Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

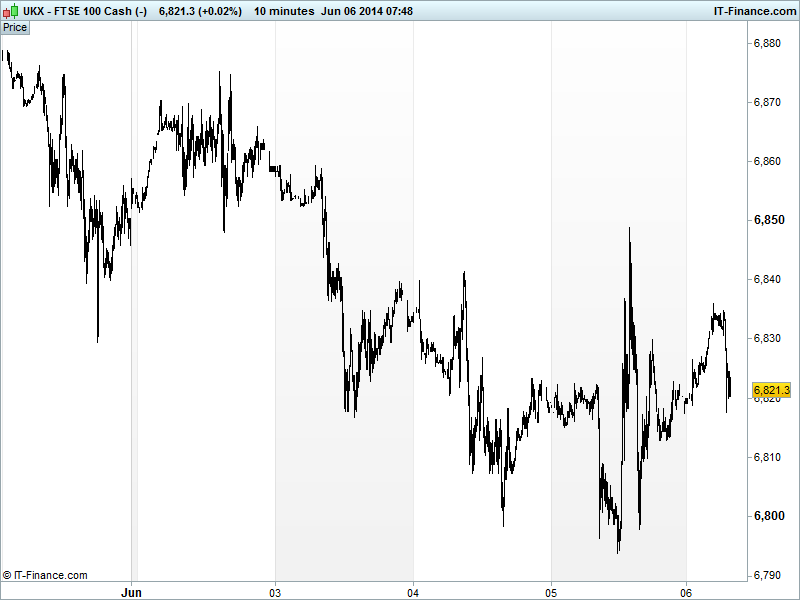

UK 100 called to open +10pts at 6820 after a positive close and decent gains in the US (more record highs posted by DJIA and S&P) following the ECB policy announcement and despite an indifferent response from Asia ahead of the US jobs report this afternoon. Note German’s DAX testing the 10,000 level.

The ECB delivered a host of stimulatory measures to counter rising Eurozone deflation risks (rate cuts, LTRO, negative deposit rates). Some were disappointed by a lack of QE, but Draghi did say preparations for ABS purchases had begun, interest rates will stay low for long (possibly longer than previously foreseen) and, more importantly, the ECB is not finished with easing and will do more if required.

Sentiment was also boosted stateside and overnight by renowned hedge fund manager David Tepper saying his market concerns had now alleviated and the Fed’s Kocherlakota arguing for real interest rates staying low for the next five years, even if peer Williams said there was a real cost to using monetary policy to address financial stability.

Overnight in Asia, stocks not reacting as positively, as traders move their focus from one risk event to another, digesting the ECB decision and prepping themselves for the next key risk events - US Non-Farm Payrolls this afternoon and China’s trade balance numbers over the weekend.

Note the World Bank seeing signs of improvement in China, and forecasts GDP growth of 7.6% in 2014 and 7.5% next year and the Chinese regulator CBRC said it was considering loosening the 75% loan-to-deposit ratio.

The UK index tested support at round number 6800 several times yesterday before recovering to 6830 overnight, however, resistance at the 6850 ECB-spike highs keeps it in the downtrend from 29 May, meaning potential for a revisit of 6770. A break above 6850 would open the door for a recovery to recent 6883 highs.

In focus today will be the US Jobs Report with expectations for 210K to have been added in May, this is far less than last month’s 288K but remains above the 12-month average of 197K and would be at odds with Wednesday’s ADP miss of 180K. The unemployment rate is seen rising a notch to 6.4% after hitting a low of 6.3% last month (from 6.7%) and getting markets spooked about early rate rises.

In commodities, Gold gas been boosted by the ECB stimulus announcement moving up off its recent lows of $1245/oz, to touch $1256 and by safehaven demand ahead of the US jobs report this afternoon following the ADP disappointment on Wednesday.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- AU AIG Construction Perf Improved

- JP Sentiment Indices Beat, mixed

- DE Industrial production Miss, mixed

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

• Telecom Plus finance director to step down in October

• British telecoms group KCom's profit falls marginally

• Ultra Electronics wins $19 mln contract with U.S. Navy

• Pubs operator Fuller's full-year profit rises about 10 pct

• GW Pharmaceuticals announces fast track designation from US FDA for Epidiolex