost profitability but for which it says it will not overpay. Note RSA H1 results beating forecasts this morning.

US stocks closed lukewarm on Wednesday, with Wall St. futures currently in the red following mixed macro data: Early on, US ADP employment change came in much softer than expected, initially buoying the markets on hopes a September interest rate rise might be pushed back.

Later, however, US PMI Services edged up, pushing further into expansion territory while US ISM non-manufacturing jumped with non-factory employment recording its largest ever monthly increase. This all together failing to allay those rate hike fears as the USD strengthened, pressuring both equities and commodities.

Fed Governor Powell sought to balance Lockhart’s hawkish talk of a September rate hike, with the former seeking further improvement in the labour market while maintaining reasonable confidence that inflation is moving towards the 2% target. Note potential absence of volatility in US markets today in anticipation of tomorrow’s key (it always is) Non-Farm Payrolls.

US earnings, nonetheless, largely disappointed with CBS reporting shrinking advertising sales with profits propped up by share buybacks. Luxury electric car maker Tesla disappointed with its FY outlook despite beating Q2 expectations, while shares in Disney and Time Warner suffered under investor concerns about the future of TV. All about the outlook this time round, it seems.

In focus today will be June UK Industrial & Manufacturing Production with growth for the former seen slowing in June, while the latter rebounds. This follows blowout Factory Orders data from Germany this morning with June growth rebounding way beyond expectations - still the region’s powerhouse of industrial output.

Then it’s all about the Bank of England (BoE) which amid a shake-up by governor Carney aimed at increasing transparency will see it simultaneously release the latest policy decision (no change expected), the minutes/vote from that meeting and the quarterly inflation report. This deluge (billed ‘Super Thursday’) is sure to generate GBP volatility with increased speculation on rate rise timing given all the information made available at once rather than being drip fed.

Stateside crude inventories fell at a greater than expected rate in the week ending 31 July with stockpiles at Cushing, Oklahoma declining by 542,000 barrels, more than twice what was forecast. At the same time, US production was seen to be rising with the latter, along with an in-demand USD, being the better digested – Both Brent ($49) and US Light Crude ($45) are trading sub $50 and headed back towards their respective 2015 lows.

Gold ($1086) remains suck near 5.5-yr lows with net US data backing monetary policy tightening sooner rather than later – solid economic momentum hitting safe haven demand (which doesn’t seem to be doing much for the yellow metal anyway) while Bears continue to roam the campsite in China.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires/Bloomberg)

- Weak metals prices drag Rio Tinto H1 underlying earnings -43%

- Kerry Group nudges up FY earnings forecast

- Savills sees H1 profits boosted by U.S. acquisition, strong UK and Asian markets

- AstraZeneca signs immuno – oncology deal with Sosei unit Heptares

- Genel Energy first – half revenue +4%

- Genel Energy posts 15 pct rise in core profit

- Majestic Wine says CFO Nigel Alldritt to step down

- Cobham maintains full – year organic revenue growth guidance

- Randgold says Q2 profit from mining -7%

- Aviva posts forecast – beating H1 operating profit

- Inmarsat reschedules Global Xpress satellite launch for end – Aug

- RSA H1 pretax profit beats forecast as Zurich circles

- RBS raising $3.1bn through issue of CoCo bonds

- Enterprise Inns sees FY trading in line with its expectations

- Aggreko sees challenging 2016, warns on lower returns

- AIM restores trading in Quindell from 7.30 am on Aug. 6

- BTG says Health Canada approves Varithena

- Cobham keeps full-year revenue guidance

- UDG Healthcare says 9-months revenue ahead of last year

- Wincanton renews its distribution contract with Dairy Crest

- South Africa's Mondi posts 24% rise in H1 earnings