Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

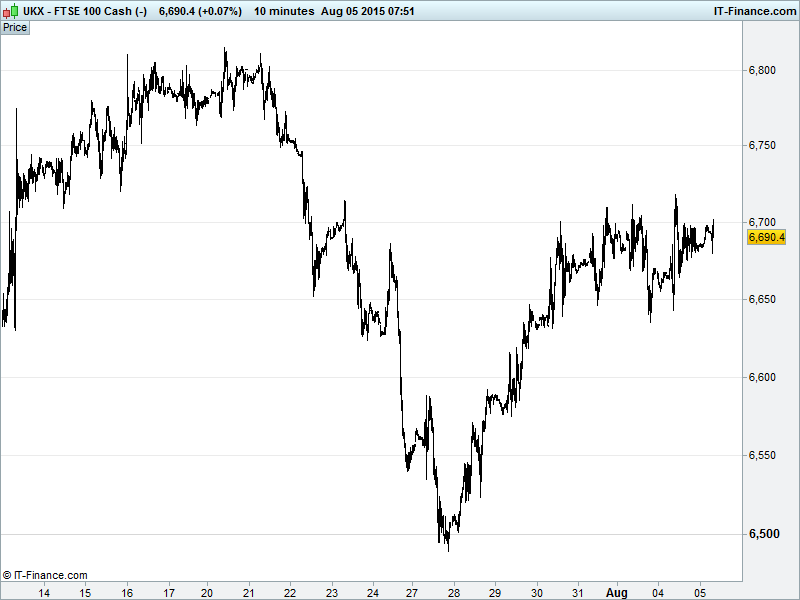

UK 100 Index called to open +5pts at 6690, trading 6680-6700 since yesterday afternoon. The range since late last week is slightly wider with support 6640 and rising highs 6700-6720 - a broadening formation of sorts. While the current sideways move could yet prove a pause before resumption of the uptrend, we still have to contend with falling highs from early June at 6750 as well as the 200-day MA 6770. Updated watch levels: Bullish 6730, Bearish 6630.

The mildly positive opening call comes after an improvement in Caixin China PMI Services to an 11-month high helped Crude oil to bounce higher and despite heightened speculation the Fed will pull the rate-hike trigger in September sending the USD to fresh 4-month highs ahead of Friday’s jobs report, ushering Copper and Gold lower.

US markets edged lower, with many on the side-lines ahead of Friday’s US labour market update, and held back by uncharacteristically hawkish comments from Atlanta Fed President Lockhart who said that the Fed is ‘close’ and it would take a significant deterioration in US economic health for him not to support a rate rise from record lows next month. Persistent weakness in Apple (AAPL shares) also continues to dent confidence.

Declines were despite optimism of a Greek deal in the coming days with ‘constructive collaboration’ potentially allowing approval before the €3.2bn due to ECB on 20 Aug after a report from think-tank NIESR claimed Athens needs debt relief of €100bn (more than the IMF demands) if the nation is to stand a chance of clawing its way out of depression.

Note the Telegraph’s Pritchard saying monetary expansion and leading indicators in Europe, America and China all point to stronger growth this year, signalling another leg to the global expansion, however, the NIESR says UK growth is set to slow in Q3, lowering its previous estimate, and it sees the Bank of England raising rates in Feb 2016. Note UK Shop Price deflation accelerating in July.

Asian stocks largely higher overnight, paring initial losses despite a weak lead on Wall Street (due to hawkish commentary from the Fed’s Lockhart) with oil prices continuing off their 3 Aug lows and some encouraging macro data from China (July Caixin services PMI coming in at 53.8 – the best score in 11 months) boosting sentiment. China’s stock market nonetheless resumed its declines as government intervention began to deter investors, with trading volume down significantly overnight.

Additional Services PMIs came in from Japan (overall expansion slowing, but employment and business sentiment improving) and Australia (spiked to a 17-month high with all sub-indices outperforming), whose own print was supported by a housing market rebound, low interest rates and a weak AUD.

In focus today will be July final Eurozone PMI Services with the major nations confirming still solid expansion but ticking back from June while Retail sales for the single currency region are seen falling. In the afternoon, the US ADP Employment Change will likely serve as a warm-up act for Friday’s Jobs report supporting another month of 200K+ jobs creation while US PMI Services is expected to be confirmed higher in July.

Crude prices continue to recover Wednesday with traders expectant of a fall in US stockpiles – typically indicative of increased demand both in the US and China. Friday’s non-farms report also being eyed for its effects on USD strength ahead of a potential September US interest rate hike, which would have a knock-on effect on commodity prices. Brent is testing $50 while WTI trading around $46.

Gold ($1087) remains range bound and under pressure near the floor of a longer term trading channel with USD strength on hawkish US Fed commentary keeping the non-interest bearing yellow metal near 5 year lows. Note physical demand from China could become a driver if the world’s #2 economy starts to push hard to get reserve status for the Yuan – the IMF recommending it boosts gold reserves to help back up the currency.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Legal & General H1 operating profit rises 18%

- London Stock Exchange H1 earnings see boost from UK Index – Russell

- Ryanair says July traffic up 11% to 10.1m customers

- BBA Aviation remains confident in FY outlook

- Devro says H1 pretax profit up to £9.6m

- Spirax – Sarco first – half adjusted pretax profit slips

- IP Group's H1 adjusted pretax profit £70.1m vs £15m

- AstraZeneca's Medimmune partners Mirati for immuno–oncology combination in lung cancer

- Soco raises lower end of full – year production guidance

- Ferrexpo interim earnings hit by iron ore slump