Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

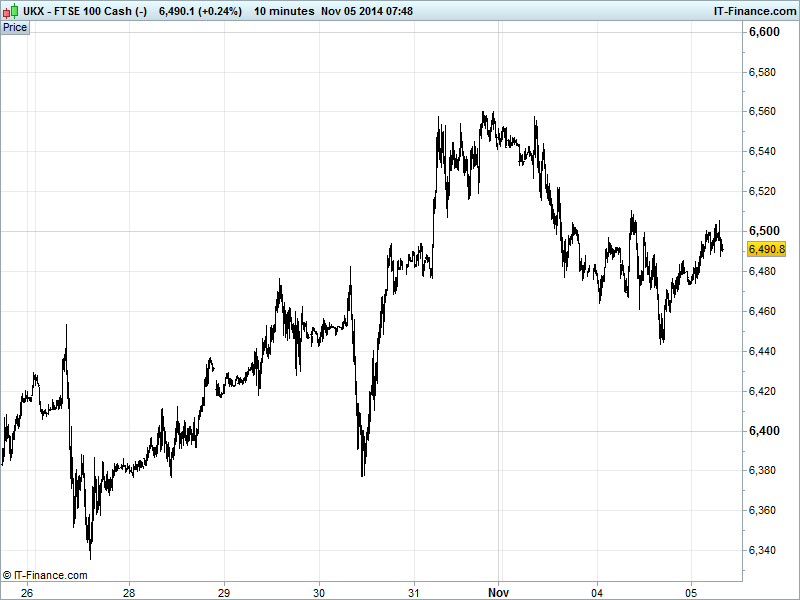

UK 100 Index called to open +35pts at 6495, rebounding to retest 6500 ahead of Thursday’s ECB monetary policy update on Thursday and Friday’s Non-Farm Payrolls. This follows a probe of 6450 late yesterday afternoon which may have taken indices too far. While the bounce keeps the uptrend from 17 Oct alive, the risk is that 6500 becomes resistance after the fall back below the trendline of rising highs from 14 Oct following a failed breakout on Friday. Watch levels: bullish 6505, bearish 6445.

Overnight the US Republican party has taken the Senate and thus control of Congress for the first time in nearly a decade after mid-term elections, with sweeping victories suggesting deep unease among voters towards the Democrats and President Obama. A Rep majority in the upper and lower house means political deadlock should be reduced helping towards reforms.

The positive opening call is despite a mixed US close, with another sharp slip in the price of oil weighing on US Energy stocks (White House non-committal on whether it will replenish strategic petroleum reserves), muted US data, a suggestion of ECB bankers challenging Draghi on his leadership style and question his decisions on QE and the Fed’s Bullard saying Fed does not need to consider more stimulus with economy in good shape.

Asia has delivered a largely negative session as worries over global economic growth following the European Commission's downgrade of expectations for the region, China’s HSBC PMI Services deteriorating in October and continued weakness in commodity prices denting sentiment.

While Asia mostly negative, Japan’s Nikkei continues to outperform both on a relative and absolute basis with a weaker JPY (>114) boosting exporter equities after BoJ governor Kuroda reiterated his central banks unwavering commitment to do whatever is necessary (sounds like Draghi!) to overcome deflation.

In focus today; final Eurozone PMI Services data with France expected to have contracted further, Italy to recover a bit towards breakeven, Germany and the UK to slip but stay in growth, and the Eurozone’s prior unchanged growth reading to be confirmed. Eurozone Retail Sales seen dropping in September suggesting a mix of consumer woes and warm weather in the region.

In the afternoon, the US ADP Employment Change is forecast to add a similar number of jobs as September, which would be supportive of the solid trend of around 250K jobs/month US Non-Farm Payroll (NFP) additions over the last 6 months. Note ADP often seen as warm-up for NFP which is on Friday. US Services PMI and ISM on-manufacturing Composite seen pulling back but remaining strongly in growth.

In commodities, Gold has fallen as low as $1550 as resurgent USD strength hurts demand and assets in the largest exchange-traded product backed by the metal dropped to a six-year low. This is coupled with expectations of US Fed moving towards a rate rise peers boost stimulus, while soft global inflation negates need for a hedge and strength in equities reduces safehaven demand.

Oil has plunged yet further as forecast for a gain in US crude stockpiles bolstered speculation that rising supply is outpacing demand, with the US and OPEC playing chicken. US Light Crude trades $75 with Brent Crude now below $82. Good for consumers if the get the lower prices, but bad for inflation.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK BRC Shop price Index Miss, deteriorated

- CN HSBC Services PMI Deteriorated

- CN HSBC Composite PMI Deteriorated

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Howden Joinery sees full-year profit ahead of expectations

- Stock Spirits warns on core profit

- M&S non-food sales fall for 13th straight quarter

- Alent Q3 net sales value rises 5.5 pct

- Alent appoints Andrew Heath as new CEO

- Lancashire's profit up on fewer catastrophe losses, Cathedral buy

- Wincanton first-half underlying oper profit rises 2.9 pct

- Costain says on track to meet its full-year expectations

- Costain gets contract from BAE Systems

- Firstgroup says trading in line

- Esure sees FY combined operating ratio rising to about 92 pct

- EMED Mining says expects to get final permit for copper project restart before year-end

- Old Mutual assets rise 5 percent, gross sales drop

- Meggitt cuts revenue outlook for 2015

- UK's Drax adds forward power sales despite a tough market

- John Menzies says Menzies Aviation MD Craig Smyth to resign

- Centamin cuts full – year gold output forecast at Sukari mine

- J D Wetherspoon first-quarter like-for-like sales rise 6.3 pct

- Firstgroup says trading in line