Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

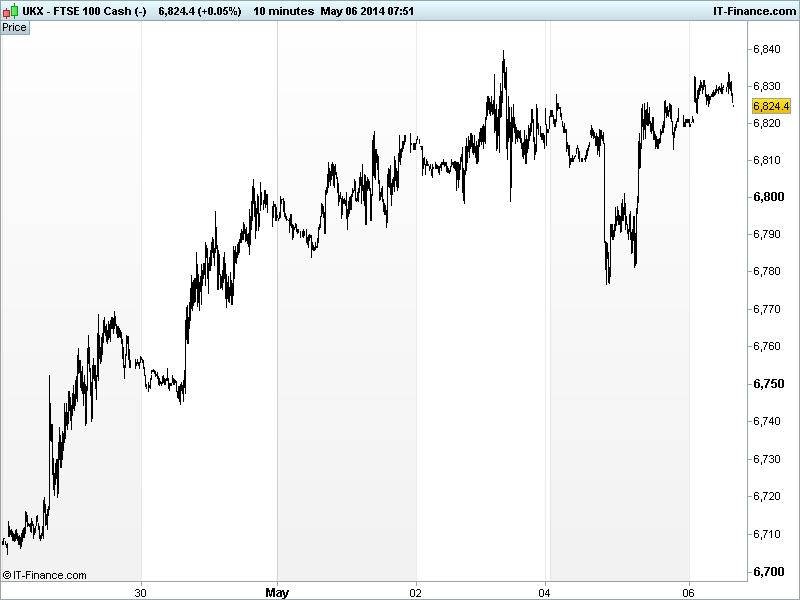

UK 100 called to open +5pts at 6825, trying to test Friday’s highs after a quiet start to the week, helped by equities in the US rebounding from early losses (S&P 500 still near record levels, but lead by defensives) to close positive after ISM and PMI Services improvements both beat expectations offsetting weak China Manufacturing data and a still extremely tenuous situation in the Ukraine.

Over the weekend the official China Services PMI improved to 54.8 from 54.5 in April, which looks to have revived some market optimism, this after global risk appetite started the weak on the back foot with the final HSBC China Manufacturing PMI reading missing estimates and showing continued contraction, as well as giving up ground on the preliminary (48.1 v 48.4est v 48.3 prelim) even if it did tick up from 48.0 March.

The positive start also follows a weak Friday close after US Non-Farm Payrolls and Unemployment Rate beat expectations (288 v 218K est; 6.3% v 6.6% est) but focus held on the drop in participation. Even though lower participation means people dropping out, combining it with upwards revisions to Q1 jobs adds and the fact it is back to level from the beginning of the year suggests the surprise unemployment rate drop more genuine.

So markets are again likely to start looking at US the situation as an economic positive rather than a negative via an earlier end to easy policy/stimulus. Could there be upwards revisions for the recently weak GDP too?

Overnight data included a lower Australian Trade Surplus in March as the RBA left interest rates unchanged at 2.5%, in-line with expectations. Other Monday data included further contraction in Aussie Services sector and Building approvals, while the Eurozone Sentix Investor Confidence fell back in contrast to consensus and Producer prices in the region showed a slightly lower rate of deflation in March (breathing room for ECB on the deflationary and need for stimulus front?).

Australia's ASX keeps displaying worrying early strength followed by weakness, all since the fresh 6-year high made a week ago. Miners BHP Billiton (BLT) and Rio Tinto (RIO), and three of the four major banks are all in the red after early gains, having initially recovered much of Monday's selloff. Elsewhere in Asia, China fluctuating while Japan, Hong Kong and South Korea all closed.

Results this morning from Barclays (BARC), which warned about a slight fall in profits two weeks ago, show a Q1 net profit beat of £965m v £934m est with focus on cost restructuring (strategy update Thursday). Adjusted profits fell to £1.69bn from £1.79bn a year ago hindered by the continued slowdown in Fixed Income, FX and Commodities; investment banking -28% to £2.49bn.

Elsewhere, Swiss banking peer UBS Q1 profits also beat expectations (CHF 1.05bn v 885m est). After the China manufacturing weakness, note miner Glencore reporting Copper production +24% YoY in Q1 due to higher output from its Congo mines and improved performance from certain mines in Latin America and Australia.

On the corporate activity front, note much press coverage of the Pfizer-Astrazeneca takeover and whether there will be another bid exceeding the rebuffed £50/share, while financial data and services provider Markit has revealed plans for a $750m US IPO which could come as soon as later this month.

In focus today: Eurozone PMI Services data with IT seen regaining growth territory (can it surprise again after the big jump in PMI Manufacturing last week?) and FR, DE and EZ confirming their flash readings (50-55). FR still close to breakeven, although while DE and EZ solidly in growth. The UK figure is seen strong and improving to 57.8 from 57.6, but remember how construction disappointed last week. EZ Retail Sales are expected to have weakened in March, giving up 0.2% versus growth of 0.4% in Feb.

In the afternoon, with a quiet line up we have but the US March Trade Balance (deficit expected to have fallen from $42.3bn to $42bn) and the IDB/TIPP Economic Optimism survey for May seen falling back from 48.0 to 47.5.

In commodities, Gold is back up around $1310 from its Friday lows of $1275 after renewed safehaven seeking by those watching the events in Ukraine. This also helped maintain US Light Crude above $99 and give Brent Crude a base at $107 after weakness to 5-week lows stemming from China data and more US inventory builds last week.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- AU Trade balance Miss, surplus fell

- AU Interest rate decision In-line, unchanged

- UK Q1 results: UBS, Barclays, Lufthansa, Adidas, Continental

See Live Macro calendar for full details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Countrywide sees full-year profits towards top end of its expectations

- AstraZeneca wins U.S. approval for heart pill

- Barclays Q1 profits fall as fixed income revenue slumps

- Balfour Beatty CEO steps down after profit warning

- Hiscox sees rates in many lines to remain under pressure

- Hiscox records claims from lost Malaysian plane, S.Korea ferry

- Rexam completes sale of healthcare businesses

- Salamander Energy reiterates 2014 production forecast of 13,000-16,000 boepd

- Glencore copper output up 24 pct, says trading strong

- Aberdeen Asset Management pretax profit -3%

- Just Eat says trading ahead of management expectations

- Xcite Energy inks collaboration agreement with Statoil and Shell