Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

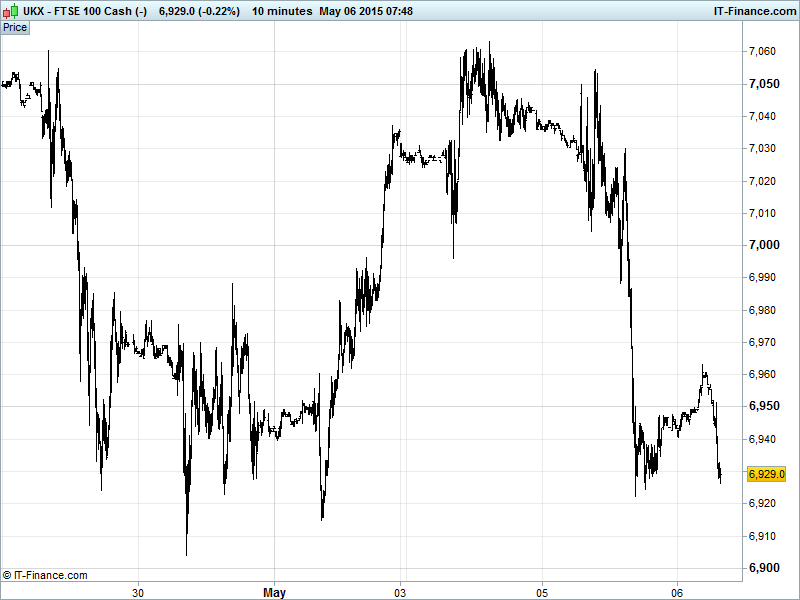

UK 100 Index called to open flat at 6930 following yesterday’s sharp sell-off. Support overnight around 6920 offers potential for rebound to toward 7040 ceiling of index’s current falling channel pattern. Watch for overnight bounce to 6960 potentially being the midst of a bearish flag pattern as well as the last hurrah of a bearish head & shoulders pattern formed over the last week. Watch levels: Bullish 7070, Bearish 6890.

The flat open comes after another selloff yesterday amid mixed macro data releases that were clearly cause for concern in the markets – with Aussie, Spanish, UK, Eurozone and US data largely missing consensus. In the UK in particular, Thursday’s general election will be stalling proceedings somewhat as investors await the outcome of one of the most closely run ballots ever, largely pondering the question of who will team up with who in the virtually inevitable event of a hung parliament.

US bourses finished Tuesday’s session nursing considerable losses following poor Services PMI and Economic Optimism prints, not to mention the ballooning Trade Deficit, that brought growth concerns to the fore again while speculation continued to stalk Europe with Greece’s debt situation becoming ever more tenuous. Expectations are that the US economy will have contracted in Q1 with several financial institutions now having revised their US GDP growth estimates for the period to a unanimous -0.5%. The Fed is naturally watching proceedings like a hawk – or perhaps more like a dove as things stand at the moment, though it is adamant that it won’t make policy based on 3-months of data.

Asian stocks mixed, with ex-Japan down for a second day in a row as banks and IT suffered following the weak US close on growth concerns (US, China, Europe), Greek debt speculation and Friday’s US jobs report. Chinese stocks rebounding on talk of the PBOC considering new >10yr loans to banks so they can buy local government debt, offsetting yesterday’s weakness on excessive stimulus hopes and higher margin trading requirements.

Australia’s ASX lower with a fourth successive improvement in China HSBC PMI Services and strong Aussie home sales growth failing to offset disappointing retail sales. Note the Fed’s Kocherlakota (non FOMC voter) saying a 2015 US Fed rate rise would be inappropriate given current consumption and inflation and Q1 growth weakness.

Today’s macro-economic releases encompass a raft of services PMI data with Spain, Italy, Germany, Eurozone and UK prints coming in quick succession, starting at 0815. This afternoon sees US ADP Employment Change and Non-Farm Productivity – either warming us up or getting us nervous ahead of Friday’s Non-Farm Payrolls.

Oil showing continued gains, with US Light Crude above $61/barrel, breaking above $60 for the first time this year following reports that a Libyan terminal had closed, while its Brent counterpart moved above $68/barrel. Commodities prices benefiting from Chinese data and a weaker USD following mixed stateside economic data, especially the much bigger trade deficit and economic optimism falling below 50.

Gold ($1196) is trending this week into the upper section of a longer term shallow falling channel as it continues to battle bugbear resistance at, and just north of, $1200 having failed to better its April highs $1224. The yellow metal is supported this week by a weaker US Dollar Basket, uncertainty surrounding the UK election and wider global affairs as macro data continues to come in wayward to consensus.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK BRC Shop Price Index Missed, Improved

- Aussie HIA New Home Sales Improved

- Aussie Retail Sales Missed, Deteriorated

- China HSBC Services PMI Missed, Deteriorated

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Game Digital names Mark Gifford as CFO

- Boohoo.com starts new year well as profits rise rise

- CRH sees 10 pct H1 earnings rise on continuing operations

- JD Wetherspoon posts 1.7 pct rise in Q3 sales

- Sainsbury's posts first underlying profit fall in a decade

- Legal & General Q1 net cash generation rises, net inflows drop

- Software firm Sage says on track to meet full – year targets

- GKN continues to forecast growth in 2015

- Wincanton says H J Heinz renews contract

- Intu Properties says key operating metrics are "stable"

- OneSavings Bank sees NIM ahead of expectations

- UK's OneSavings Bank sees net interest margins ahead of expectations

- Electra Partners says Electra Private Equity invests 25 mln stg in Park Resorts