Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

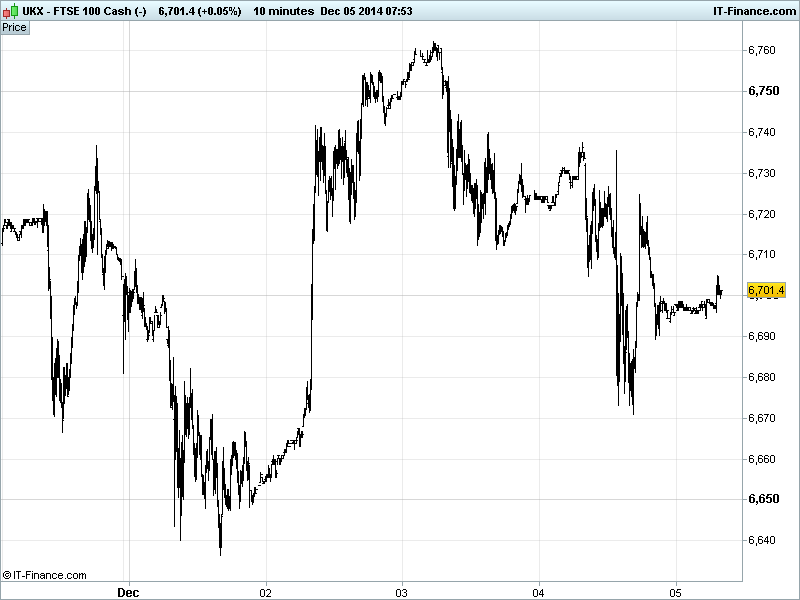

UK 100 Index called to open +20pts at 6700, with futures having traded there all night, mid-way between the prior day’s highs and lows, as markets sit tight ahead of the US jobs report following disappointment from the ECB. The index is now sideways since 18 November which could mean a pause before a resumption of uptrend/recovery. Watch levels: Bullish 6750 and Bearish 6660.

The ECB disappointed with its lack or urgency given the region’s woes by delaying a decision on QE (needs unanimity) and slashing growth and inflation targets which took markets from day highs, but this was offset by reports after the European close that the ECB was in fact preparing for ‘possible’ QE (sovereign debt purchases) in January which led to a recovery from the lows. Thanks for the volatility Mario & Co. in Frankfurt!

Positive opening call comes despite US bourses equities closing lower (only just) weakening into the close on comments in Die Welt that certain ECB members opposed President Draghi’s QE plans. Central Bank decisions dominated the little US macro data published with Challenger Job Cuts falling, the RBC Consumer Outlook rising but Initial Jobless Claims coming up short. A jump in German Factory orders is helping sentiment this morning.

Stocks in Asia mixed overnight with Japan’s Nikkei recovering from earlier losses as investors adopt their monthly cautiousness ahead of the US Jobs report, but helped by weak JPY after the USD rallied back from lows as buying resumed following weakness in the wake of the ECB update. (EUR strengthened on no QE, then reversed on possible QE, sending USD down then back up).

Hong Kong’s Hang Seng benefiting from continued strength in Chinese equities with Shanghai (+20% in last month) trading volumes hitting new records, likely helped by new trading link with Hong Kong and shares swinging the most since 2010 on a jump in valuations from near the cheapest on record, an increase in speculative bets fuelled by use of leverage/borrowed money and hopes of more central bank stimulus.

Australia’s ASX in the red, breaking a run of 3 positive days, as miners and energy fall, on a combination of caution before the US jobs report, the USD recovery, a miner mothballing an iron-ore mine and the AIG Construction Performance Index plunging into contraction.

In focus today, Eurozone GDP is seen showing muted growth for the Q3 preliminary reading. The US Jobs report is expected to show growth in job additions and a stable unemployment rate, however, remember the ADP reading on Wednesday did disappoint. The US trade balance is seen improving slightly on its deficit, while US Factory orders are seen flat in October after a weak September.

In commodities, Gold is holding around $1205, despite the volatility in USD. Support at $1200? The price of Oil remains under pressure following its early month rally, slowly retracing its gains with US Light Crude at $66.5 and Brent back below $70 after the ECB delayed its QE and the USD stayed strong as well as Saudi Arabia offering Asian customers record discounts on its crude, bolstering speculation it’s defending market share.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan Sentiment Indices In-line

- Germany Factory Orders Beat

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Songbird responds to offer from QIA and Brookfield

- Segro, Slough Borough Council renew landmark planning deal

- Ophir signs oil field production sharing contract with Myanmar govt

- Monitise signs strategic partnership with Virgin Money

- SThree says FY pretax profit in line with expectations

- Chesnara receives regulatory approval for CEO change

- Balfour rejects $1.6 bln John Laing Fund offer for PPP assets

- Interserve buys Employment & Skills Group for 25 mln stg

- Berkeley to meet full – year expectations as H1 profits rise 80 pct