Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

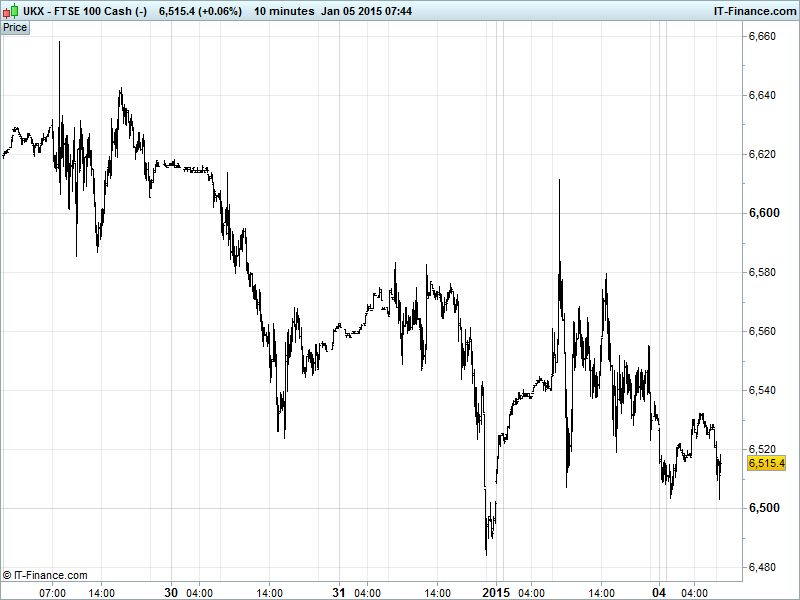

UK 100 Index called to open -30pts at 6515, on the back foot having retraced to 6500 from Dec 29 highs of 6650. Will the trend of falling highs from September persist taking the index back towards recent lows of 6100 or will support takeover at 6500 helping the index regain 2014 highs of 6750-6900?

The negative open to kick off the first full week of 2015 stems from continued global growth uncertainty (China, Europe) and oil maintaining its southerly course to fresh 5.5yr lows on speculation that the global supply glut will keep it in bear market territory as well as a strengthening USD.

US bourses closed flat on Friday on very low volumes following sluggish US and Eurozone Manufacturing data which led to questions about the US recovery and the Eurozone’s need for full-on QE from the ECB, along with geopolitical risk getting a boost from the US authorizing sanctions against North Korea following the Sony film hack.

Note better than expected and improved China PMI Services over the weekend has offered little support to European opening calls for equities or indeed commodities, with manufacturing output still the focus.

Fed talk saw Mester say rates could rise anytime in 2015 but that it’s the pace of increases which is more important than the first hike itself. Colleague Rosengren also said low core inflation and wage growth requires patience on monetary policy change but that tighter policy needed to spur wage growth. Peer Kocherlakota suggests discretion should be used rather than policy rules.

In Europe, worries continue around the Greek election outcome with polls showing anti-austerity party Syriza leading the ruling conservatives by 3.1pts, and reports that Greece could exit the Euro. PM Samaras has warned as to the possibility, in contrast to Greek opinion polls, while Germany says it is manageable.

The EUR remains weak (2006 lows versus USD) on the back of Draghi’s newspaper comments heightening the prospect of the ECB launching QE this month, although the Greek election result (25 Jan, after next ECB meeting) could see it delayed until Feb.

Overnight, Asian bourses mixed with Japan’s Nikkei in the red despite a still weak JPY and a stable PMI Manufacturing reading and slowing in of vehicle sales contraction. The weak oil price theme continues to weigh heavily on sentiment as do fresh Eurozone jitters and weak Australian PMI manufacturing.

In focus today we have Eurozone Sentix Investor Confidence which is expected to improve while UK Construction PMI edges down from its prior strong reading. German Consumer Price Inflation likely the standout data given the risks of Eurozone deflation and calls for QE from the ECB to revive the region. After sluggish US manufacturing data last week, watch ISM New York as sole US data print today.

Gold has rebounded from Friday’s 1-month lows $1168 to trade back near $1200 despite US dollar strength on divergent central bank policy and equity appetite, likely benefiting from continued short-covering from early December highs and fresh safehaven demand linked to Eurozone jitters on the Greek election outcome and possible exit from the Euro.

We now see US Light Crude testing $52/barrel and Brent $56 on global supply glut peculation and as the USD keeps rising in response to Fed rate rise expectations.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – it’s all part of the service.

Key Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan PMI Manufacturing Stable

- Japan Vehicle Sales Contraction slowed

See Live Macro Calendar for full data line-up, incl. consensus expectations

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Gulf Keystone says focusing on maintaining 40,000 bopd target

- Galliford Try construction unit completes 45.2 mln stg contract

- Mcbride says trading in first-half in line with board's expectations

- Heavy rain storm in west Australia raises cyclone threat

- Xaar appoints Doug Edwards as chief executive

- Rockhopper says awarded 40 pct interest in Croatian project

- Brit and Versutus agree quota share reinsurance deal